Why Bitcoin’s volatility is irrelevant

The importance of time

Bitcoin’s store of value narrative took hold during the macroeconomic changes of 2020. The global pandemic and its consequences forced nations around the globe into lockdowns. Economic activity slowed down substantially, and millions of people lost their jobs. Governments had to step in and provide stimulus to keep cooperations and people afloat. Money printing was the answer. It provided short-term stability in exchange for future economic uncertainty.

The fear of inflation rose with the money supply, and asset managers everywhere started looking for a store of value. A place that secures purchasing power over a long period of time. Bitcoin during those times was still far below its last all-time high, the peak of the bull market in 2017.

The halving, the event that cuts mining rewards in half, is often cited as the beginning of a new boom and bust cycle for the decentralized currency. It happens every four years, and the next one was set to be during the summer of 2020. Cutting the incoming Bitcoin supply in half creates a shock on the supply side, which serves as a catalyst for a new bull market.

That’s part of the reason for all the 100.000$ price predictions and the stock-to-flow model by PlanB.

The timing of the fourth halving couldn’t have been better. It coincided with the search for a new store of value, and many asset managers that were never interested in crypto started to reevaluate bitcoin’s potential to serve that purpose.

Michael Saylor was one of them. He and his company Microstrategy were forced to find a place for the cash on their balance sheet. From his perspective, he was sitting on a melting ice cube. If he didn’t do anything, the companies purchasing power would slowly disappear over the years to come.

Michael Saylor and his team were evaluating all the different options. Real estate, stocks, gold, alternative assets like art or wine. But nothing beat bitcoin when it came to the properties that were essential to protect purchasing power. It has true scarcity, a hard cap at 21 million. It‘s decentralized, unconfiscatable, and independent of any government or central authority. Microstrategy found a new home for their cash and bought bitcoin during the summer of 2020.

While Michael Sayler was the most prominent many made a similar move. Asset managers that previously saw nothing but speculation in the digital asset discovered its value for the first time and changed their minds. It was no longer a career risk or fringe opinion to see bitcoin as an important asset of the future economy.

But the spotlight bitcoin found itself in also brought many of the critics back. And the endless discussions, speculative asset or not, that died down after the crash of 2018 started anew. And I don’t see that as a bad thing. Debates are healthy and needed for any idea. Without critics, we wouldn’t get anywhere.

I wrote this to address a common argument that gets thrown around a lot. One that I see almost every single day on Twitter.

How can something as volatile as bitcoin be a store of value?

How volatile is bitcoin?

Before I address the argument, let’s look at the data over the last decade to see how volatile bitcoin really is.

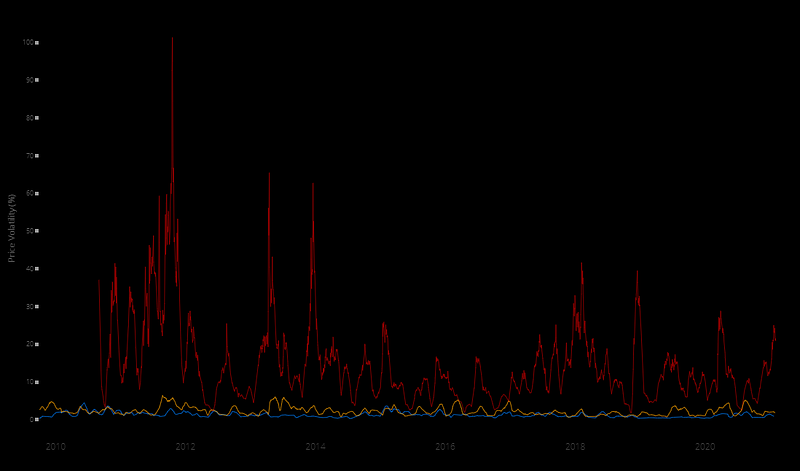

The chart below compares bitcoin’s 60-day volatility (red) to gold (orange) and USDEUR (blue).

As you can see, bitcoin’s 60-day volatility was everywhere between 2% and 101% over the last ten years. Gold rarely went above 5%, and the USDEUR volatility stayed below that for the entire decade. So bitcoin’s volatility is, without a doubt, far higher than that of gold or fiat currency.

But the chart shows us something else that’s noteworthy. If we look at the volatility over time, we can see a trend. It’s decreasing. The chart shows lower lows and lower highs year after year.

That’s not surprising. The more people trade the asset and the higher its market cap, the harder it becomes to move the price. This also correlates with the decreasing rate of return we get in each cycle.

Once Bitcoin reaches gold’s market cap (9 trillion USD), I suspect the 60-day volatility will be comparable. That’s still more than 1400% from where Bitcoin is today (02.02.2021).

Just because Bitcoin is highly volatile now doesn’t mean it’ll stay that way forever. The asset needs time to mature before we can give an accurate judgment.

Why volatility is irrelevant for a store of value

No matter how volatile Bitcoin really turns out to be, this one metric alone shouldn’t be a deciding factor for the store of value argument. As so often, when it comes to investments, your time horizon is way more important than anything else. How long do you plan to hodl? one year? Five years? Ten years?

The longer you hold an asset, the less important is short-term price fluctuation. Why would you care what the price does while you’re holding? As long as your purchasing power is higher or equal by the time you sell, the purpose of a store of value is fulfilled. Everything that happened in between is just noise and can be ignored.

So if you consider buying bitcoin as a store of value, you shouldn’t be concerned about volatility. You should ask yourself a different question.

What is the longest time period that bitcoin’s price spent below its prior all-time high?

Or in other words:

If you bought at the worst point in Bitcoin’s history, how long did it take until you could sell your position without a loss?

The “worst” date to buy bitcoin was November 29th, 2013, when the price was at 1242$. If you bought back then, literally at the peak of the bull run, you had to wait 1189 days, or a bit more than three years, until you could sell without a loss (red line).

But we don’t just want to sell without a loss in USD value. We want to keep our purchasing power. So we have to take inflation into account.

During those three years that we were holding, the dollar had an average inflation rate of 1.28% per year, a cumulative increase of 5.22%. If we add that 5.22% to the 1242$, we get 1306$. That’s the price we need to sell at to retain our purchasing power.

Bitcoin hit 1306$ for a few minutes on March 10th, 2017, but I’ll ignore that for the sake of this example because I’m guessing most people would’ve missed it unless they put in an exact limit sell order. Bitcoin hit the same price again on April the 26th, 1244 days after our initial purchase (blue line).

So if your time horizon is anywhere beyond three years and five months, the historical data suggests your investment will be fine and retain its purchasing power.

You might say that past performance isn’t indicative of future results, which is true. But the same goes for volatility. This analysis's whole point was to show that volatility alone is not an argument against bitcoin being a store of value. It doesn’t matter what the price does in short periods of time. The long-term trajectory has always been up, and if you believe in Bitcoin on a fundamental level, volatility shouldn’t scare you.

It all depends on your time horizon.

Join Coinmonks Telegram group and learn about crypto trading and investing

Also, Read

- What is a Flash loan?

- The Best Crypto Trading Bot | Grid Trading

- 3Commas Review | Pionex Review | Coinrule review

- AAX Exchange Review | Deribit Review |FTX Exchange Review

- NGRAVE ZERO review | Phemex Review | PrimeXBT Review

- Bybit Exchange Review | Bityard Review | CoinSpot Review

- 3Commas vs Cryptohopper

- The Best Bitcoin Hardware wallet | BitBox02 Review

- Ledger vs Ngrave | Ledger nano s vs x

- Crypto Copy Trading Platforms | Bityard copy trading

- Vauld Review | YouHodler Review | BlockFi Review

- The Best Crypto Tax Software | CoinTracking Review

- Best Crypto Lending Platforms | Leveraged Token

- Ledger Nano S vs Trezor one vs Trezor T vs Ledger Nano X

- BlockFi vs Celsius | Hodlnaut Review

- Bitsgap review | Quadency Review

- Ellipal Titan Review | SecuX Stone Review

- DEX Explorer | Blockchain APIs | LocalBitcoins Review

- Best Blockchain Analysis Tools | Earn Bitcoin

- Crypto arbitrage guide: How to make money as a beginner

- Best Crypto Charting Tool | Best Crypto Exchange

- What are the best books to learn about Bitcoin?

Get Best Software Deals Directly In Your Inbox