Power of Compound Interest — a Mathematical Deep Dive

The Secret Sauce Behind Financial Independence

Albert Einstein is reputed to have said:

“Compound interest is the eighth wonder of the world. He who understands it, earns it — he who doesn’t, pays it.”

Appreciating the life-changing power of compound interest can transform your life, whether you’re scaling your startup or investing for financial independence.

Edit: See sequel articles here and here, and relevant videos on my YouTube.

1. Compound Interest = Exponential Growth

Many people mistake compound interest for simple interest, which grows your assets linearly. Compounding assets grow exponentially*, which mathematically skyrockets their value. This effect is dramatically enhanced by the interest rate (i.e. exponent) and time in the market.

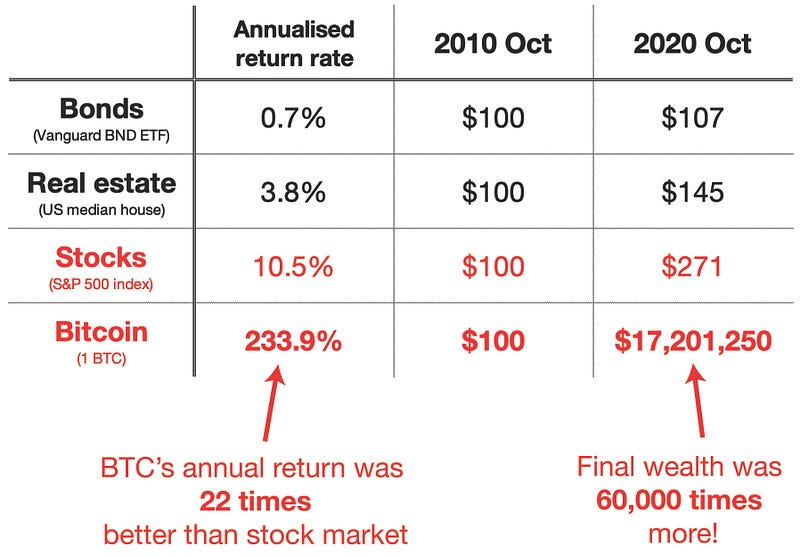

Consider putting $100 into a variety of asset types in 2010. Even though Bitcoin’s annualised return rate — at 230% — was a crazy 22 times more than the US stock market average of 10.5%, your wealth snowballed way more than 22 times that over a period of ten years. We’re talking a difference of millions of dollars versus just a few hundred bucks in your wallet. The story gets even better with some of the other large cryptocurrencies.

That’s the power of compound interest.

New to Medium?

Join here and gain unlimited access to the best crypto & investing articles and guides on the internet.

*Actually, compound growth is geometric, not exponential, but the ideas are very similar.

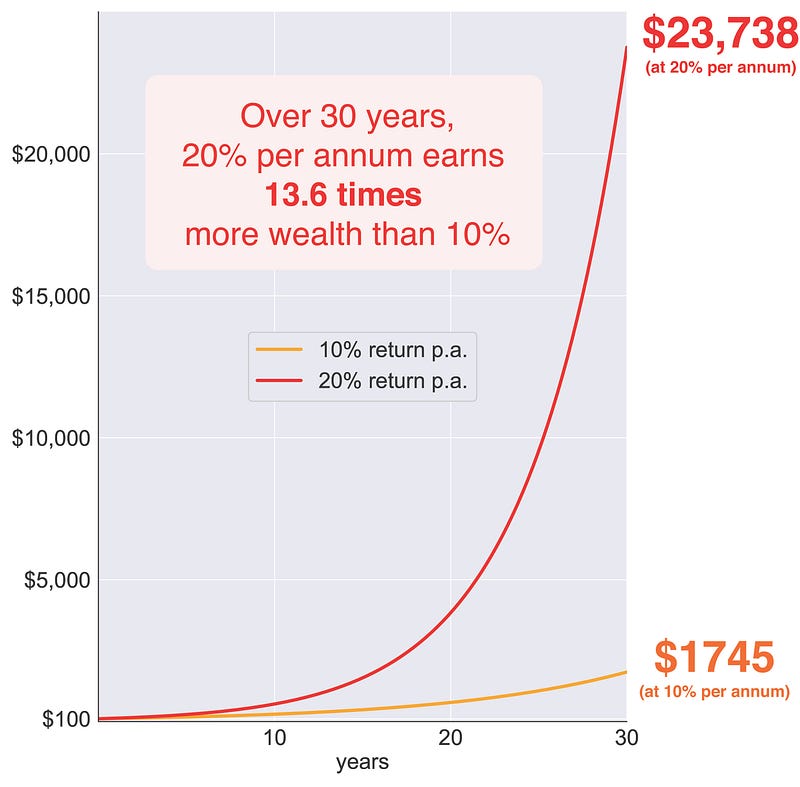

Rate of Return makes a big difference

If you double your rate of return, you’ll way more than double your returns.

The reason for this is two different exponential functions diverge away from each other quickly.

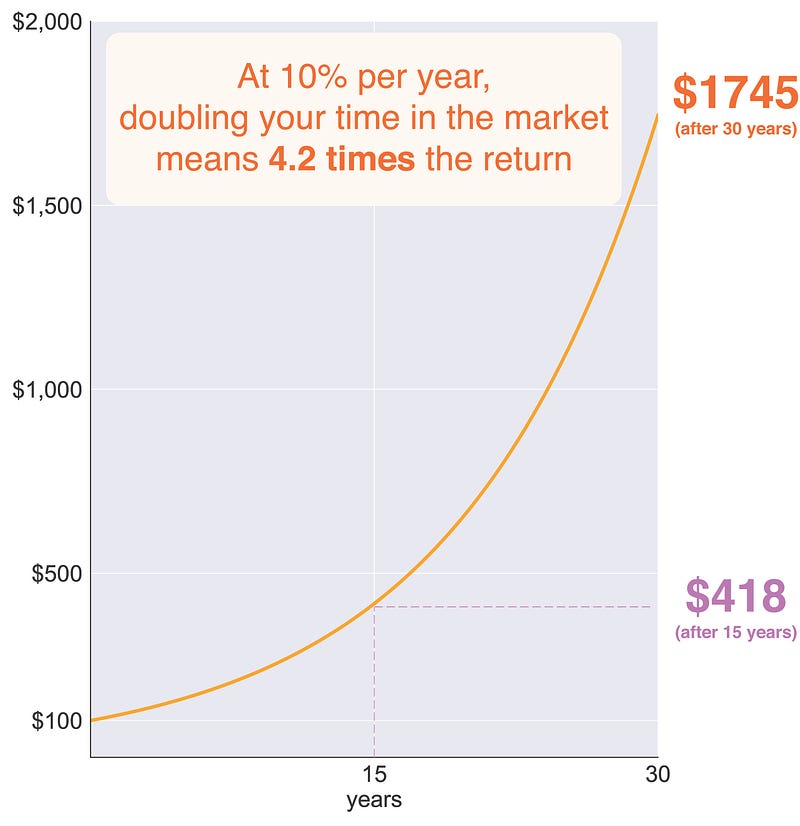

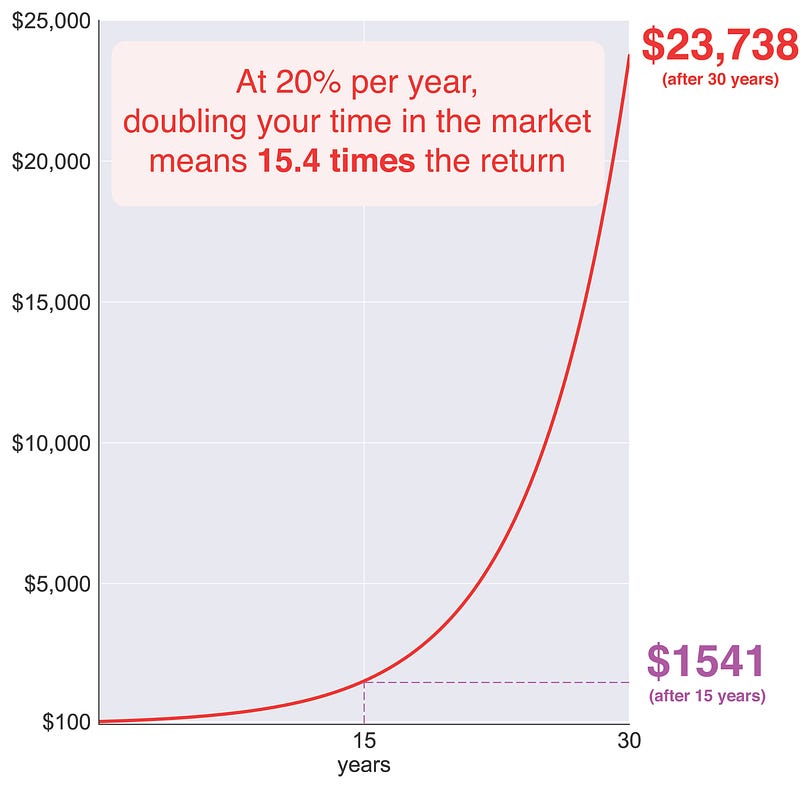

Time in the market makes a big difference

If you double your time in the market, you’ll way more than double your returns.

The reason for this outcome is the same as above: one exponential function grows way faster than the other — the effect of which becomes amplified as you stay in the market for longer.

Combine this with higher interest rates to further exaggerate the gains. For example, doubling your time in the market at 10% per year already quadruples your wealth after 30 years. But at a 20% interest rate, you’ll 15 times your wealth. Crazy huh! 😎

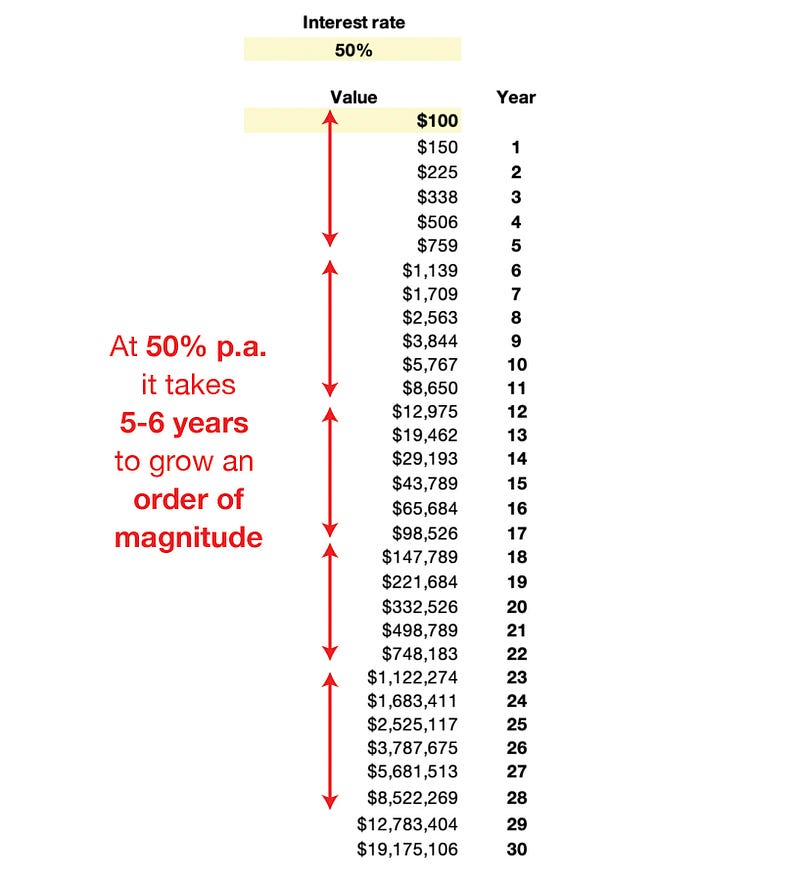

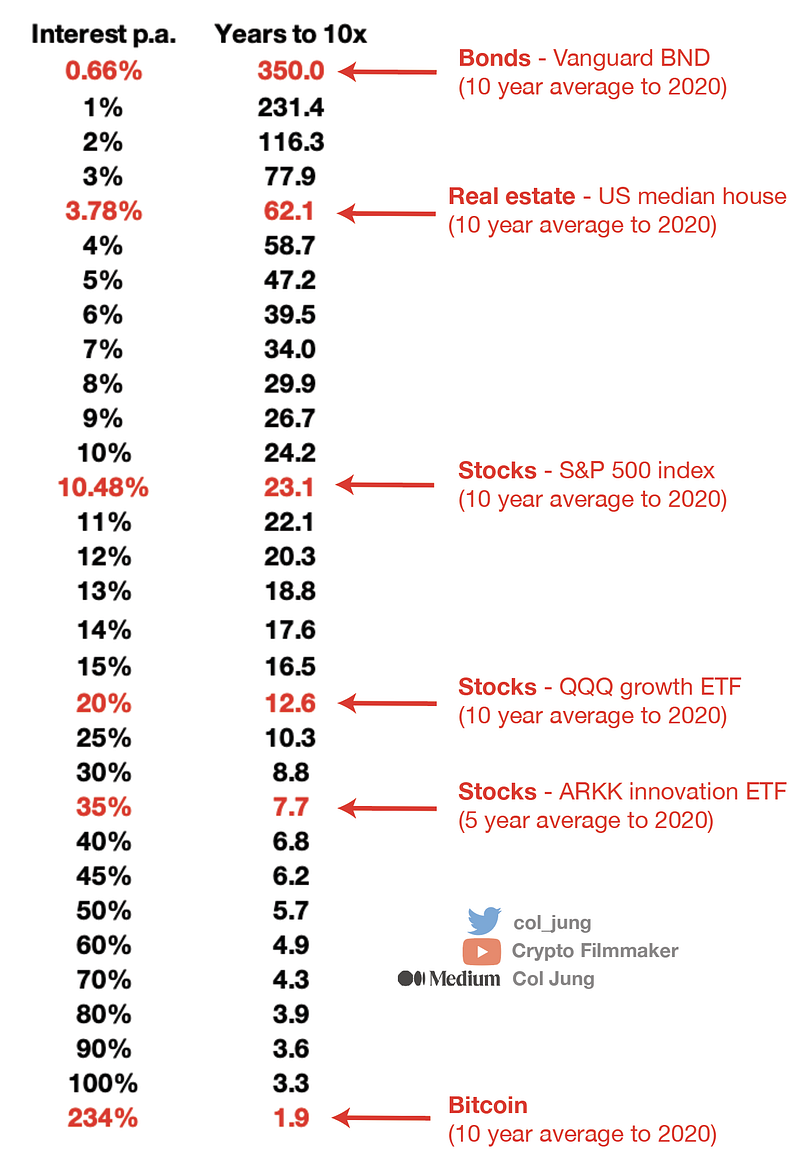

2. Your asset grows an order of magnitude regularly

Fun fact: For any interest rate, it takes roughly the same amount of time for your asset to grow an order of magnitude. This means it takes the same time for the value to grow from $100 to $1,000 as growing from $1,000 to $10,000. Here’s a demo using a 50% interest rate.

Pretty amazing huh. I hope you’re having as much fun as me writing this. 😂

The reason for this is because of the ‘memoryless property’ of exponential functions. This means it takes the same amount of time for an amount to double, triple, ten-fold, and so forth, regardless of the starting principal. In the case of ten-folding at 50% p.a., that time is always 5–6 years.

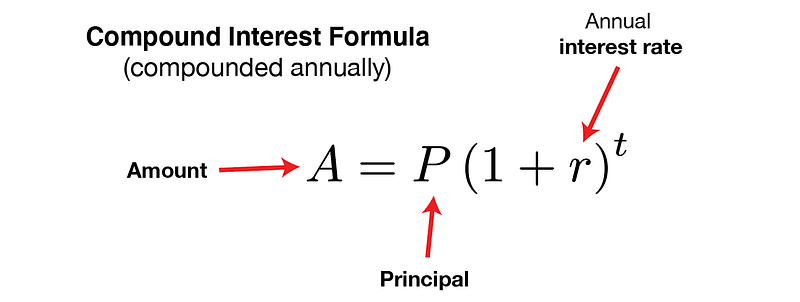

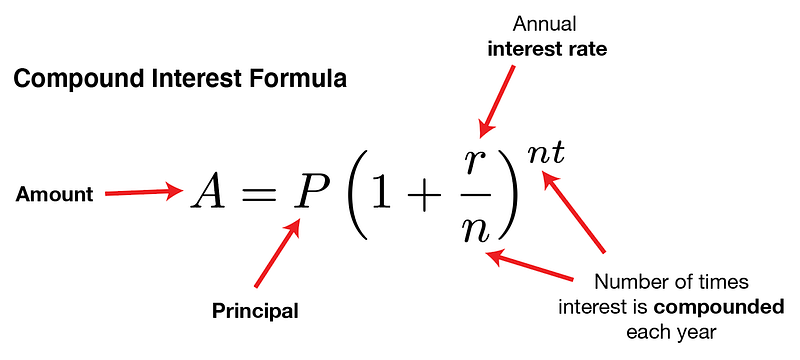

Let me show you. Here’s the formula for annualised compound interest.

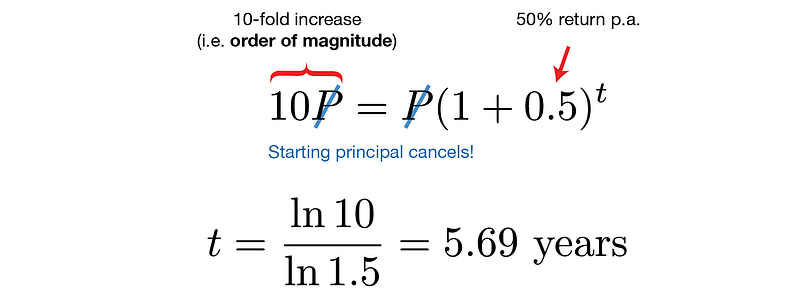

For any starting principal P, let’s find out how long it takes to go up an order of magnitude at 50% interest rate.

Because P cancels away, the time taken will not depend on our starting amount. A-hah! 🍿 Rearranging the compound interest formula for t shows that it takes 5.7 years to compound our way to a ten-fold increase, whether we start with $100 dollars or $100 million dollars.

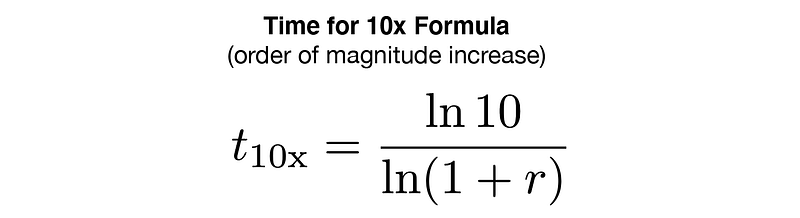

In general, the time taken to snowball your wealth an order of magnitude is:

For a variety of interest rates, here are the number of years you’ll need to wait to 10x your investment.

If this doesn’t make you wanna pull your money out of your ordinary savings account (earning 1% p.a. or less) into an investment account (thus making your money work for you big time), I don’t know what will! 😩

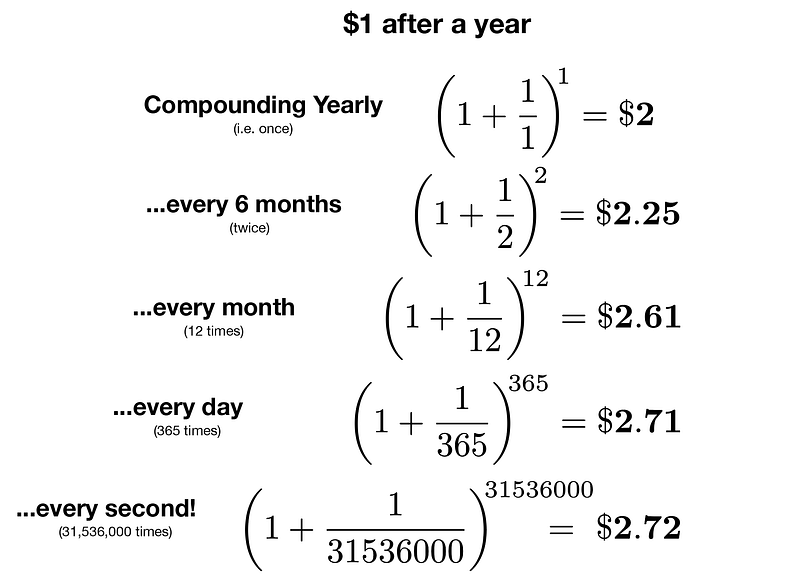

3. Compound Frequency = Diminishing Returns

Another fun fact: There’s a limit to how much extra money you can earn by having your bank balance compounded more frequently. In fact, the difference between compounding daily and every second is almost negligible.

Let me show you. Here’s the formula for compound interest, taking into account multiple compound periods each year.

Now suppose you’ve got $1 in the bank that earns 100% per year. Then P = $1, r = 100% = 1 and t = 1 year.

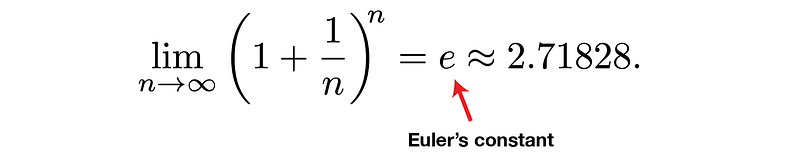

We see that there’s diminishing returns, followed by what appears to be a ceiling. In fact, this ceiling is known as Euler’s constant, one of the most important constants in mathematics, alongside π and i.

The moral of the story is if your balance is being compounded monthly, that’s pretty good already.

4. Stock market Tips. Investing is easy. Emotional discipline is hard.

Since many readers are stock market investors, I want to finish off by giving some tried and true tips on investing in the stock market.

The biggest epiphany is realising that you don’t need to be an expert, because the simplest and easiest things to do are often more profitable than trying to be too clever.

In short, just do the following:

- Regularly put disposable cash (dollar-cost average) into

- an ETF index fund like VOO (S&P 500) or VTI (entire US market); and

- hold for decades (time in the market is king).

This will get you an average 10% return in the long term and you’ll be well on your way towards building a solid nest egg. It really is that easy.

Let’s dig into how we reach the above enlightenment.

Time in the market > Timing the markets

In the stock market, the basic premise is you want to open a position during the dips and sell during the highs. The problem is, it’s very hard to know when the lows will be. This results in poor decision-making and two types of emotional behaviour by the majority of investors.

- Panic selling — selling a tanking stock in panic, when it’s probably just a temporary pullback. The stock quickly recovers, and you wish you had just kept those itchy fingers away.

- FOMO-in — joining the bandwagon on a growing stock because it’s hot. But often you’ve already missed the boat, and before you know it, suddenly there’s a big correction. Whoops. This then feeds into panic-selling, when the correction’s probably just temporary. Can you see how easy it is to lose money if you don’t rein in your emotions?

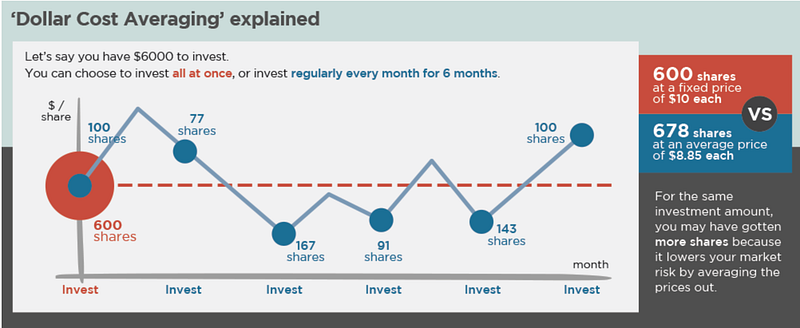

Instead of timing the market, you want to dollar-cost average. This means every every at every pay check, put a little bit of money into the markets. On average, you’ll end up with more shares than trying to time your way into the best deal of the century.

And finally, you want to hold your positions for a long time so that compound interest can do its magic and snowball your wealth.

Volatility in prices are natural. The stock market rewards you for taking on this volatility risk (quantified stock’s beta measure) by giving you a positive expected return, which just requires you to sit on your investments for a long time to guarantee a safe return.

For example, on average the S&P 500 dips every four years. However on average, the index has returned an average 10% since the 1920’s. In fact, the S&P 500 has had a positive return for every 20 consecutive year period in history.

As a long-term investor, you don’t lose money until you close the position. As long as you’re investing in companies with solid balance sheets and great fundamentals, your investments will rise in the long-run.

Try to think like this:

- When stocks rise, you make money → you win.

- When stocks dip, you can buy more at a bargain → you win.

This is an especially easy mindset to get into if you dollar-cost average.

Buy ETF index funds

Various studies have shown that for the vast majority of investors, buying a basket of companies in an ETF index fund outperforms managed mutual funds and picking your own stocks. Like driving, people regularly overestimate their own expertise.

The premise behind diversification is as follows:

- You pick a stock you think is amazing. But the average micromanager investor 1) overestimates their ability; 2) don’t adapt when company fundamentals, competition dynamics or economic conditions change; and 3) at times let their emotions get in way and panic sell or FOMO-in. In other words, there’s a good amount of risk.

- To compensate, you pick a second stock that you also think is amazing. But the same problem inherently exists.

- Pick a third. A fourth. A fifth. But that risk remains while you continue to hold a relatively small basket of stocks.

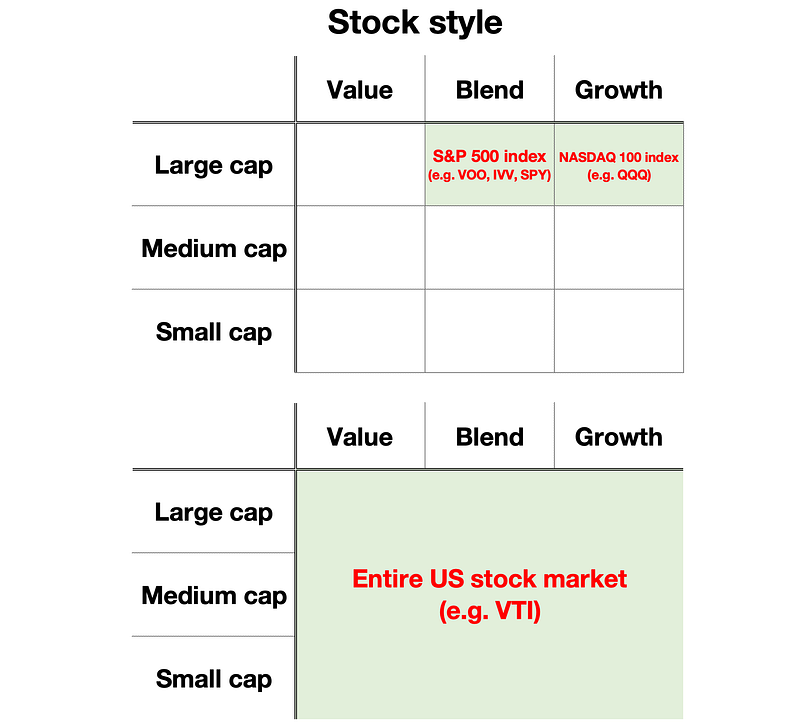

- This gives rise to the idea of an ETF index fund, like Vanguard’s VOO, which tracks the S&P 500 index (500 biggest American companies based on market capitalisation), VTI (full basket of all tradable stocks on the US stock market — over 3,000 stocks) or QQQ (which tracks the growth-oriented tech-heavy NASDAQ index).

Summary

Every compounding interest rate corresponds to its own exponential curve when graphed.

Because exponential curves can diverge away quickly from each other, a higher interest rate and a longer time in the market has drastic effects on the growth of your wealth.

Also, exponentially-growing quantities take the same amount of time to jump an order of magnitude, so you’ll see your investments grow from $1,000 to $10,000 as quickly as it did growing $100 to $1,000.

Finally, don’t get angry at your bank for not compounding your balance daily. You’re not gaining a huge difference over a monthly compound frequency.

These profound concepts about compound interest can be applied to rapidly expanding startups in an environment with little competition.

I also discussed stock market investing.

In short, you want to stay in the market for a long time, rather than try and time your entry into the markets. To prevent mistakes from poorly timed entries, invest frequently in small amounts (dollar cost averaging). To manage risk, invest in ETF index funds that diversify away the chances of picking bad individual stocks.

What’s a good fund to start with? The S&P 500 index has provided an average annualised return of 10% since the 1920’s, which as we saw earlier quadruples your money over 30 years. Nice! The main S&P 500 ETF funds are VOO (from Vanguard), IVV (from BlackRock) and SPY(from State Street).

If you’re a more active type of investor who enjoys fundamental and technical analysis, take a look at individual stocks; growth ETFs like the NASDAQ-based QQQ and innovation-centric ARKK; and other asset classes, like bitcoin and other cryptocurrencies.

In fact, the power of compound interest is probably the most obvious for high-growth assets precisely like crypto, enabling investors to generate strong passive income with a smaller principal. Again, feel free to check out my guides here and here.

Tools for Diagrams and Plots

I used

- Python (Matplotlib and Seaborn packages) to generate the plots.

- Adobe Illustrator for extra labelling.

- LaTeXiT for math equation and symbol labelling.

- Microsoft Excel for the tables.

Follow me on Twitter & YouTube for regular analyses and guides.

My Crypto Articles

- Unlock unlimited access to Medium by joining here.

- When Will the Bear Market End? Macro 101 for Crypto Investors

- A Review of the Cryptocurrency Market in 2022

- Web3 Gaming — What do Crypto, NFTs & Metaverse offer?

- FTX’s Collapse & Solana’s Long-term Impact

- Polygon & Solana — 6 Killer Crypto/NFT Use Cases

- A Brief History of NFT Marketplaces

- Compound Interest is the 7th Wonder of the World

- How to Generate Passive Income with Crypto

- Crypto Passive Income on BNB Chain

- Move & Earn Crypto — 6 Month Review of STEPN

- PancakeSwap’s High APY Pools — What’s the Catch?

- Cardano, Avalanche, Solana Staking Guides (2022)

- Cardano, Avalanche, Solana Price Predictions (Bull Market)

- How to Make Crypto Price Predictions

- Top 3 Price Prediction Mistakes

- Crypto VISA Cards — Cashbacks for Every Purchase?

- How to Build Wealth like Smart Money

- Is Crypto.com’s Earn Program Worth It?

- Understanding Terra’s Anchor Protocol

- How to Participate in Initial DEX Offerings

- Memecoin Speculation — Is It Worth It?

- Why SHIB Can Never Reach $1 (or even close)

- Want to Retire Early? Buy Bitcoin

- Democrats vs Republicans — Which Party Better for Markets?