TandaPay DMCA Legal Defense Funds

How peer-to-peer insurance can be used to protect Youtube creators from abusive DMCA claims.

💢😡Youtube Copyright Content ID System😡💢

Not a very popular feature on Youtube right now judging by the number of videos and articles produced about this issue. I had no idea that peer-to-peer insurance could potentially provide a solution to this issue until I heard this:

Thank you to our channel sponsor Joshua Davis from TandaPay. We are working on a longer video or even videos about TandaPay. (TandaPay) is kind of a cool way that communities can insure themselves (against) problems of that community foresees (being an issue). For example maybe there could be a (TandaPay group) for people who receive false DMCA claims. (Rather than using crowdfunding to provide a legal defense) people who were susceptible to false DMCA claims, like Youtuber’s Union, may all put a small amount of money into a monthly tanda and then if someone has a claim (lit. gets hit) then (the TandaPay group) can pay out (a claim) to those people (as a way of providing) a legal defense fund. It’s a it’s a strange concept but we think it’s actually a very powerful and positive concept for change.

I feel bad for content creators who are negatively impacted by this issue. At the same time I’d be dishonest if I were to misrepresent my initial reaction upon hearing this which can best be described as “intrigued.”

First let’s understand the problem

Let me explain, so I’ve been working on an architecture for peer-to-peer insurance called TandaPay for nearly 1 and 1/2 years. This is my 4th and final attempt at trying to solve this problem over the past 5 years. Many of my friends and family have watched with some amount of dismay as I took my crypto fortune and spent it entirely on solving this problem. Now all my crypto wealth is gone and I’ve nothing except TandaPay to show for it. Furthermore, most people think that TandaPay is a really poor protocol for insurance. The problem with TandaPay is that it seems to only work in very niche use cases.

Without some special context it’s difficult to imagine that P2P insurance has a valuable use case. Why would people want to participate?

The use cases I’ve found up till now have all had their issues. Here’s a quick review:

- The $500 auto insurance deductible: The people who stand to benefit the most are the people who don’t have $500 in their bank account or easy access to credit. These people usually don’t plan or save for their future… so it’s hard to see how they might become customers who purchase insurance.

- Coverage related to social justice issues: Issues relating to police brutality, sexual assault or unsafe work places (workers’ comp). TandaPay might be useful in these circumstances but there isn’t universal agreement as to how communities should decide these issues. Furthermore, no one believes that insurance would be a potential solution.

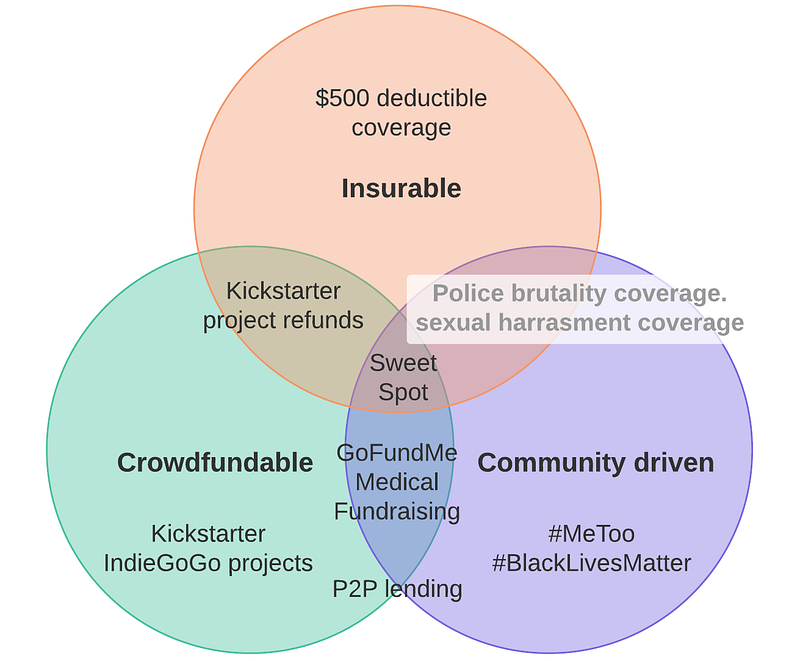

Its a leap to conceptualize using insurance to cover some liability that has never previously been associated with insurance. Even if insurance tied to social justice issues seems interesting, most people can’t imagine that you could actually insure this type of risk. If we take a look at this Venn diagram you can see that finding the sweet spot is very difficult:

The takeaway is this:

- The $500 deductible is not seen as a problem which is solved by either communities or crowdfunding. Historically however this has always been the type of unexpected cost for which people have used Tandas.

- The police purchase liability coverage to manage the risk of litigation for police brutality. But, can you imagine yourself purchasing police brutality insurance?

- Corporations purchase liability coverage to manage the risk of litigation for sexual harassment claims. But, can you imagine yourself or your spouse purchasing sexual assault insurance?

If people can’t imagine themselves creating a GoFundMe campaign to raise money for an issue after it happens then it is unlikely that they can imagine purchasing insurance for an issue before it occurs.

Why DMCA false claims legal defense funds make sense

Some interesting points I was considering recently with regard to this issue:

- Chances are that if you have more than 100 K subscribers you’ve either dealt with this issue in the past or will deal with it in the near future.

- Almost everyone thinks Youtube’s DMCA claims system is broken.

- It’s been broken for about a year or so and the situation hasn’t improved.

- While under attack a content creator may lose some or all of their revenue stream.

- The amount of time required by a creator to respond to an attack means they can’t create new content.

- These two factors can result in a temporary but significant financial hit.

- Content creators might be willing to pay a nominal monthly fee to recover some of their lost income when dealing with this issue.

- We have seen how solidarity among the Youtube community on social media has provoked Youtube to helping creators reach faster resolutions. This is something a traditional insurer could never provide.

- The most qualified people to judge if a DMCA claim is justified or abusive is other content creators on Youtube. This means that their knowledge as to this issue provides a type of skill based arbitrage. This is due to the relative cost of a claim evaluation between a community of Youtube creators and a traditional insurer. The community has much lower claim evaluation costs than a traditional insurer would, who lacks this expertise.

- Traditional insurers won’t provide coverage to content creators for this type of risk. Even if they did, a community of peers would be able to out perform a traditional insurer by offering the same service at lower costs.

Tandas are communities that come together for mutual aid and protection. The issue of false DMCA claims seems to be a perfect fit because:

- It is conceivable that someone might want to pay a premium to gain protection when their channel comes under attack. People can conceive of an insurance product covering loss caused by false DMCA claims.

- People have created crowdfunding campaigns on GoFundMe and IndieGoGo so that channels can raise funds from supporters to respond to this issue. See the following: Ammobox Studios Legal Battle Help Addison Cain with her legal defense! Second Mallory Video Gala Phoenix Legal Fund

- The community of content creators are closely aligned in their values and beliefs. It’s completely realistic to think that they would want to form these types of groups.

- Almost none of the content creators believe that there is any controversy with regard to determining which claims are valid. It is universally accepted that the DMCA claims system is being abused. This allows for faster resolutions when evaluating claims.

- Its fairly easy to check if a claimant has a valid claim because all the relevant information is either online or can be easily captured via screenshots and video screen captures.

- There is greater power in numbers and in solidarity. TandaPay would simply be a tool for these communities to coordinate, share information and reach a joint response when someone is attacked.

- Since traditional insurers won’t cover this risk, the only reasonable way people might be able to obtain coverage would be via P2P insurance.

Conclusion

Not all risks can be covered by traditional insurers. Sometimes this is because there isn’t a market for an insurance product which could guard against non-traditional risk. Other times this is because traditional insurers can’t move quickly enough to respond to changing markets. Community insurance can guard against non-traditional risks and it is flexible enough to move quickly in response to changing market conditions. The change in Youtube’s DMCA policy is fairly recent and it is unknown how long it will be until the system is better aligned to content creators. The window where these types of policies are valuable may be brief. Knowing this a traditional insurer would never develop products for this type of risk. This suggests that there are many risks traditional insurers will never cover, which implies there are likely many uses for community insurance which simply haven’t been discovered yet.

What you can do

If you want to help and you know something about this issue please consider providing answers to the questions that will help me make this product better: