What Is It Costing You For Advice?

There is no free lunch, especially not in the financial industry.

Most financial advisors do not ‘charge’ for advice. They get compensated when a potential client takes action and decides to invest with them. The investments selected have a fee applied to them. Some of these are embedded. And can add to a substantial amount of money.

Four types of sales charges

Front-end load / initial sales charge (ISC). Some mutual funds charge a fee when you buy your units or shares. This fee is a percentage (up to 5%) of your investment in the fund.

The mutual fund company pays the investment firm selling you the fund. You can sometimes negotiate this fee with your advisor.

Back-end load / deferred sales charge (DSC). Some funds charge a fee of up to 6% when you redeem your units. This fee declines every year according to a fixed schedule. The longer you hold a fund with a DSC, the less you’ll pay when you sell it.

If you hold it long enough (typically between 5 and 7 years), you won’t pay a fee when you sell the fund. If you sell it within two years, you may end up paying up to 4% to 5% of the value of the amount sold.

Some fund companies may also let you redeem some of your money (usually 10%) out of the fund each year without charging you a fee.

Your advisor’s firm receives commission (usually about 5%) upfront from the mutual fund company when you buy the fund. Your advisor receives part of this commission. Any deferred sales charge you pay goes to the mutual fund company.

Low load / low sales charge (LSC). Low load funds charge a lower redemption fee (up to 3%) when you sell your fund. You usually won’t have to pay a redemption fee if you hold your units or shares for at least three years.

No load. A no-load fund doesn’t charge a fee when buying or selling its units or shares. Advisors are often paid according to the type of load you purchase. Mutual fund companies reward advisors for selling high-load funds.

Most fund companies allow you to redeem 10% of your fund annually at no cost if you purchased them with a deferred sales charge.

Ensure that your advisor is not redeeming this 10% each year only to turn around and purchase the same fund but this time with a front-end load! This practice is quite common!

The advisor gets paid twice, but you have just ended up spending 2% for something you did not need. You should compare the MER and performance of each fund before you decide.

Management Expense Ratios:

Besides the “loads,” the infamous management expense ratio (MER) is charged on the mutual fund each year.

The MER includes the management fee the mutual fund company earns. It consists of a trailing commission paid to the adviser’s firm that sold the fund. It also covers the cost of advice to the client. We can assume the advisor advised the client to purchase the investyment.

The MER also includes the fund’s daily operating expenses, such as record keeping, audit, legal fees, and charges for sending out prospectuses and annual reports. Over and above the MERs are trading costs to buy and sell the securities held in the mutual fund.

MERs can range from a low of 0.20% (as in the case of Exchange Traded Funds) to 3.5%, as is the case for some international equity mutual funds. The MER is taken off the mutual fund each year.

So, if your fund reported a return of 5% and the MER is 2.5%, then the fund did 7.5%, but 2.5% was taken off for the MER.

Since this is charged every year regardless of the level of advice you are receiving or the fund’s performance (yes, you pay even when the fund makes nothing!), it can add up to a large amount over time taken off your portfolios.

So, if your fund had a front-end load of 2% and a MER of 2.5%, now you must make at least 4.5% to break even the first year.

While you cannot control the markets, keeping your costs down will ensure it is not “eating” into your return.

Actively Managed Investing.

Wrap Accounts:

Often referred to as “portfolio solutions” or “managed portfolio services.”

There are three types of wrap accounts.

Mutual fund wrap.

These are portfolios tied to objectives based on a questionnaire provided by the firm, ranging from “income” portfolios that are conservative to “aggressive growth” for aggressive investors.

Pooled funds wrap.

These are portfolios of proprietary pooled funds. A profiling questionnaire leads to a recommended mix of the program’s pools, usually based on Modern Portfolio Theory.

Separately managed fund wraps.

These are separate portfolios of individual securities held by the broker and managed by a professional money manager. The managers in these programs are like those found in mutual and pooled funds. The difference is that the client gets individual securities instead of a mutual fund.

Wraps offer automatic rebalancing, which means they adjust your holdings periodically to make sure you don’t stray from your target mix of assets. If stocks are soaring, your wrap will reduce your stock holdings.

Your wrap will buy you enough to get back to that target mix if stocks are sinking. Wrap accounts are cookie-cutter approaches to investing.

The management fees are also usually high. They offer convenience to advisors and clients.

Index Funds.

So far, I have covered fees regarding actively managed funds, where there is a team managing the assets in the fund or the pool.

As clients get more sophisticated and become more fee-sensitive, they are less willing to pay for management fees, especially when many of these funds are underperforming their benchmarks, often due to the higher costs.

The alternatives are index funds and exchange-traded funds. Index funds mirror the holdings and performance of a stock market benchmark, such as the S&P 500.

Therefore, there is no need for intense research and analysis to actively seek stocks that may do better during a given time frame. Actively managed funds have higher fees, presumably to generate superior returns.

However, research has often shown active management to underperform the broader market after accounting for fees. For the past ten years, actively managed funds have underperformed the index.

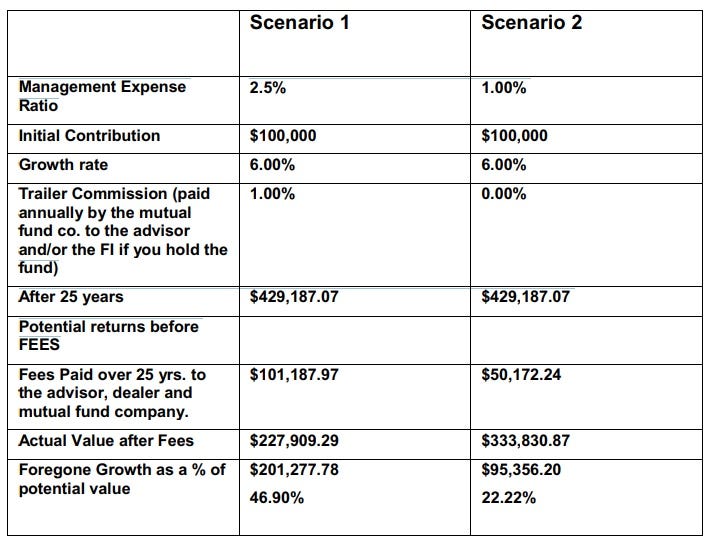

The Impact of Fees on Your Portfolio Over Time.

Fees’ eat into’ your portfolio. Almost 50% of the value of your portfolio, as shown in the example above.

Paying 1.5% more for the 1 in 5 chance of a better return, in my view, is not the best way to keep costs down.

Most advisors are compensated for recommending actively managed funds over Index Funds.

The past ten years have seen explosive growth in Exchange Traded Funds (ETFs). Initially, Exchange Trade Funds were like an index fund, tracking an index, a commodity, bonds, or a basket of assets.

Over the last few years, many large ETFs providers have been offering actively managed ETFs. At a fraction of the cost of an actively managed fund.

Unlike mutual funds, an ETF trades like a common stock on a stock exchange. ETFs experience price changes throughout the day as they are bought and sold. ETFs typically have higher daily liquidity and lower fees than mutual fund shares, making them an attractive alternative for many investors.

Holding a mutual fund with a high MER in your portfolio adds up to a lot of money over time. Countries such as Australia and The UK have banned embedded fees.

It is essential to know what you’re paying for your investments. The MER is not reduced during the downturn, making it even more challenging to recover over time.

Choosing a fee-based advisor who selects ETFs and Index Funds can save you money since they are not benefitting from trailers and commissions. Don’t drag your returns by holding investments with high fees.

Does the advice you are receiving warrant the fees you are paying?

“IIf you invested in a very low-cost index fund — where you don’t put the money in at one time, but average in over ten years — you’ll do better than 90% of people who start investing at the same time” — Warren Buffet

This article contains affiliate links. I may receive compensation for items purchased through these links.