Money

We Spend All Our Lives Earning It But Are Clueless About How To Manage It

Money may not buy you happiness, but it buys you freedom, and that may be better than happiness!

The hard facts

It touches almost every aspect of your life- your health, relationships, dreams for your future, and sense of security. Yet, speaking of it is still taboo in some homes, and many people still avoid openly discussing it. And we’re doing a lousy job at managing it.

Living paycheck to paycheck.

Yes, I am talking about your hard-earned money. According to Lending Club Corp, 64% of Americans live paycheck to paycheck. If you were to lose your job today, what would happen to your life? Live on your credit card till you land a new job?

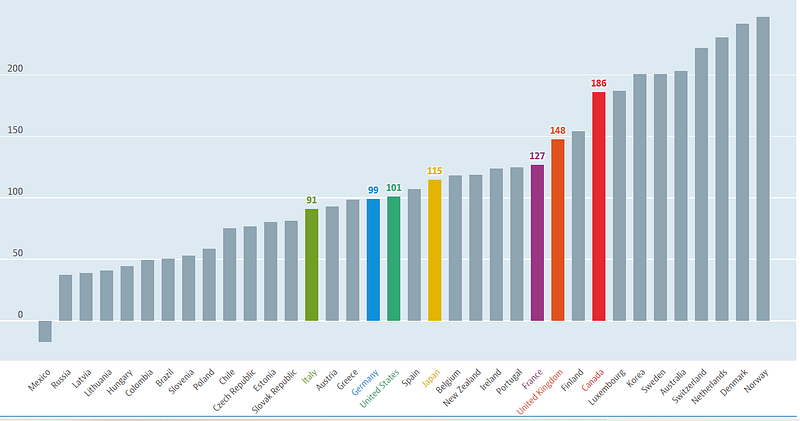

Deep in dept.

People are deep in debt. The latest statistic from the Federal Reserve Bank of New York has Household debt totaling almost $16T in the US. Below are the figures from the OECD on household debt as a percentage of net household disposable income. According to these figures, Canadians, on average, owe $186.00 for every $100.00 earned.

The cause of conflict

Conflicts over money are still one of the main reasons couples get divorced. Money issues cause tremendous stress on an individual. If you’re stressed out about money, you’re not alone.

Cause of stress

A recent survey completed by the American Psychological Association found that money is a top cause of stress for many Americans. This is not the case just in America, especially since Covid.

How did we get into this mess?

How did we get into this mess? We have had access to easy credit at extremely low-interest rates for the last twenty years. On top of that, house prices have accelerated, and people have started to use the equity in their homes as an ATM.

In 2021, Canadians owed just over $260B in home equity lines of credit. We’re sinking deep in do-do with the illusion that home prices will keep rising, and we’ll have this never-ending supply of money.

We are starting them young.

Financial Institutions are very creative in enticing people to spend even before they’ve earned. Starting from when they are kids, students are offered a credit card.

Almost 65% of college students have credit card debt. And added to that, 58% carry student loan debt. Most students are starting their lives in debt.

Turning the ship around

It is obvious things need to change. Here’s how:

1. Decide your financial future.

Studies have shown that we are more likely to reach our desired outcomes by setting goals. According to a study conducted by Dr. Gail Matthews, a psychology professor at the Dominican University of California, you are 42% more likely to achieve your goals just by writing them down. So, why not give it a shot?

Write a list of your financial goals and set a timeline for when you’d like to achieve these goals. It could be to pay off debt, put a down payment on a new home or launch a business. Decide when you’d like to accomplish these.

2. Don’t get it if you can’t pay for it.

Carrying debt robs you of a stable financial future. If money provides you with freedom, debt restricts your options of doing what you want to do.

Start by paying the loan or credit card with the highest interest rate. Or pay the loan or credit with the smallest balance owing, which has a snowball effect.

Eliminating debt one loan at a time — allows you to achieve small wins. Small wins give you a sense of satisfaction, creating momentum to tackle other debt.

Keep two credit cards and cut the rest. If you need to replace your furniture or buy a new car, pay cash instead of getting a loan.

3. Put aside a portion of everything you earn.

Start by saving 10% of your income each time you get paid. You can create an emergency fund — which should be three to six months’ worth of living expenses.

Only use your emergency fund for dire circumstances., like a leaky roof, car repairs, or a job loss.

Once you’ve created an emergency fund, the rest of your savings should be allocated to achieving your financial goals.

4. Investing is the only way up.

Your additional savings should be invested. Wise investing allows your money to work for you. A savings account may generate about one percent in interest. At that rate, it will take you forever to achieve any of your goals.

You don’t get rich by savings but by investing. Invest in assets that increase in value over time. Assets such as real estate, stocks, and bonds.

By investing in stable, high dividend-paying stocks, you’re looking at an average annualized potential return of over 6%. Compounded over time, this will build into a nice nest egg. If you’re young, time is on your side!

5. Start a side-hustle.

Do you have a passion or skill that you know and enjoy? Why not teach it online? Share your expertise through YouTube videos. Thinkific and Udemy are great platforms to upload your lessons. Or start writing on blogging platforms such as Medium.com.

Billionaire financier Warren Buffett says, “If you don’t find ways to make money while you’re asleep, you’ll work till you die.” And no one wants to work at something they don’t enjoy till they die.

6. Protect Your Family

The best-laid plans will derail if you don’t protect your greatest asset- yourself and your ability to earn an income.

What would happen to your family’s financial situation if you become disabled or die?

Do you have insurance to protect them from the loss of income if tragedy were to strike? Consult with an insurance advisor on how you can protect your family in this respect.

7. Invest In You

The best investment you can make is to invest in yourself. Through thinkific and udemy or skillshare courses, pick up a new skill this yeat. Learn about investing and managing your money. Or deepen your knowledge on something you’re passionate about.

Join Medium for $5 a month, enjoy thousands of articles, and get paid to write. Sign up HERE. This is a Medium revenue-sharing affiliate link. If you sign up using this link, you can support me and others as a fellow writer. I will receive a portion of your Partner Program membership fee for the referral; however, it will NOT increase your membership cost.