The Psychology Behind Certain Stock Market Decisions

We hate to lose

I’m a sucker for psychology; it’s one of my “stretch interests” that I wish I knew more about. While I never got the chance to take a course in undergrad on the subject, I have something even better — books written by psychologists. I can learn on my own time and it's way cheaper.

I’m currently reading The Paradox of Choice by Barry Schwartz. One section in particular stood out to me and as soon as I read it, I related it to my own experiences with trading / short-term investing. The section is about prospect theory and how we take greater risks not to lose money than risks to make money.

On a side note — I haven’t finished the book yet, but so far would highly recommend it.

Prospect Theory

Prospect theory explains how people decide between alternatives that involve risk and uncertainty. Prospect theory states that decision-making depends on choosing among options that may themselves rest on biased judgments.

The theory shows that people would rather keep what they have than risk the chance to increase their wealth, which is why the theory is sometimes referred to as the loss-aversion theory.

An important element of prospect theory is the idea that individuals are particularly averse to losing what they already have and less concerned to gain. Given a choice of equal probability, individuals would choose to preserve their existing wealth, rather than risk the chance to increase wealth.

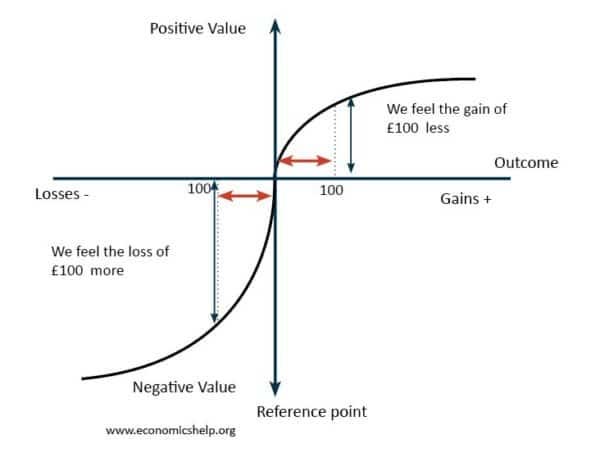

The classic example used is between gaining and losing $100 or $200. The theory shows that if you ask people if they would rather have $100 or flip a coin and get $200 if the coin is heads and $0 if the coin is tails, most would choose the $100. On the other side, if people were asked if they would rather lose $100 or flip a coin to decide if they lose $200 or $0, most would elect for the coin flip.

This perfectly illustrates that we take greater risks to avoid losing what we already have.

People are risk-averse when it comes to potential gains BUT are risk-seeking when it comes to potential losses.

It's important to note on the chart below the loss portion of the graph is steeper than the gain portion. Losing the $100 produces a feeling of greater intensity than gaining $100.

In short, we hate to lose.

It’s also important to note the line is not a straight linear line. This is due to the law of diminishing marginal utility and the decreasing marginal disutility of losses. Gaining the first $100 feels better than the second $100. Losing the first $100 hurts worse than the second $100.

According to the graph, we would have to be offered the option of gaining $100 or the chance of ~$240 on the coin flip for you to choose the coin flip.

Real-Life Studies

There are two studies Schwartz talks about in the book supporting this theory.

The first example relates to research done by Ziv Carmon and Dan Ariely. The study involves students from Duke University and tickets to the men's basketball championship game Duke was playing in. Duke held a lottery to determine which students would get tickets to the game. After the lottery, students who did not win a ticket were asked how much they would be willing to pay for a ticket compared to those that did win a ticket who were asked how much they would sell theirs for.

The students that did not win a ticket said they would pay $175 for a ticket to the game. The students that did win a ticket said they would have to be paid $2,400 to give up their ticket.

That more than $2,000 difference shows students who had no ticket would only pay a small amount to gain the ticket. Compared to the students with tickets, who would need a lot of money to be alright giving away their ticket.

The second study was related to car buying decisions under two conditions. In the first condition, the car was loaded with extra features and buyers had to eliminate the features they didn’t want. In the second condition, the car had no optional features and buyers had to add on the ones they wanted.

Since we’ve established losses hurt more than gains satisfy, giving up a stereo upgrade hurts more than its cost but choosing to add in the stereo when it was not originally there will likely not be worth the cost. In the end, buyers who faced the loaded cars left with more features in their cars than those who started with none.

Applying it to the Stock Market

It's pretty easy to see how this theory can apply to investing. We are willing to take a greater chance of losing money on an investment than we are gaining money. Shouldn't it be the opposite way?

I have recognized this in my time day trading and investing short-term. Now I’m glad I know what it's actually called.

I use to be willing to take a greater loss on a trade with the hopes of it rebounding, compared to when a trade is up, I am happy to sell for a small gain.

Losing 10% on a stock has a greater impact on us than gaining 10%. In order for us to feel the impact of the 10% loss, we would need a gain that’s greater than 10%.

Because of this theory, it’s important to establish and stick to your sell prices. If you decide before investing you only want to lose a maximum of 8% on a trade, once it hits 8% you need to sell and not hold on. And the same goes for gains, if you decided before investing you wanted a 6% gain, wait for the 6% instead of selling at a profit beforehand. Emotions get too involved when short-term investing or trading, which is why it's always important to have a plan before each trade.

It's also another reason why I no longer day trade or do much short-term investing, I’m all in for the long run now!