Warren Buffet — “To Become Rich, Buy Stocks Below Their Intrinsic Value.” Here’s How You (Exactly) Find It!

Bob at the grocery store asked me to buy the new AI stock.

“This will go up buddy!” — he said.

But will it?

And if it would, what’s the reason for it?

Let’s discuss all of this in this article.

Why Do Stocks Go Up?

Every investor’s dream is to buy stocks low and then sell them at a higher value.

But have you ever wondered where the stock market’s returns come from?

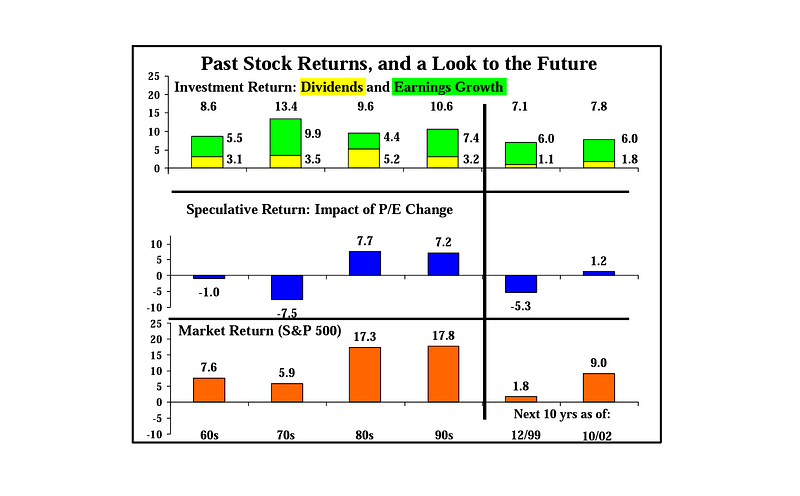

There are two components to the returns:

Speculative Returns

These are the returns gained on relying on a greater fool to take a stock off your hands at a higher price when the time arrives.

One’s return depends on the gullibility of others when using this strategy of speculation.

In more formal terms, the speculative return comes from the changes in the price-to-earnings (P/E) ratio of a stock.

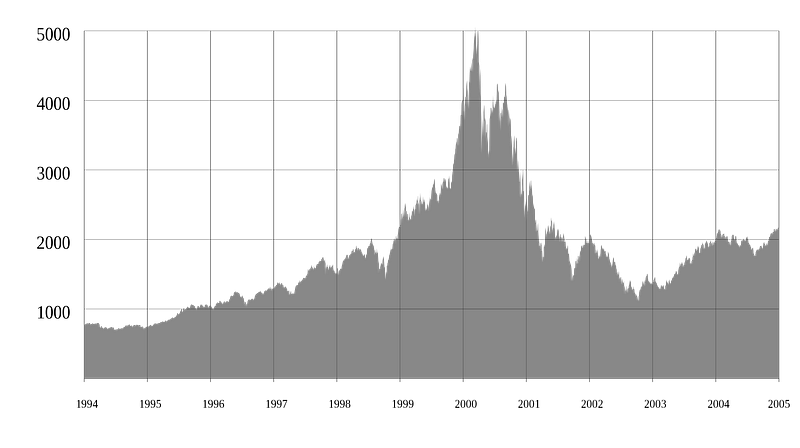

An example of this was seen during the Dot-com bubble of the late 1990s when the majority of people were solely relying on speculation for higher returns.

Investment Returns

Investment return is the appreciation of a stock because of how well a company is performing its operations and growing.

This is shown by a company’s:

- Dividend yield

- Earnings growth

John C. Bogle, the founder and former CEO of Vanguard, one of the largest asset-managing firms in the world, addressed this by saying that:

Contrary to popular belief, over a long time span, the impact of Investment returns trumps the impact of Speculative returns.

This is one of the most important takeaways for life that you can have when investing in stocks.

When To Invest?

Now that you know that efficiently operating and growing companies will give higher returns in the future, should you just buy their stocks at the instant that you identify them?

Not really!

Let’s learn what Warren Buffet, one of the wealthiest men on the planet, has to say about it.

Warren, in his various interviews, letters to shareholders, and public interviews points us towards an extremely crucial concept to internalize when investing.

It is —

Identifying the Intrinsic value of a company and buying its stocks below this, keeping a margin of safety.

This means that one should be buying companies that are undervalued relative to their future earnings potential and net value.

The more that you buy at a discount, the better your future returns will be.

This takes us to the next question: How to find the intrinsic value of the company?

Is it the tangible assets the company owns in terms of its factories and offices, or is it the cash that the company has in hand?

What about technology companies like Google? Is their intrinsic value determined mostly by the number of users who are using their products?

Estimating The Intrinsic Value Of A Company

Economists Irving Fisher and John Burr Williams, many decades ago, described a highly valuable way that can be used to estimate the intrinsic value of a company’s stock.

It goes as follows:

The value of a stock is equal to the present value of its future cash flows.

Let me explain this better, step by step.

The money that a company generates is grossly used in the following:

- Pays operating expenses

- Reinvested to expand the business

- Left as Free cash flow

Why Free Cash Flows Are Gold

Free Cash Flow of a company is an extremely important indicator of the company’s financial status.

It is all the amount of money that can be taken out of the business each year without harming its operations.

Free cash flow can be used by a company to:

- Pay a dividend

- Buy back stock which reduces the number of shares outstanding and thus increases the percentage ownership of each shareholder.

- Retain and reinvest in its business

According to Fisher & Williams, these free cash flows are what gives the company its intrinsic value.

Now that you know what the cash flows mean, let’s learn what is meant by: the Present value of its Future cash flows.

Imagine this first. You plan to go on holiday this week but you get a call from your boss. Your current project is struggling and it needs your help.

Your boss asks you to stay in.

You’re a bit annoyed.

But to make the offer lucrative, your boss offers you 2 extra weeks of vacation time, 3 months later!

The offer doesn’t seem too bad now!

Wonder why this happened?

This is because the value of taking a vacation in the future is less than the value of taking it today.

There is always a risk involved — What if your boss refuses at a later date, or he gets fired or what if your employer goes bankrupt?

So you discount the future vacation time in your mind and the extra 2 weeks is the risk premium your boss pays to compensate for it.

In other words, the discounted value of the vacation today is 2 weeks more than the vacation time 3 months later!

“Bird in the hand is worth two in the bush”

The same principle applies when investing in the stock market.

Let’s say that you have money in your bank right now that you want to invest.

The value of this money is always more than the money that you will get in the future as investment returns. (This is called the Time value of money.)

There is also always a risk that you might not get an investment return in the future. So you always add in a risk premium that makes you indifferent to getting money in the future rather than having it today.

A Discount Rate represents this risk premium.

Calculating Present Value Of Future Cash Flows

This discount rate helps us calculate the present value of the company’s future cash flows.

Time for some maths!

The present value or discounted value of future cash flows is calculated using the following formula:

where:

DCFis the discounted value of the future cash flowsCF(1) is the cash flow for year 1CF(2)is the cash flow for year 1CF(n)is the cash flow for the yearnris the Discount rate

Let’s say that a company’s cash flows are $100 each year for the next 10 years but you want to know its value today.

Using a discount rate of 10%, the above-mentioned formula will result in $614.46.

This means that by applying a discount rate of 10%, you’ve determined that an investment offering $100 each year for 10 years is worth $614.46 to you today.

In other words, if you can invest elsewhere at a 10% return, you’d be willing to pay no more than $614.46 right now for a promise of receiving $100 annually for the next 10 years.

This can be a bit confusing to understand but keep holding on!

How To Determine The Appropriate Discount Rate

The discount rate is determined by the:

- amount

- timing

- riskiness of a company’s future cash flows

The higher these factors are, the higher the discount rate that you put on that stock’s buying price.

The following types of companies should be discounted more in general:

- Small market cap

- Cyclical business

- Higher debt-to-equity ratio

- Narrow and shallow Economic moat

- Newly founded companies

The discount rate should be at least the rate of returns for the government bonds (i.e. 4–6% per annum) which are relatively risk-free.

But practically speaking 10–15% is a good discounting rate to consider.

Calculating Perpetuity Value & Discounting It To The Present

Remember the company that we talked about in the previous example, whose cash flows were $100 each year for the next 10 years?

How do we calculate its discounted cash flows after year 10?

Companies can last forever and we cannot keep calculating the discounted cashflows for it for ‘forever’.

Therefore we used something called a Perpetuity value to calculate the cashflows of a company in the very very long term.

For our example company, we can assume that from year 11, it will grow constantly at a lower rate in the very long term (till perpetuity).

To estimate the cash flow from year 11 onwards (till perpetuity), we use the following formula:

Perpetuity Value = FCF (10) x (1 + g) / (R — g)

where:

FCF(10)is the free cash flow at year 10gis the long-term growth rate of the companyRis the discount rate

g is usually considered to be 2–3% as this is the average long-term growth of the US GDP.

Next, we discount the Perpetuity value to the present using the following formula:

Discounted Perpetuity Value = Perpetuity Value / (1 + R) ^ n

where n represents the number of years into the future when the perpetuity begins (10 in our case).

Calculating The Intrinsic Value

In the next step, we sum up the discounted perpetuity value to the sum of the 10 discounted cash flows to calculate the Total Equity Value for the company.

We divide this figure by the total number of shares outstanding for the company to obtain the Per-Share Intrinsic value of the company.

Per Share Intrinsic Value = Total Equity Value/ Total Shares Outstanding

Oh! That was a lot of calculations. But hold on, this will pay off really well!

The overall model that was described above is called the Discounted Cash Flow (DCF) Valuation Model.

Now we will take an example of a real-world company and estimate the intrinsic value of its stock.

How about Apple?

Steps To Calculate The Intrinsic Value of Apple’s Stock

Step 1: Forecast The Free Cash Flows For The Next 10 Years

Apple’s Free Cash flow growth for the last 10 years has been approximately 9% per year. (Source)

For the year 2022, the free cash flow was $111,443 (millions)(Source).

If we expect the cash flows to grow at the same rate for the next 10 years, the projected cash flows can be calculated as below (figures in millions).

Year 2023: $121,472.47 Year 2024: $132,405.09 Year 2025: $144,321.55 Year 2026: $157,310.49 Year 2027: $171,468.24 Year 2028: $186,900.58 Year 2029: $203,721.63 Year 2030: $221,956.98 Year 2031: $241,733.12 Year 2032: $263,189.10

Step 2: Discount The Projected Free Cash Flows To Calculate Their Present Value

Let’s discount them to find the present value of these future cash flows.

Discounting at the rate of 10%, this figure totals approximately $865,279.15.

The breakdown of discounted cash flows is shown below (figures in millions):

Year 2023: $110,429.52 Year 2024: $109,904.65 Year 2025: $106,420.74 Year 2026: $104,014.16 Year 2027: $100,644.24 Year 2028: $96,493.92 Year 2029: $91,848.76 Year 2030: $86,835.33 Year 2031: $81,596.05 Year 2032: $76,282.04

Step 3: Calculate The Perpetuity Value

Next, we calculate the perpetuity value from year 11 onwards as follows (figure in millions):

Perpetuity value = FCF (2032) × ( 1 + 0.03 ) / (0.10–0.03)

Perpetuity value = $263,189.10 x 1.03 / 0.07

Perpetuity value = $3872639.6

Step 4: Calculate The Perpetuity Value Discounted To The Present

In the next step, we discount it to the present (2022) at a 10% rate (figure in millions).

Discounted Perpetuity Value = $3872639.6 / ( 1 + 0.10 ) ^ 10

Discounted Perpetuity Value = $1,487,080.63

Step 5: Calculate The Total Equity Value

Next, we calculate the Total equity value of Apple by adding the 10-year discounted cashflows and discounted perpetuity value as follows (figure in millions).

Total Equity Value = $865,279.15 + $1,487,080.63 = $2,352,359.78

Step 6: Calculate Per Share Intrinsic Value

The per-share intrinsic value of Apple’s stock is calculated by dividing the above figure by the total shares outstanding (i.e. 16,326 million in 2022).

Per-share Intrinsic Value = $2,352,359.78 million / 16,326 million = $144.10

Note that because we have taken a highly conservative approach to evaluating the stock, the final per-share intrinsic value is an approximate (but important) estimate of a company’s real worth.

Also, a little disclaimer that this article is for educational purposes only and is not formal financial/ investment advice.

If you found the article valuable and wish to offer a gesture of encouragement:

- Clap 50 times for this article

- Leave a comment telling me what you think

- Highlight the parts in this article that you resonate with

{kind=link}