Strategic Asset Allocation (SAA) & Portfolio Optimization (PO): Go-To’s for Quants

- This paper represents an in-depth analysis of the Strategic Asset Allocation (SAA) and multi-criteria Portfolio Optimization (PO) methods as a well structured collection of implemented and tested quant trading algorithms in Python.

- The SAA process aims to monitor that the portfolio meets the long-term return and risk targets.

- The PO process selects the best possible combination of investment portfolio assets and their weights.

- The primary goal of both processes is to maximize return while minimizing risk.

Data Science in SAA/PO

- Data science plays a pivotal role in optimizing portfolios and and managing various types of financial risks, including market risk, credit risk, and operational risk.

AI for Quant Trading (AI4QT):

- The objective of AI4QT is to develop a holistic SAA framework by incorporating AI-powered data science [5] into risk-adjusted portfolio optimization (PO) strategies [6,9].

- The idea is take on board key features of the recently released PythonFinanceAI [1–4]. This is a standalone repository that provides insights into various fintech solutions [5, 8], ranging from basics of financial analysis [11] to advanced investment portfolio management algorithms such as Alpha Research and Smart Beta PO.

Algo-Trading Strategies

- This article seeks to provide an in-depth understanding of momentum and breakout trading strategies. These two popular strategies are both dependent on technical analysis.

- Momentum trading involves making investment decisions based on the current market trend.

- Breakout trading is a strategy where investors buy a security when its price moves outside a defined support or resistance level with increased volume.

Fundamentals vs. Technicals

- Fundamental analysis attempts to identify stocks offering strong growth potential at a good price by examining the underlying company’s financial health.

- Technical analysis, on the other hand, looks for statistical patterns on stock charts that might predict future price moves.

- Our goal is to find out how quants can use these two stock-picking strategies together.

Altman Z-Score

- Typically, fundamental analysis is used to assess a company’s value. Here we will provide the Altman Z-score [12] that estimates the likelihood of a company’s bankruptcy.

Let’s delve into the specifics of the aforementioned fintech projects and algorithms.

Alpha Research & Factor Modeling (Portfolio 1)

- In this section, the focus is on the Alpha Research and Factor Modeling strategy (cf. [7, 10]), viz.

- Build a statistical risk model using PCA along with 20 alpha factors.

- Evaluate the factors using factor-weighted returns, quantile analysis, and Sharpe ratio.

- Multiple PO using the risk model and factors.

Scope

- Part 1: Fetching Stock Data and Getting Returns; Part 2: Statistical Risk Model; Part 3: Create Alpha Factors; Part 4: Evaluate Alpha Factors.

- Let’s consider the 5Y Portfolio 1 of 43 stocks

ticker_list = [

'AAPL', 'ABBV', 'AMGN', 'AMZN', 'AXP', 'BA', 'BIIB', 'BMY', 'CAT', 'CMCSA', 'CSCO', 'CVX', 'DD', 'DIS', 'F', 'GE', 'GILD', 'GM', 'GOOGL',

'GS', 'HD', 'HON', 'IBM', 'INTC', 'JCI', 'JNJ', 'JPM', 'KO', 'MCD', 'META', 'MMM', 'MRK', 'MSFT', 'PEP', 'PFE', 'PG', 'T', 'TSLA', 'UNH', 'V',

'VZ', 'WMT', 'XOM'

]

years = 5

year_end = 2024- Importing the necessary libraries and preparing the input data

# Import necessary libraries

import yfinance as yf

import pandas as pd

from datetime import datetime, timedelta

import numpy as np

import json

import matplotlib.pyplot as plt

Fetching Stock Data and Getting Returns

def fetch_stock_data(ticker_list, years=5, year_end=None):

if year_end is None:

year_end = datetime.now().year

end_date = datetime(year_end, 12, 31)

start_date = end_date - timedelta(days=years * 365)

close_data_df = pd.DataFrame()

open_data_df = pd.DataFrame()

for ticker in ticker_list:

stock = yf.Ticker(ticker)

hist_data = stock.history(period='1d', start=start_date, end=end_date)

# Close Data

close_data = hist_data['Close'].rename(ticker)

close_data_df = pd.merge(close_data_df, pd.DataFrame(close_data), left_index=True, right_index=True, how='outer')

# Open Data

open_data = hist_data['Open'].rename(ticker)

open_data_df = pd.merge(open_data_df, pd.DataFrame(open_data), left_index=True, right_index=True, how='outer')

return close_data_df, open_data_df

close, open = fetch_stock_data(ticker_list, years, year_end)

close.tail()

AAPL ABBV AMGN AMZN AXP BA BIIB BMY CAT CMCSA ... PEP PFE PG T TSLA UNH V VZ WMT XOM

Date

2024-06-14 00:00:00-04:00 212.490005 168.589996 298.619995 183.660004 224.820007 177.270004 231.690002 41.200001 321.470001 37.439999 ... 163.809998 27.530001 166.789993 17.639999 178.009995 495.019989 270.660004 39.669998 67.019997 109.110001

2024-06-17 00:00:00-04:00 216.669998 169.679993 303.279999 184.059998 228.270004 178.389999 226.460007 40.970001 322.399994 37.310001 ... 166.139999 26.980000 167.500000 17.670000 187.440002 489.230011 271.170013 39.459999 67.419998 108.360001

2024-06-18 00:00:00-04:00 214.289993 171.360001 305.989990 182.809998 229.309998 174.990005 223.649994 40.810001 325.140015 36.900002 ... 166.479996 27.410000 168.559998 18.049999 184.860001 481.049988 273.619995 40.080002 67.599998 109.379997

2024-06-20 00:00:00-04:00 209.679993 172.130005 309.890015 186.100006 230.210007 176.300003 225.580002 41.040001 329.130005 37.849998 ... 166.679993 27.740000 167.669998 18.110001 181.570007 484.519989 276.820007 40.240002 68.010002 111.739998

2024-06-21 00:00:00-04:00 207.490005 170.389999 308.160004 189.080002 230.380005 176.559998 224.000000 41.930000 327.839996 38.480000 ... 167.279999 27.740000 168.259995 18.400000 183.009995 482.589996 275.220001 40.240002 67.910004 110.760002

5 rows × 43 columns

close.shape

(1125, 43)

close.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 1125 entries, 2020-01-02 00:00:00-05:00 to 2024-06-21 00:00:00-04:00

Data columns (total 43 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 AAPL 1125 non-null float64

1 ABBV 1125 non-null float64

2 AMGN 1125 non-null float64

3 AMZN 1125 non-null float64

4 AXP 1125 non-null float64

5 BA 1125 non-null float64

6 BIIB 1125 non-null float64

7 BMY 1125 non-null float64

8 CAT 1125 non-null float64

9 CMCSA 1125 non-null float64

10 CSCO 1125 non-null float64

11 CVX 1125 non-null float64

12 DD 1125 non-null float64

13 DIS 1125 non-null float64

14 F 1125 non-null float64

15 GE 1125 non-null float64

16 GILD 1125 non-null float64

17 GM 1125 non-null float64

18 GOOGL 1125 non-null float64

19 GS 1125 non-null float64

20 HD 1125 non-null float64

21 HON 1125 non-null float64

22 IBM 1125 non-null float64

23 INTC 1125 non-null float64

24 JCI 1125 non-null float64

25 JNJ 1125 non-null float64

26 JPM 1125 non-null float64

27 KO 1125 non-null float64

28 MCD 1125 non-null float64

29 META 1125 non-null float64

30 MMM 1125 non-null float64

31 MRK 1125 non-null float64

32 MSFT 1125 non-null float64

33 PEP 1125 non-null float64

34 PFE 1125 non-null float64

35 PG 1125 non-null float64

36 T 1125 non-null float64

37 TSLA 1125 non-null float64

38 UNH 1125 non-null float64

39 V 1125 non-null float64

40 VZ 1125 non-null float64

41 WMT 1125 non-null float64

42 XOM 1125 non-null float64

dtypes: float64(43)

memory usage: 386.7 KB- Examining the descriptive statistics summary of the dataset

close.describe().T

count mean std min 25% 50% 75% max

AAPL 1125.0 143.658611 34.734293 54.632896 123.990799 146.971649 171.161026 216.669998

ABBV 1125.0 120.252841 31.394200 53.663055 93.122742 130.147095 144.791183 180.415100

AMGN 1125.0 229.201625 30.390542 159.913116 208.148529 222.399857 245.879562 319.771271

AMZN 1125.0 141.189915 28.669234 81.820000 116.750000 148.023499 164.868500 189.500000

AXP 1125.0 150.053098 36.689715 64.962784 127.278458 153.474594 167.936493 243.080002

BA 1125.0 199.101303 41.000993 95.010002 173.160004 202.720001 218.759995 345.395020

BIIB 1125.0 264.431298 40.002559 187.539993 231.990005 267.869995 286.540009 414.709991

BMY 1125.0 58.363579 7.720472 40.207870 52.710373 57.102249 64.020714 76.548782

CAT 1125.0 207.083070 62.089769 83.515442 172.211151 203.556000 236.764145 377.922363

CMCSA 1125.0 41.974927 6.296697 27.474335 37.743309 41.433960 46.057053 57.373844

CSCO 1125.0 45.861873 5.738260 29.084276 41.383766 46.999535 50.200222 59.220711

CVX 1125.0 120.667475 36.004832 44.864265 87.971695 134.733536 153.243607 176.953262

DD 1125.0 64.932338 11.107107 26.226181 56.228531 68.340065 73.100937 82.160004

DIS 1125.0 124.724984 33.161822 79.062325 97.129997 113.849998 149.622360 201.254089

F 1125.0 10.669939 3.193563 3.364042 9.495123 11.201049 12.310000 21.238628

GE 1125.0 67.139188 30.726982 26.821478 47.380741 61.730171 80.237434 168.860001

GILD 1125.0 64.485216 8.982150 48.918766 57.292091 62.327827 73.114235 85.358162

GM 1125.0 39.789857 10.409134 16.454935 32.726471 37.865936 47.570000 64.389725

GOOGL 1125.0 112.715794 28.157881 52.646080 89.788452 114.440659 135.842102 179.630005

GS 1125.0 303.479342 73.462022 121.462883 270.750275 317.004181 350.596802 467.580383

HD 1125.0 287.946219 46.524254 137.325714 258.115295 290.264862 315.013367 392.471649

HON 1125.0 184.879189 23.944280 95.141182 175.067902 190.931870 201.240326 220.703552

IBM 1125.0 122.849117 23.973442 73.761368 105.327614 119.168266 131.599976 195.835968

INTC 1125.0 42.294133 9.593616 23.974878 33.875050 44.011238 49.978661 62.477165

JCI 1125.0 54.227994 12.665147 21.432339 46.875332 56.875942 63.770000 76.871490

JNJ 1125.0 150.426623 12.724748 98.888367 145.279999 153.009399 158.975784 174.296173

JPM 1125.0 131.705269 28.884633 69.640205 111.258682 134.498169 147.201843 204.789993

KO 1125.0 53.109379 6.713766 32.919655 48.319462 55.395565 58.796181 63.656071

MCD 1125.0 234.139605 37.086671 124.335892 204.344177 237.010330 263.060455 296.902130

META 1125.0 271.613339 95.444213 88.727669 201.665588 268.388489 328.095795 526.816956

MMM 1125.0 104.554440 20.317660 68.398048 87.095383 104.484344 120.384705 146.007172

MRK 1125.0 86.375625 20.211091 55.622543 68.933578 78.446602 104.073280 131.165314

MSFT 1125.0 273.887771 70.907046 130.375595 224.182755 265.359100 321.913879 449.779999

PEP 1125.0 150.520650 21.307595 92.089531 129.536469 157.412201 167.235062 188.991516

PFE 1125.0 35.864667 7.338801 22.702326 29.745178 34.496193 42.067959 55.076660

PG 1125.0 135.360503 15.846908 87.905472 125.435829 135.991638 147.639648 168.559998

T 1125.0 16.692364 1.474788 12.776750 15.869843 16.803026 17.472309 21.093868

TSLA 1125.0 206.531430 81.738779 24.081333 166.660004 216.419998 258.079987 409.970001

UNH 1125.0 422.687371 91.189455 183.182266 333.794434 462.890991 496.851379 546.607117

V 1125.0 217.368442 27.959699 131.732117 198.659409 213.533295 230.491501 289.833618

VZ 1125.0 41.765110 5.625551 29.680738 36.542049 44.023743 46.539070 50.483551

WMT 1125.0 46.695827 6.333629 32.341011 43.098869 45.827610 49.881126 68.010002

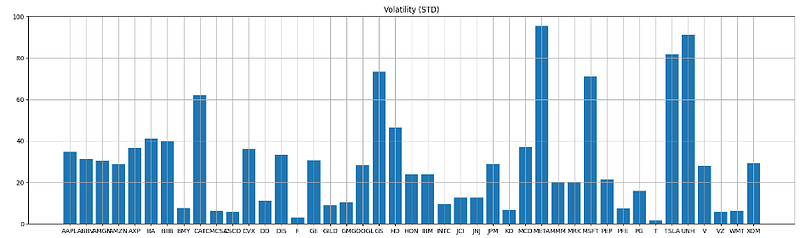

XOM 1125.0 73.847216 29.364404 25.440153 49.019825 76.831482 102.509506 121.215431- Plotting the volatility (STD) column

yy=close.describe().T

plt.figure(figsize=(22,6))

plt.bar(ticker_list,yy['std'])

plt.title('Volatility (STD)')

plt.grid()

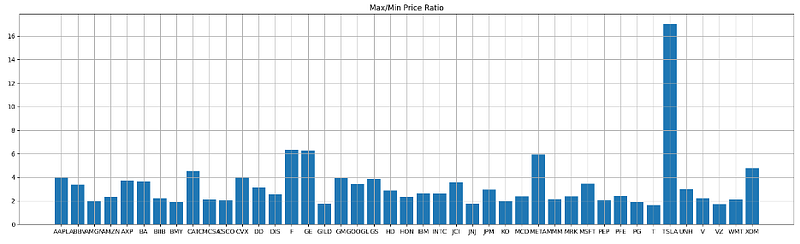

- Calculating and plotting the price range as the Max/Min ratio

yy=close.describe().T

plt.figure(figsize=(22,6))

plt.bar(ticker_list,yy['max']/yy['min'])

plt.title('Max/Min Price Ratio')

plt.grid()

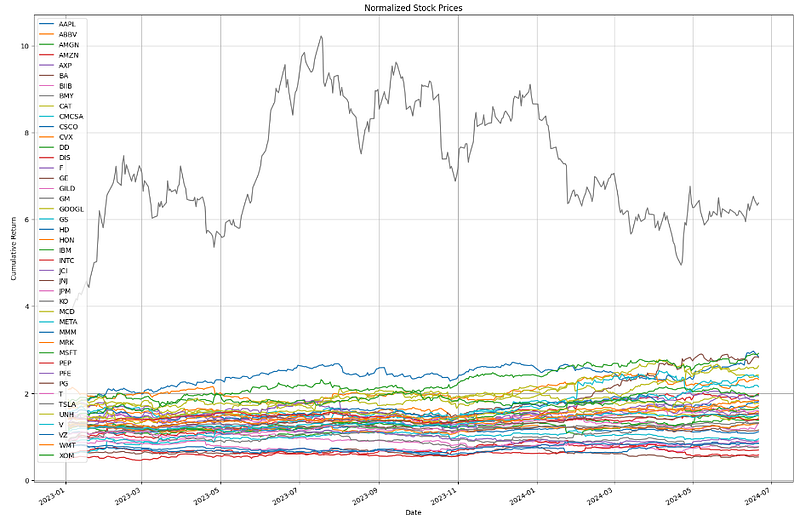

- Calculating the stock normalize price or cumulative return 2023–2024

def plot_data2(df,stocks,title='Stock Prices',ylabel="Stock Price",start='2023-01-03', end ='2024-06-21'):

""" This function creates a plot of adjusted close stock prices

inputs:

df - dataframe

title - plot title

stocks - the stock symbols of each company

ylabel - y axis label

y - horizontal line(integer)

output: the plot of adjusted close stock prices

"""

df_new = df[start:end]

ax = df_new.plot(title=title, figsize=(20,14), ax = None)

ax.set_xlabel("Date")

ax.set_ylabel(ylabel)

ax.legend(stocks, loc='upper left')

plt.grid()

plt.show()

# create function that normalizes the data

def normalize_data(df):

"""

This function normalizes the stock prices using the first row of the dataframe

input - stock data

output - normalized stock data

"""

return df/df.iloc[0,:]

stocks = ticker_list

plot_data2(normalize_data(close),stocks,title = "Normalized Stock Prices", ylabel = 'Cumulative Return')

- Calculating the stock daily returns

def generate_returns(prices, shift):

return_prices = prices.pct_change(shift).iloc[shift:, :]

return return_prices

returns = generate_returns(close, 1)

returns.tail()

AAPL ABBV AMGN AMZN AXP BA BIIB BMY CAT CMCSA ... PEP PFE PG T TSLA UNH V VZ WMT XOM

Date

2024-06-14 00:00:00-04:00 -0.008168 0.012188 0.000402 -0.000925 0.011837 -0.018982 -0.009194 -0.006750 -0.014983 -0.003725 ... 0.002939 -0.004340 0.002283 -0.001698 -0.024442 -0.000362 -0.001954 -0.002765 0.004798 -0.008451

2024-06-17 00:00:00-04:00 0.019671 0.006465 0.015605 0.002178 0.015346 0.006318 -0.022573 -0.005583 0.002893 -0.003472 ... 0.014224 -0.019978 0.004257 0.001701 0.052975 -0.011696 0.001884 -0.005294 0.005968 -0.006874

2024-06-18 00:00:00-04:00 -0.010984 0.009901 0.008936 -0.006791 0.004556 -0.019059 -0.012408 -0.003905 0.008499 -0.010989 ... 0.002046 0.015938 0.006328 0.021505 -0.013764 -0.016720 0.009035 0.015712 0.002670 0.009413

2024-06-20 00:00:00-04:00 -0.021513 0.004493 0.012746 0.017997 0.003925 0.007486 0.008630 0.005636 0.012272 0.025745 ... 0.001201 0.012039 -0.005280 0.003324 -0.017797 0.007213 0.011695 0.003992 0.006065 0.021576

2024-06-21 00:00:00-04:00 -0.010444 -0.010109 -0.005583 0.016013 0.000738 0.001475 -0.007004 0.021686 -0.003919 0.016645 ... 0.003600 0.000000 0.003519 0.016013 0.007931 -0.003983 -0.005780 0.000000 -0.001470 -0.008770

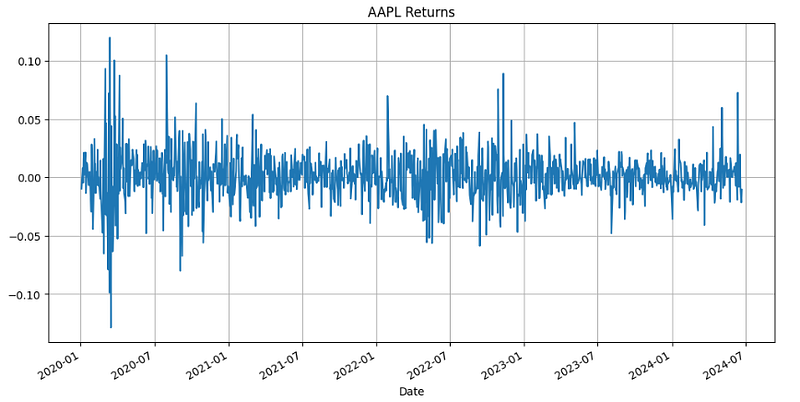

5 rows × 43 columns- Plotting the AAPL daily return as an example

returns['AAPL'].plot(figsize=(12,6))

plt.grid()

plt.title('AAPL Returns')

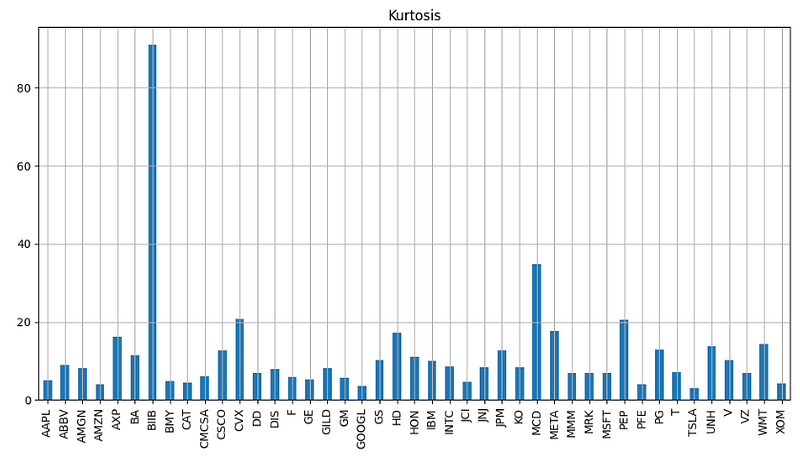

- Calculating and plotting the kurtosis of daily returns

plt.figure(figsize=(12, 6))

retkurt=returns.kurt()

retkurt.plot.bar()

plt.grid()

plt.title('Kurtosis')

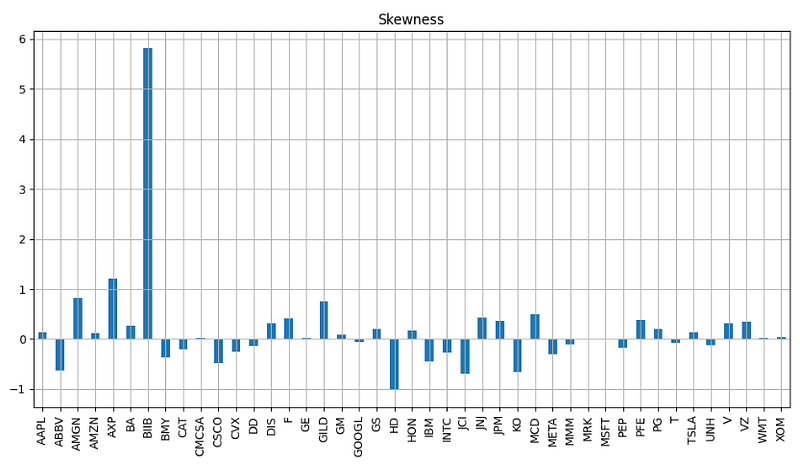

- Calculating and plotting the skewness of daily returns

plt.figure(figsize=(12, 6))

retkurt=returns.skew()

retkurt.plot.bar()

plt.grid()

plt.title('Skewness')

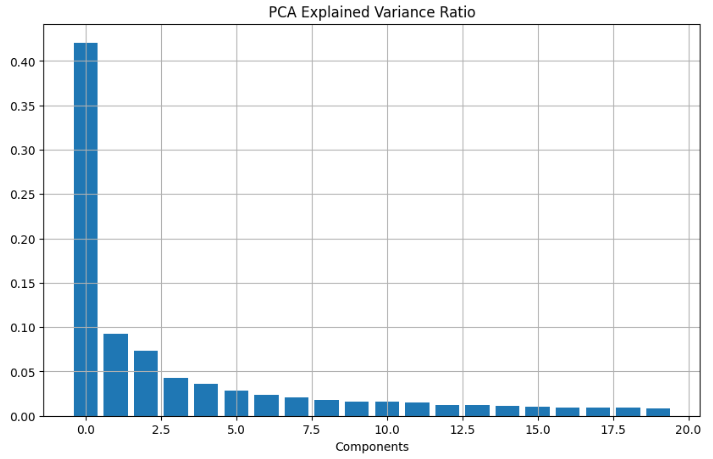

- Creating the Statistical Risk Model

- Performing SVD PCA of daily return in terms of 20 factor exposures

# Fit PCA

from sklearn.decomposition import PCA

def fit_pca(returns, num_factor_exposures, svd_solver):

pca = PCA(n_components=num_factor_exposures, svd_solver=svd_solver)

return pca.fit(returns)

num_factor_exposures = 20

pca = fit_pca(returns, num_factor_exposures, 'full')

2. Calculating the factor betas in terms of PCA vs factor exposures

#Factor Betas

def factor_betas(pca, factor_beta_indices, factor_beta_columns):

factor_betas = pd.DataFrame(pca.components_.T, factor_beta_indices, factor_beta_columns)

return factor_betas

risk_model = {}

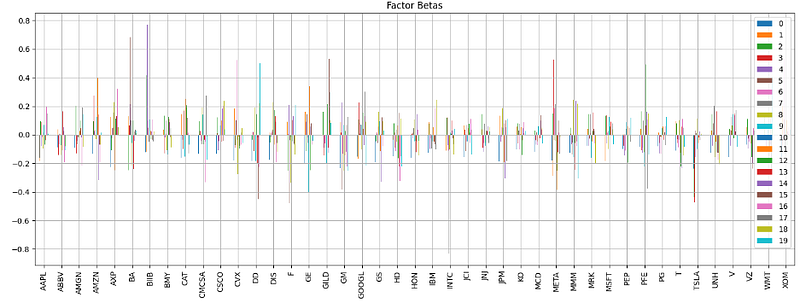

risk_model['factor_betas'] = factor_betas(pca, returns.columns.values, np.arange(num_factor_exposures))- Plotting the factor betas

risk_model['factor_betas'].plot.bar(figsize=(18,6))

plt.grid()

plt.title('Factor Betas')

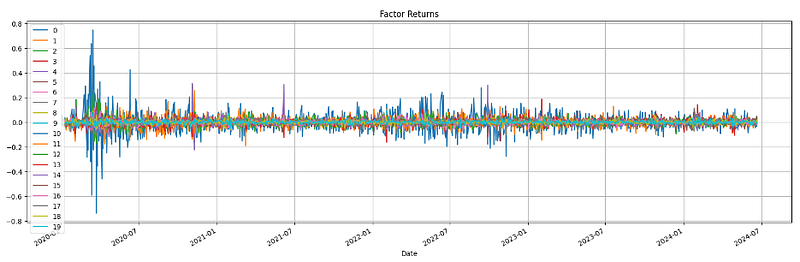

3. Calculating and plotting the factor returns

# Factor Returns

def factor_returns(pca, returns, factor_return_indices, factor_return_columns):

factor_returns = pd.DataFrame(pca.transform(returns), factor_return_indices, factor_return_columns)

return factor_returns

risk_model['factor_returns'] = factor_returns(

pca,

returns,

returns.index,

np.arange(num_factor_exposures))

risk_model['factor_returns'].plot(figsize=(20,6))

plt.grid()

plt.title('Factor Returns')

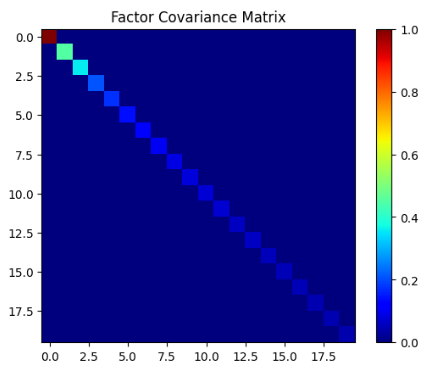

4. Calculating and plotting the factor covariance matrix

# Factor Covariance Matrix

def factor_cov_matrix(factor_returns, ann_factor):

factor_cov_matrix = np.var(factor_returns, ddof=1)

factor_cov_matrix = np.diag(factor_cov_matrix) * ann_factor

return factor_cov_matrix

ann_factor = 252 # Annualization factor

risk_model['factor_cov_matrix'] = factor_cov_matrix(risk_model['factor_returns'], ann_factor)

from matplotlib.pyplot import imshow

import numpy as np

data = risk_model['factor_cov_matrix']

imshow(np.asarray(data),vmin=0, vmax=1, cmap='jet')

plt.colorbar()

plt.title('Factor Covariance Matrix')

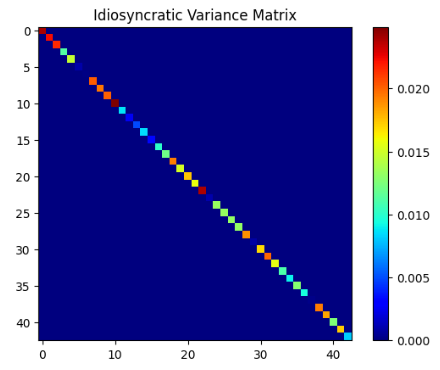

5. Calculating and plotting the Idiosyncratic Variance Matrix

# Idiosyncratic Variance Matrix

def idiosyncratic_var_matrix(returns, factor_returns, factor_betas, ann_factor):

dot_product = np.dot(factor_returns, factor_betas.T)

common_return = pd.DataFrame(dot_product, returns.index, returns.columns)

residual_return = returns - common_return

idiosyncratic_var_matrix = pd.DataFrame(np.diag(np.var(residual_return)) * ann_factor, returns.columns, returns.columns)

return idiosyncratic_var_matrix

risk_model['idiosyncratic_var_matrix'] = idiosyncratic_var_matrix(returns, risk_model['factor_returns'], risk_model['factor_betas'], ann_factor)

from matplotlib.pyplot import imshow

import numpy as np

data = risk_model['idiosyncratic_var_matrix']

imshow(np.asarray(data),cmap='jet')

plt.colorbar()

plt.title('Idiosyncratic Variance Matrix')

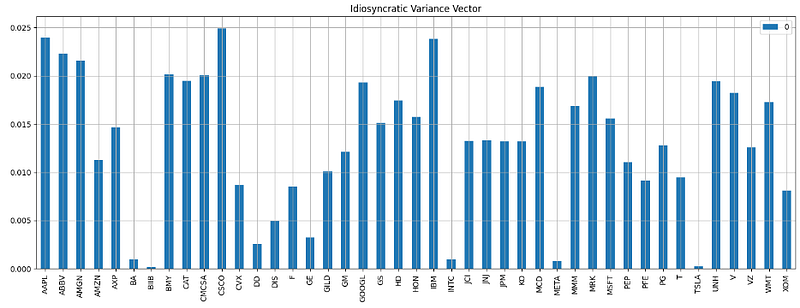

6. Calculating and plotting the Idiosyncratic Variance Vector

# Idiosyncratic Variance Vector

def idiosyncratic_var_vector(returns, idiosyncratic_var_matrix):

idiosyncratic_var_vector = pd.DataFrame(np.diagonal(idiosyncratic_var_matrix), returns.columns)

return idiosyncratic_var_vector

risk_model['idiosyncratic_var_vector'] = idiosyncratic_var_vector(returns, risk_model['idiosyncratic_var_matrix'])

from matplotlib.pyplot import imshow

import numpy as np

data = risk_model['idiosyncratic_var_vector']

risk_model['idiosyncratic_var_vector'].plot.bar(figsize=(18,6))

plt.grid()

plt.title('Idiosyncratic Variance Vector')

7. Predicting the expected portfolio risk using the above Risk Model

# Predict using the Risk Model

def predict_portfolio_risk(factor_betas, factor_cov_matrix, idiosyncratic_var_matrix, weights):

form_break_01 = np.dot(np.dot(factor_betas, factor_cov_matrix), factor_betas.T) + idiosyncratic_var_matrix # (BFB.T + S)

form_break_02 = np.dot(np.dot(weights.T, form_break_01), weights) # (X.T(form_break_01)X)

predicted_portfolio_risk = np.sqrt(form_break_02)

return predicted_portfolio_risk[0][0]

all_weights = pd.DataFrame(np.repeat(1/len(ticker_list), len(ticker_list)), ticker_list)

predict_portfolio_risk(

risk_model['factor_betas'],

risk_model['factor_cov_matrix'],

risk_model['idiosyncratic_var_matrix'],

all_weights)

0.2090265849547022- Creating the Alpha Factors

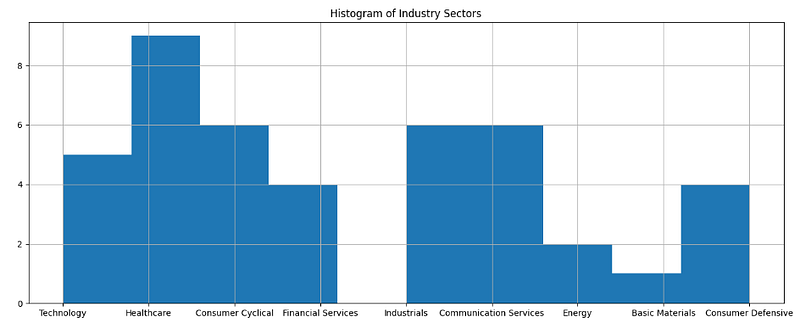

#Part 3: Create Alpha Factors

# Function to fetch sector information for a list of tickers

def fetch_sector_data(ticker_list):

sector = {}

for ticker in ticker_list:

tickerdata = yf.Ticker(ticker)

sector[ticker] = tickerdata.info.get('sector', 'Unknown')

return sector

sectors_data = fetch_sector_data(ticker_list)

sectors_series = pd.Series(sectors_data)

print(sectors_series)

AAPL Technology

ABBV Healthcare

AMGN Healthcare

AMZN Consumer Cyclical

AXP Financial Services

BA Industrials

BIIB Healthcare

BMY Healthcare

CAT Industrials

CMCSA Communication Services

CSCO Technology

CVX Energy

DD Basic Materials

DIS Communication Services

F Consumer Cyclical

GE Industrials

GILD Healthcare

GM Consumer Cyclical

GOOGL Communication Services

GS Financial Services

HD Consumer Cyclical

HON Industrials

IBM Technology

INTC Technology

JCI Industrials

JNJ Healthcare

JPM Financial Services

KO Consumer Defensive

MCD Consumer Cyclical

META Communication Services

MMM Industrials

MRK Healthcare

MSFT Technology

PEP Consumer Defensive

PFE Healthcare

PG Consumer Defensive

T Communication Services

TSLA Consumer Cyclical

UNH Healthcare

V Financial Services

VZ Communication Services

WMT Consumer Defensive

XOM Energy

dtype: object- Plotting the Histogram of Industry Sectors involved

plt.figure(figsize=(16,6))

sectors_series.hist()

plt.title('Histogram of Industry Sectors')

- Implementing the Mean_Reversion_5Day_Sector_Neutral factor

# Mean Reversion 5 Day Sector Neutral Factor

# Auxiliary function to calculate z-scores

def calculate_z_scores(demeaned):

# Adding a small value to the standard deviation to avoid division by zero

epsilon = 1e-7

demeaned_std_aligned = demeaned.std(axis=1).to_frame(name='std')

demeaned_std_aligned = pd.concat([demeaned_std_aligned] * demeaned.shape[1], axis=1)

demeaned_std_aligned.columns = demeaned.columns

demeaned_std_aligned += epsilon

# Calculating z-scores

demeaned_mean_aligned = demeaned.mean(axis=1).to_frame(name='mean')

demeaned_mean_aligned = pd.concat([demeaned_mean_aligned] * demeaned.shape[1], axis=1)

demeaned_mean_aligned.columns = demeaned.columns

z_scored = (demeaned - demeaned_mean_aligned) / demeaned_std_aligned

return z_scored

# Function for 5-day sector neutral mean reversion

def calculate_mean_reversion_5day_sector_neutral(returns, sectors):

# Aligning sectors with the return columns

aligned_sectors = sectors_series.reindex(returns.columns)

# Subtracting the sector mean from each return

sector_means = returns.groupby(aligned_sectors, axis=1).transform('mean')

demeaned = - returns.sub(sector_means)

# Normalizing the results

demeaned = demeaned.rank(axis=1)

z_scored = calculate_z_scores(demeaned)

# Converting to long format

z_scored_long = z_scored.stack().reset_index()

z_scored_long.columns = ['Date', 'Ticker', 'Mean_Reversion_5Day_Sector_Neutral']

return z_scored_long

# Calculating 5-day returns

returns_5d = generate_returns(close, 5)

# Applying the function

mean_reversion_5day_sector_neutral = calculate_mean_reversion_5day_sector_neutral(returns_5d, sectors_series)

mean_reversion_5day_sector_neutral.set_index(['Date', 'Ticker'])

Mean_Reversion_5Day_Sector_Neutral

Date Ticker

2020-01-09 00:00:00-05:00 AAPL -1.433516

ABBV -0.318559

AMGN 0.557478

AMZN 0.955677

AXP -0.238919

... ... ...

2024-06-21 00:00:00-04:00 UNH 1.513156

V 0.398199

VZ 0.637118

WMT -0.079640

XOM 0.477839

48160 rows × 1 columns- Implementing the Mean_Reversion_5Day_Sector_Neutral_Smoothed factor

# Mean Reversion 5 Day Sector Neutral Smoothed Factor

# Function for smoothed 5-day sector neutral mean reversion

def calculate_mean_reversion_5day_sector_neutral_smoothed(factor_long):

# Reconverting to wide format for smoothing

factor_wide = factor_long.pivot(index='Date', columns='Ticker', values='Mean_Reversion_5Day_Sector_Neutral')

# Smoothing using simple moving average

smoothed = factor_wide.rolling(window=5).mean()

# Normalizing the results again

smoothed = smoothed.rank(axis=1)

z_scored = calculate_z_scores(smoothed)

# Converting to long format

z_scored_long = z_scored.stack().reset_index()

z_scored_long.columns = ['Date', 'Ticker', 'Mean_Reversion_5Day_Sector_Neutral_Smoothed']

return z_scored_long

mean_reversion_5day_sector_neutral_smoothed = calculate_mean_reversion_5day_sector_neutral_smoothed(mean_reversion_5day_sector_neutral.reset_index())

mean_reversion_5day_sector_neutral_smoothed.set_index(['Date', 'Ticker'])

Mean_Reversion_5Day_Sector_Neutral_Smoothed

Date Ticker

2020-01-15 00:00:00-05:00 AAPL -1.433733

ABBV 0.318607

AMGN 0.438085

AMZN 1.593036

AXP -0.557563

... ... ...

2024-06-21 00:00:00-04:00 UNH 0.796398

V 0.398199

VZ 0.557478

WMT -1.114957

XOM 0.637118

47988 rows × 1 columns- Implementing the Sum_Overnight_Sentiment_5Day factor

# Overnight Sentiment Factor

# Function to calculate overnight returns

def calculate_overnight_returns(open_prices, close_prices):

# Calculating the return from yesterday's close to today's open

return (open_prices - close_prices.shift(1)) / close_prices.shift(1)

# Function to calculate trailing overnight returns

def calculate_overnight_sentiment(overnight_returns, window_length):

# Calculating the rolling sum of overnight returns

summed = overnight_returns.rolling(window=window_length).sum()

# Normalizing the results by converting to z-score

z_scored = calculate_z_scores(summed)

# Converting back to long format

z_scored_long = z_scored.stack().reset_index()

z_scored_long.columns = ['Date', 'Ticker', 'Sum_Overnight_Sentiment_5Day']

return z_scored_long

# Applying the functions

overnight_returns = calculate_overnight_returns(open, close)

overnight_sentiment = calculate_overnight_sentiment(overnight_returns, window_length=5)

overnight_sentiment.set_index(['Date', 'Ticker'])

Sum_Overnight_Sentiment_5Day

Date Ticker

2020-01-09 00:00:00-05:00 AAPL -0.061856

ABBV -0.349628

AMGN -0.232041

AMZN -0.506176

AXP -0.097025

... ... ...

2024-06-21 00:00:00-04:00 UNH -0.239129

V -0.392243

VZ -0.114173

WMT 0.208194

XOM 1.099303

48160 rows × 1 columns- Implementing the Sum_Overnight_Sentiment_5Day_Smoothed factor

# Overnight Sentiment Smoothed Factor

def calculate_overnight_sentiment_smoothed(overnight_sentiment):

# Reconverting to wide format for smoothing

overnight_wide = overnight_sentiment.pivot(index='Date', columns='Ticker', values='Sum_Overnight_Sentiment_5Day')

# Smoothing using simple moving average

smoothed = overnight_wide.rolling(window=5).mean()

# Normalizing the results again

smoothed = smoothed.rank(axis=1)

z_scored = calculate_z_scores(smoothed)

# Converting to long format

z_scored_long = z_scored.stack().reset_index()

z_scored_long.columns = ['Date', 'Ticker', 'Sum_Overnight_Sentiment_5Day_Smoothed']

return z_scored_long

overnight_sentiment_smoothed = calculate_overnight_sentiment_smoothed(overnight_sentiment.reset_index())

overnight_sentiment_smoothed.set_index(['Date', 'Ticker'])

Sum_Overnight_Sentiment_5Day_Smoothed

Date Ticker

2020-01-15 00:00:00-05:00 AAPL 1.035317

ABBV 0.079640

AMGN -0.716758

AMZN 0.398199

AXP 0.477839

... ... ...

2024-06-21 00:00:00-04:00 UNH -0.557478

V 0.000000

VZ 0.637118

WMT 1.114957

XOM 1.433516

47988 rows × 1 columns- Combining all the above Factors into a single DF

# Combine the Factors

from functools import reduce

# Create a list of all dataframes

dataframes = [mean_reversion_5day_sector_neutral,

mean_reversion_5day_sector_neutral_smoothed,

overnight_sentiment,

overnight_sentiment_smoothed]

# Use 'reduce' to merge all dataframes into a single dataframe

all_factors = reduce(lambda left, right: pd.merge(left, right, on=['Date', 'Ticker'], how='inner'), dataframes)

# Readjust 'Date' and 'Ticker' as indices

all_factors = all_factors.set_index(['Date', 'Ticker'])

all_factors['Combined_Factors'] = all_factors.mean(axis=1)

all_factors

Mean_Reversion_5Day_Sector_Neutral Mean_Reversion_5Day_Sector_Neutral_Smoothed Sum_Overnight_Sentiment_5Day Sum_Overnight_Sentiment_5Day_Smoothed Combined_Factors

Date Ticker

2020-01-15 00:00:00-05:00 AAPL -0.955677 -1.433733 0.690153 1.035317 -0.165985

ABBV 0.637118 0.318607 -0.073723 0.079640 0.240410

AMGN 0.000000 0.438085 -0.430507 -0.716758 -0.177295

AMZN 1.513156 1.593036 0.488492 0.398199 0.998221

AXP -0.716758 -0.557563 0.107696 0.477839 -0.172197

... ... ... ... ... ... ...

2024-06-21 00:00:00-04:00 UNH 1.513156 0.796398 -0.239129 -0.557478 0.378237

V 0.398199 0.398199 -0.392243 0.000000 0.101039

VZ 0.637118 0.557478 -0.114173 0.637118 0.429386

WMT -0.079640 -1.114957 0.208194 1.114957 0.032139

XOM 0.477839 0.637118 1.099303 1.433516 0.911944

47988 rows × 5 columns- Evaluating the Alpha Factors

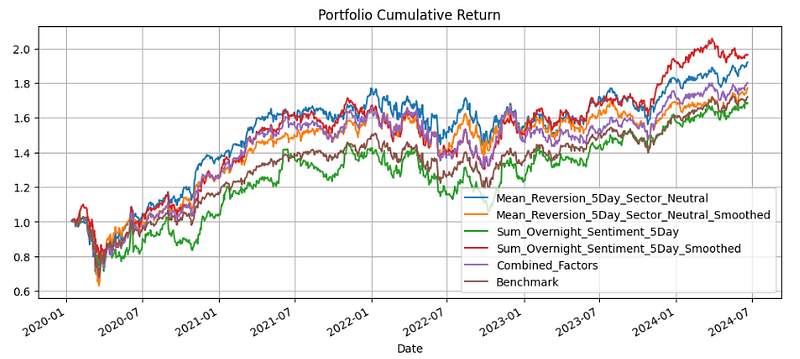

#A. Factor Returns

# Calculate forward returns and align with factor data dates

forward_returns = generate_returns(close, 1).shift(-1).reset_index()

forward_returns = forward_returns.loc[forward_returns['Date'].isin(set(all_factors.reset_index().Date))].set_index('Date')

forward_returns = forward_returns.stack().reset_index()

forward_returns.columns = ['Date', 'Ticker', 'Returns']

forward_returns.set_index(['Date', 'Ticker'], inplace=True)

def calculate_allocation(df):

df[df < 0] = 0

return df.groupby(level=0, group_keys=False).apply(lambda x: x / x.sum())

# Calculate allocations and combine with forward returns

allocation = all_factors.copy()

allocation = calculate_allocation(allocation)

strategy_returns = allocation.reset_index().merge(forward_returns.reset_index(), on=['Date', 'Ticker']).set_index(['Date', 'Ticker'])

# Apply allocation weights to returns

strategy_returns.update(strategy_returns.drop(columns='Returns').mul(strategy_returns['Returns'], axis=0))

# Calculate strategy and benchmark returns

mean_returns = strategy_returns[['Returns']].groupby(level=0, group_keys=False).apply(lambda x: x.mean())

strategy_returns = strategy_returns.drop(columns='Returns').groupby(level=0, group_keys=False).apply(lambda x: x.sum())

strategy_returns['Benchmark'] = mean_returns

# Plot cumulative returns

(1 + strategy_returns).cumprod().plot(figsize=(12, 5))

plt.title('Portfolio Cumulative Return')

plt.grid()

plt.show()

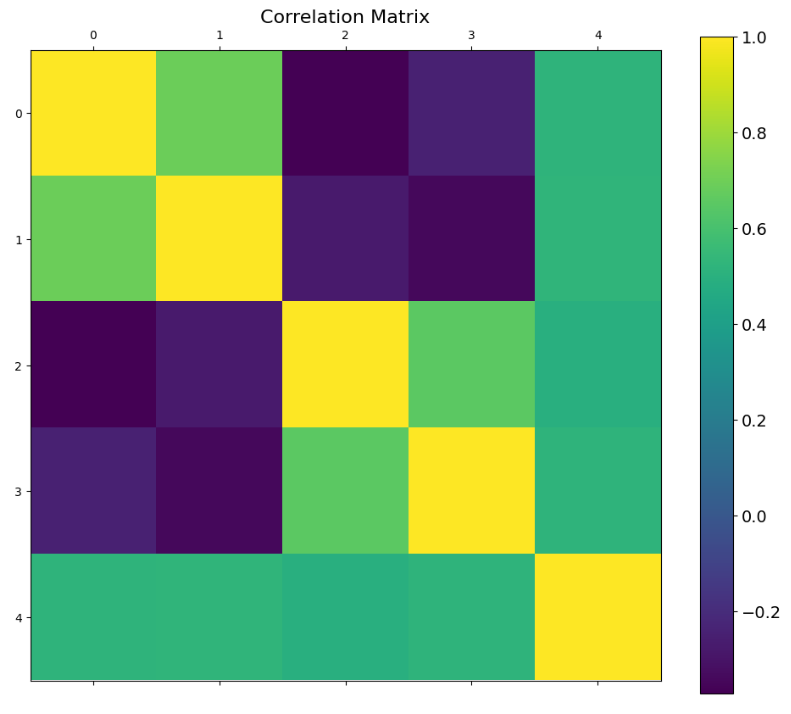

- Correlation Analysis: calculate the correlation matrix for alpha factors

#B. Correlation Analysis

# Calculate the correlation matrix for alpha factors

correlation_matrix = all_factors.corr()

correlation_matrix.style.background_gradient(cmap='RdBu')

Mean_Reversion_5Day_Sector_Neutral Mean_Reversion_5Day_Sector_Neutral_Smoothed Sum_Overnight_Sentiment_5Day Sum_Overnight_Sentiment_5Day_Smoothed Combined_Factors

Mean_Reversion_5Day_Sector_Neutral 1.000000 0.691424 -0.371131 -0.242775 0.523061

Mean_Reversion_5Day_Sector_Neutral_Smoothed 0.691424 1.000000 -0.270885 -0.339575 0.524734

Sum_Overnight_Sentiment_5Day -0.371131 -0.270885 1.000000 0.654801 0.491634

Sum_Overnight_Sentiment_5Day_Smoothed -0.242775 -0.339575 0.654801 1.000000 0.520599

Combined_Factors 0.523061 0.524734 0.491634 0.520599 1.000000

f = plt.figure(figsize=(12, 10))

plt.matshow(correlation_matrix, fignum=f.number)

cb = plt.colorbar()

cb.ax.tick_params(labelsize=14)

plt.title('Correlation Matrix', fontsize=16);

- Explaining the correlation matrix columns 0–4

correlation_matrix.columns

Index(['Mean_Reversion_5Day_Sector_Neutral',

'Mean_Reversion_5Day_Sector_Neutral_Smoothed',

'Sum_Overnight_Sentiment_5Day', 'Sum_Overnight_Sentiment_5Day_Smoothed',

'Combined_Factors'],

dtype='object')- Drawdown Analysis

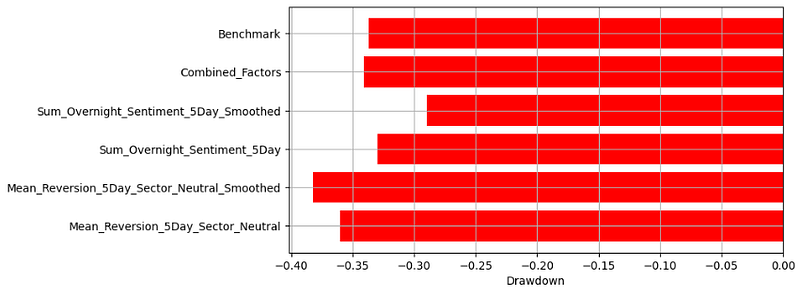

#C. Drawdown Analysis

# Calculate cumulative returns

cumulative_returns = (1 + strategy_returns).cumprod()

# Drawdown Analysis

peak = cumulative_returns.expanding(min_periods=1).max()

drawdown = (cumulative_returns - peak) / peak

plt.figure(figsize=(8, 4))

plt.barh(drawdown.min().index, drawdown.min(), color='red')

plt.xlabel('Drawdown')

plt.grid()

plt.show()

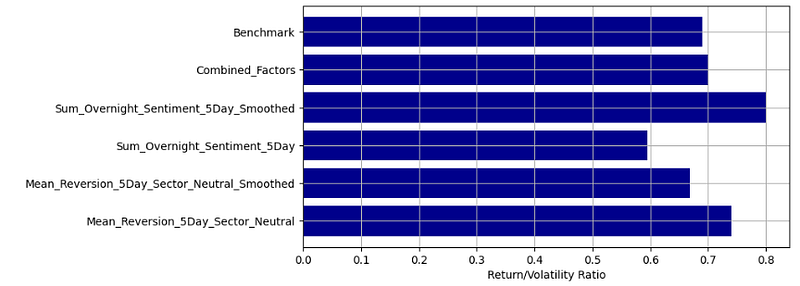

- Calculating the Return/Volatility Ratio

#D. Return to Volatility Ratio

# Calculate annualized return

annualized_return = strategy_returns.mean() * 252

# Calculate annualized volatility

annualized_volatility = strategy_returns.std() * np.sqrt(252)

# Return to volatility ratio

return_to_volatility_ratio = annualized_return / annualized_volatility

plt.figure(figsize=(8, 4))

plt.barh(return_to_volatility_ratio.index, return_to_volatility_ratio, color='darkblue')

plt.xlabel('Return/Volatility Ratio')

plt.grid()

plt.show()

Smart Beta PO (Portfolio 2)

- Let’s explore the application of the Smart Beta strategy in PO, viz. Part 1: Fetching Stock Data; Part 2: Creating Weights for Benchmarks; Part 3: Portfolio Optimization (Smart Beta Strategy).

- Let’s look at the 5Y Portfolio 2 of 10 stocks

# Fetch the data

ticker_list = ['PG', 'JNJ', 'KO', 'MCD', 'MMM', 'IBM', 'PEP', 'T', 'VZ', 'WMT']

years = 5- Importing libraries and fetching the relevant stock data, v.i.

# Import necessary libraries

import yfinance as yf

import pandas as pd

from datetime import datetime, timedelta

import numpy as np

import json

import matplotlib.pyplot as plt

#Part 1: Fetching Stock Data

def fetch_stock_data(ticker_list, years=5):

end_date = datetime.now()

start_date = end_date - timedelta(days=years * 365)

close_data_df = pd.DataFrame()

volume_data_df = pd.DataFrame()

dividends_data_df = pd.DataFrame()

for ticker in ticker_list:

stock = yf.Ticker(ticker)

hist_data = stock.history(period='1d', start=start_date, end=end_date)

# Close Data

close_data = hist_data['Close'].rename(ticker)

close_data_df = pd.merge(close_data_df, pd.DataFrame(close_data), left_index=True, right_index=True, how='outer')

# Volume Data

volume_data = hist_data['Volume'].rename(ticker)

volume_data_df = pd.merge(volume_data_df, pd.DataFrame(volume_data), left_index=True, right_index=True, how='outer')

# Dividends Data

dividends_data = hist_data['Dividends'].rename(ticker)

dividends_data_df = pd.merge(dividends_data_df, pd.DataFrame(dividends_data), left_index=True, right_index=True, how='outer')

return close_data_df, volume_data_df, dividends_data_df

close, volume, dividends = fetch_stock_data(ticker_list, years)

close.tail()

PG JNJ KO MCD MMM IBM PEP T VZ WMT

Date

2024-06-14 00:00:00-04:00 166.789993 145.539993 62.549999 253.580002 100.900002 169.210007 163.809998 17.639999 39.669998 67.019997

2024-06-17 00:00:00-04:00 167.500000 145.949997 62.619999 253.509995 100.529999 169.500000 166.139999 17.670000 39.459999 67.419998

2024-06-18 00:00:00-04:00 168.559998 145.649994 62.630001 250.789993 100.769997 170.550003 166.479996 18.049999 40.080002 67.599998

2024-06-20 00:00:00-04:00 167.669998 147.779999 62.180000 253.800003 101.660004 173.919998 166.679993 18.110001 40.240002 68.010002

2024-06-21 00:00:00-04:00 168.259995 148.750000 62.770000 259.390015 102.389999 172.460007 167.279999 18.400000 40.240002 67.910004

close.shape

(1257, 10)

close.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 1257 entries, 2019-06-25 00:00:00-04:00 to 2024-06-21 00:00:00-04:00

Data columns (total 10 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 PG 1257 non-null float64

1 JNJ 1257 non-null float64

2 KO 1257 non-null float64

3 MCD 1257 non-null float64

4 MMM 1257 non-null float64

5 IBM 1257 non-null float64

6 PEP 1257 non-null float64

7 T 1257 non-null float64

8 VZ 1257 non-null float64

9 WMT 1257 non-null float64

dtypes: float64(10)

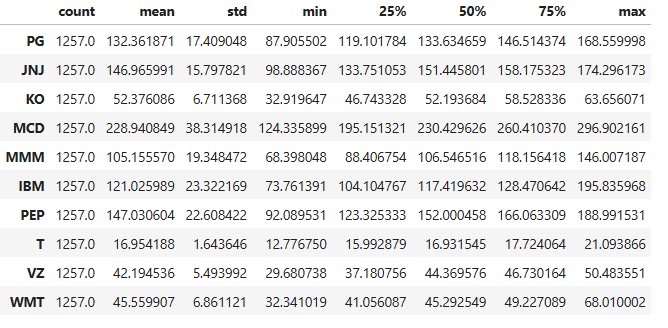

memory usage: 108.0 KB- Checking the descriptive statistics summary

close.describe().T

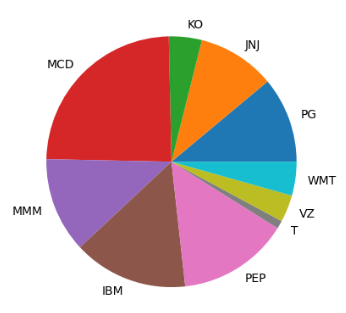

- Comparing the stock volatility (STD)

close1=close.describe().T

mylabels = ticker_list

y=close1['std']

plt.pie(y, labels = mylabels)

plt.show()

- Calculating and plotting the Market Volume Weights

#Part 2: Creating Weights for Benchmarks

#A. Market Volume Weights

def generateMarketVolumeWeights(close, volume):

dollar_volume = close * volume

market_volume_weights = dollar_volume.div(dollar_volume.sum(axis=1), axis=0)

# Shift the DataFrame by one row

# As the return for the month depends on the allocation defined in the previous month

shifted_market_volume_weights = market_volume_weights.shift(1)

return shifted_market_volume_weights

marketVolumeWeights = generateMarketVolumeWeights(close, volume)

marketVolumeWeights.tail()

PG JNJ KO MCD MMM IBM PEP T VZ WMT

Date

2024-06-14 00:00:00-04:00 0.116738 0.142376 0.086483 0.114468 0.073156 0.085326 0.126974 0.077607 0.070003 0.106869

2024-06-17 00:00:00-04:00 0.113643 0.109370 0.094340 0.131236 0.049957 0.086670 0.108842 0.073683 0.076666 0.155593

2024-06-18 00:00:00-04:00 0.153279 0.131725 0.089292 0.086931 0.047499 0.074344 0.121733 0.065670 0.119059 0.110469

2024-06-20 00:00:00-04:00 0.126916 0.132060 0.098247 0.109189 0.051144 0.085057 0.086290 0.089613 0.101087 0.120398

2024-06-21 00:00:00-04:00 0.161550 0.146852 0.093968 0.116639 0.040140 0.093293 0.093561 0.066024 0.080913 0.107061

marketVolumeWeights.plot(figsize=(12,6))

plt.grid()

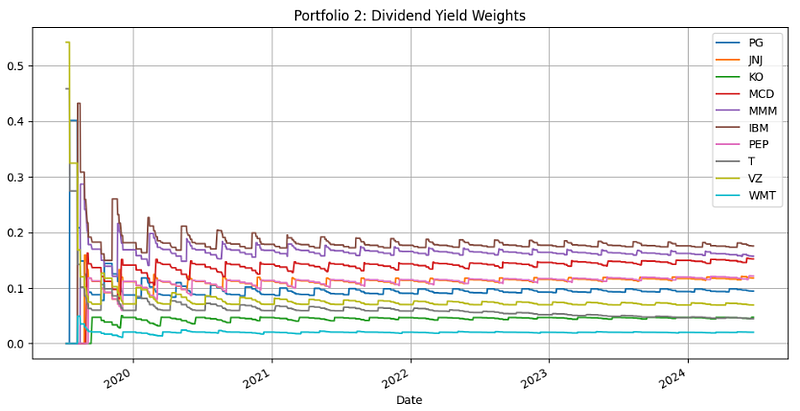

- Calculating and plotting the Dividend Yield Weights

#B. Dividend Yield Weights

def calculateDividendYieldWeights(dividends):

dividend_cumsum = dividends.cumsum()

dividend_yield_weights = dividend_cumsum.div(dividend_cumsum.sum(axis=1), axis=0)

# Shift the DataFrame by one row

# As the return for the month depends on the allocation defined in the previous month

shifted_dividend_yield_weights = dividend_yield_weights.shift(1)

return shifted_dividend_yield_weights

dividendYieldWeights = calculateDividendYieldWeights(dividends)

dividendYieldWeights.plot(figsize=(12,6))

plt.grid()

plt.title('Portfolio 2: Dividend Yield Weights')

- Generating and plotting the daily returns of Portfolio 2

#C. Returns

def generate_returns(prices):

return_prices = (prices / prices.shift(1)) - 1

return return_prices

returns = generate_returns(close)

returns.tail()

PG JNJ KO MCD MMM IBM PEP T VZ WMT

Date

2024-06-14 00:00:00-04:00 0.002283 0.000619 0.000720 -0.000473 -0.006303 0.000532 0.002939 -0.001698 -0.002765 0.004798

2024-06-17 00:00:00-04:00 0.004257 0.002817 0.001119 -0.000276 -0.003667 0.001714 0.014224 0.001701 -0.005294 0.005968

2024-06-18 00:00:00-04:00 0.006328 -0.002056 0.000160 -0.010729 0.002387 0.006195 0.002046 0.021505 0.015712 0.002670

2024-06-20 00:00:00-04:00 -0.005280 0.014624 -0.007185 0.012002 0.008832 0.019760 0.001201 0.003324 0.003992 0.006065

2024-06-21 00:00:00-04:00 0.003519 0.006564 0.009489 0.022025 0.007181 -0.008395 0.003600 0.016013 0.000000 -0.001470

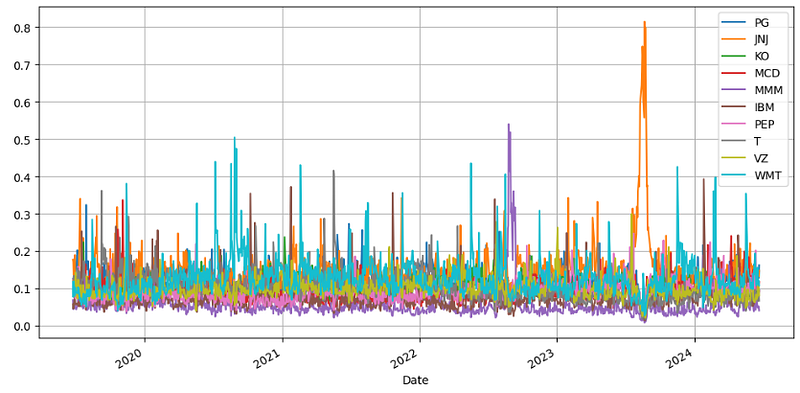

returns.plot(figsize=(12,6))

plt.grid()

plt.title('Daily Returns')

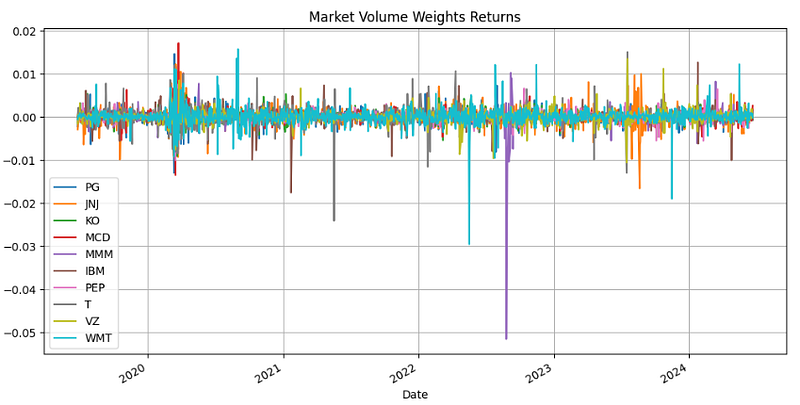

- Generating and plotting the Market Volume Weights Returns

#D. Weighted Returns

def generate_weighted_returns(returns, weights):

return returns * weights

marketVolumeWeightsReturn = generate_weighted_returns(returns, marketVolumeWeights)

dividendYieldWeightsReturns = generate_weighted_returns(returns, dividendYieldWeights)

marketVolumeWeightsReturn.plot(figsize=(12,6))

plt.grid()

plt.title('Market Volume Weights Returns')

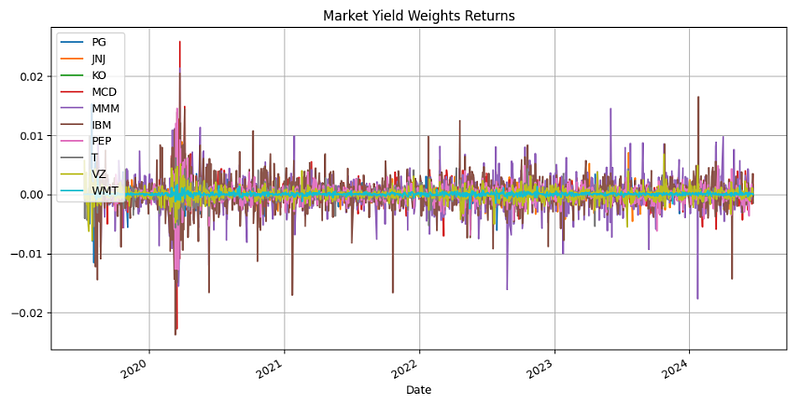

- Plotting the Market Yield Weights Returns

dividendYieldWeightsReturns.plot(figsize=(12,6))

plt.grid()

plt.title('Market Yield Weights Returns')

plt.legend(loc="upper left")

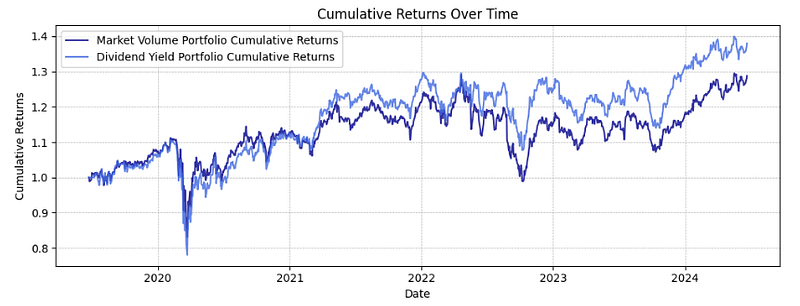

- Calculating and plotting the Cumulative Returns

#E. Cumulative Returns

def calculate_cumulative_returns(returns):

return (1 + returns.sum(axis = 1)).cumprod()

marketVolumeWeightsCumulativeReturn = calculate_cumulative_returns(marketVolumeWeightsReturn)

dividendYieldWeightsCumulativeReturn = calculate_cumulative_returns(dividendYieldWeightsReturns)

plt.figure(figsize=(10, 4))

plt.plot(marketVolumeWeightsCumulativeReturn, label='Market Volume Portfolio Cumulative Returns', alpha=0.8, color='darkblue')

plt.plot(dividendYieldWeightsCumulativeReturn, label='Dividend Yield Portfolio Cumulative Returns', alpha=0.8, color='royalblue')

plt.title('Cumulative Returns Over Time')

plt.xlabel('Date')

plt.ylabel('Cumulative Returns')

plt.legend(loc='upper left')

plt.grid(True, which='both', linestyle='--', linewidth=0.5)

plt.tight_layout()

plt.show()

- Implementing Part 3: Portfolio Optimization (Smart Beta Strategy)

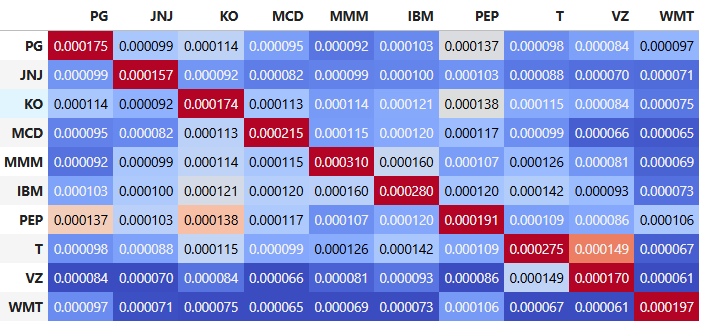

#A. Covariance matrix

def get_covariance_returns(returns):

return np.cov(returns.T.fillna(0))

covariance_returns = get_covariance_returns(returns)

covariance_returns = pd.DataFrame(covariance_returns, returns.columns, returns.columns)

covariance_returns

PG JNJ KO MCD MMM IBM PEP T VZ WMT

PG 0.000175 0.000099 0.000114 0.000095 0.000092 0.000103 0.000137 0.000098 0.000084 0.000097

JNJ 0.000099 0.000157 0.000092 0.000082 0.000099 0.000100 0.000103 0.000088 0.000070 0.000071

KO 0.000114 0.000092 0.000174 0.000113 0.000114 0.000121 0.000138 0.000115 0.000084 0.000075

MCD 0.000095 0.000082 0.000113 0.000215 0.000115 0.000120 0.000117 0.000099 0.000066 0.000065

MMM 0.000092 0.000099 0.000114 0.000115 0.000310 0.000160 0.000107 0.000126 0.000081 0.000069

IBM 0.000103 0.000100 0.000121 0.000120 0.000160 0.000280 0.000120 0.000142 0.000093 0.000073

PEP 0.000137 0.000103 0.000138 0.000117 0.000107 0.000120 0.000191 0.000109 0.000086 0.000106

T 0.000098 0.000088 0.000115 0.000099 0.000126 0.000142 0.000109 0.000275 0.000149 0.000067

VZ 0.000084 0.000070 0.000084 0.000066 0.000081 0.000093 0.000086 0.000149 0.000170 0.000061

WMT 0.000097 0.000071 0.000075 0.000065 0.000069 0.000073 0.000106 0.000067 0.000061 0.000197

covariance_returns.style.background_gradient(cmap='coolwarm')

- Importing cvxpy and invoking the weight optimization function

!pip install cvxpy

#B. Weight Optimization

import cvxpy as cvx

def get_optimal_weights(covariance_returns, index_weights, scale=2.0):

# Create a variable to store the portfolio weights.

x = cvx.Variable(len(index_weights))

# Calculate the portfolio variance using the quadratic form.

portfolio_var = cvx.quad_form(x, covariance_returns)

# Calculate the distance (L2 norm) between the portfolio weights and the index weights.

dist_index = cvx.norm(x - index_weights, p=2)

# Define the objective function: Minimize portfolio variance and distance from the index.

objective = cvx.Minimize(portfolio_var + scale * dist_index)

# Define the constraints: Weights should be positive and sum up to 1.

constraints = [x >= 0, sum(x) == 1]

# Set up the optimization problem.

problem = cvx.Problem(objective, constraints)

# Solve the optimization problem.

problem.solve()

# Return the optimal portfolio weights.

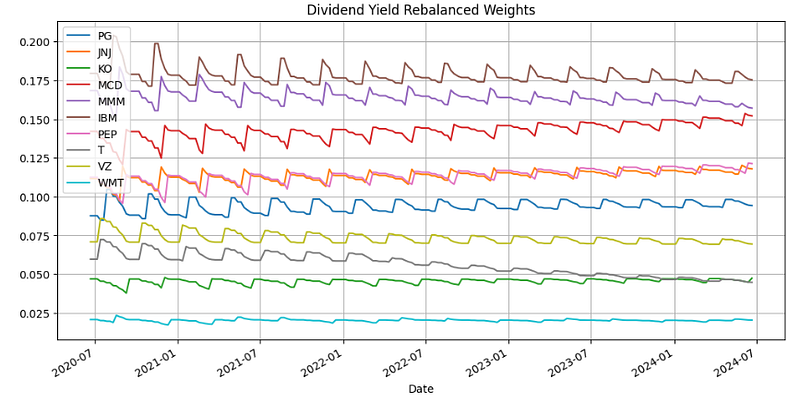

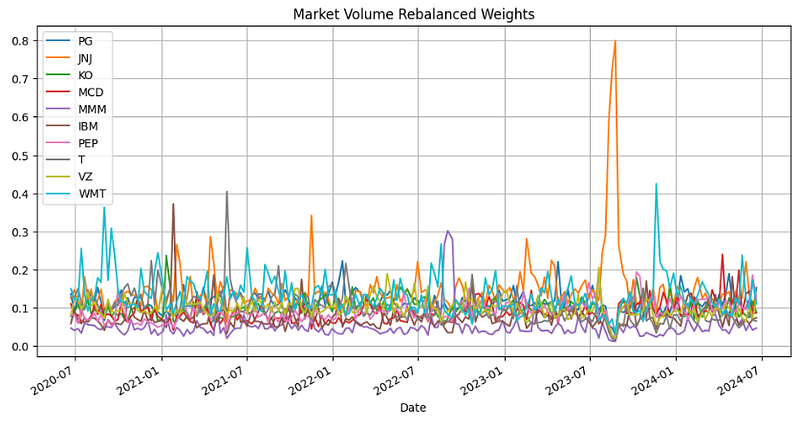

return x.value- Rebalancing portfolio over time with chunk_size = 250 (the size of the window over which covariance is calculated) and shift_size = 5 (the number of periods after which the portfolio will be rebalanced)

#C. Rebalance Portfolio Over Time

def rebalance_portfolio(returns, index_weights, shift_size, chunk_size):

# Initialize an empty list to store the rebalanced portfolio weights at each interval.

all_rebalance_weights = []

# List to store the rebalancing dates.

rebalance_dates = []

# Iterate through the historical data in steps of shift_size starting from chunk_size.

for i in range(chunk_size, len(returns), shift_size):

# Calculate the covariance matrix of returns over the chunk_size window up to the current period.

covariance_returns = get_covariance_returns(returns.iloc[i-chunk_size:i])

# Get the optimal portfolio weights using the covariance matrix and the latest index weights.

rebalance_weights = get_optimal_weights(covariance_returns, index_weights.iloc[i-1])

# Append the calculated optimal weights to our list.

all_rebalance_weights.append(rebalance_weights)

# Append the rebalance date to our dates list.

rebalance_dates.append(returns.index[i])

# Convert the list of optimal weights to a DataFrame with columns named after the assets.

df_rebalance_weights = pd.DataFrame(all_rebalance_weights, columns=returns.columns)

# Set the rebalance dates as the index of the resulting DataFrame.

df_rebalance_weights['Date'] = rebalance_dates

df_rebalance_weights.set_index('Date', inplace=True)

# Return the DataFrame.

return df_rebalance_weights

# Define the size of the window over which covariance is calculated.

chunk_size = 250

# Define the number of periods after which the portfolio will be rebalanced.

shift_size = 5

# Rebalance the portfolio

marketVolumeRebalanceWeights = rebalance_portfolio(returns, marketVolumeWeights, shift_size, chunk_size)

# Rebalance the portfolio

dividendYieldRebalanceWeights = rebalance_portfolio(returns, dividendYieldWeights, shift_size, chunk_size)- Plotting the Dividend Yield Rebalance Weights

dividendYieldRebalanceWeights.plot(figsize=(12,6))

plt.grid()

plt.title('Dividend Yield Rebalanced Weights')

plt.legend(loc="upper left")

- Plotting the Market Volume Rebalance Weights

marketVolumeRebalanceWeights.plot(figsize=(12,6))

plt.grid()

plt.title('Market Volume Rebalanced Weights')

plt.legend(loc="upper left")

- Calculating the portfolio cumulative returns

#D. Cumulative Returns Calculation

def calculate_cumulative_portfolio_returns(returns, rebalance_weights):

# Initializing the series for portfolio returns

portfolio_returns = pd.Series(index=returns.index)

# Example usage of the function with example data

n_col = len(rebalance_weights.columns)

initial_weights = pd.Series([1/n_col] * n_col, index=rebalance_weights.columns)

# Setting current weights to initial weights

current_weights = initial_weights

# Iterating through each date in the returns dataframe

for date, daily_returns in returns.iterrows():

if date != returns.index.min():

# Check if there's a rebalance for this date and update weights if needed

if date in rebalance_weights.index:

current_weights = rebalance_weights.loc[date]

# Calculating the daily portfolio return

portfolio_return = (daily_returns * current_weights).sum()

portfolio_returns[date] = portfolio_return

# Adjusting current_weights based on daily returns

current_weights *= (1 + daily_returns)

# Normalizing the weights so they sum up to 1

current_weights /= current_weights.sum()

# Calculating cumulative portfolio returns

cumulative_portfolio_returns = (1 + portfolio_returns).cumprod()

return cumulative_portfolio_returns

# Calculate cumulative returns

optimizedmarketVolumeWeightsCumulativeReturn = calculate_cumulative_portfolio_returns(returns, marketVolumeRebalanceWeights)

optimizeddividendYieldWeightsCumulativeReturn = calculate_cumulative_portfolio_returns(returns, dividendYieldRebalanceWeights)- Comparing Market Volume Portfolio Cumulative Returns vs Dividend Yield Portfolio Cumulative Returns

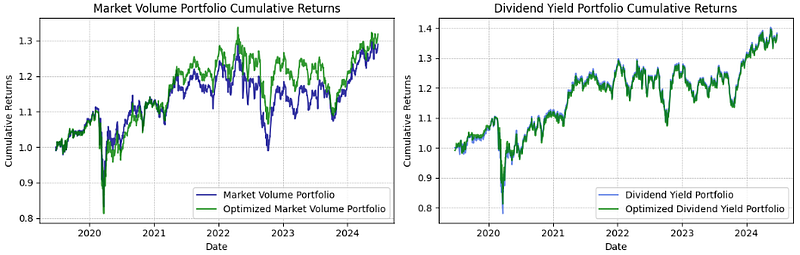

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(12, 4))

ax1.plot(marketVolumeWeightsCumulativeReturn, label='Market Volume Portfolio', alpha=0.8, color='darkblue')

ax1.plot(optimizedmarketVolumeWeightsCumulativeReturn, label='Optimized Market Volume Portfolio', alpha=0.8, color='green')

ax1.set_title('Market Volume Portfolio Cumulative Returns')

ax1.set_xlabel('Date')

ax1.set_ylabel('Cumulative Returns')

ax1.legend(loc='lower right')

ax1.grid(True, which='both', linestyle='--', linewidth=0.5)

ax2.plot(dividendYieldWeightsCumulativeReturn, label='Dividend Yield Portfolio', alpha=0.8, color='royalblue')

ax2.plot(optimizeddividendYieldWeightsCumulativeReturn, label='Optimized Dividend Yield Portfolio', alpha=0.8, color='green')

ax2.set_title('Dividend Yield Portfolio Cumulative Returns')

ax2.set_xlabel('Date')

ax2.set_ylabel('Cumulative Returns')

ax2.legend(loc='lower right')

ax2.grid(True, which='both', linestyle='--', linewidth=0.5)

plt.tight_layout()

plt.show()

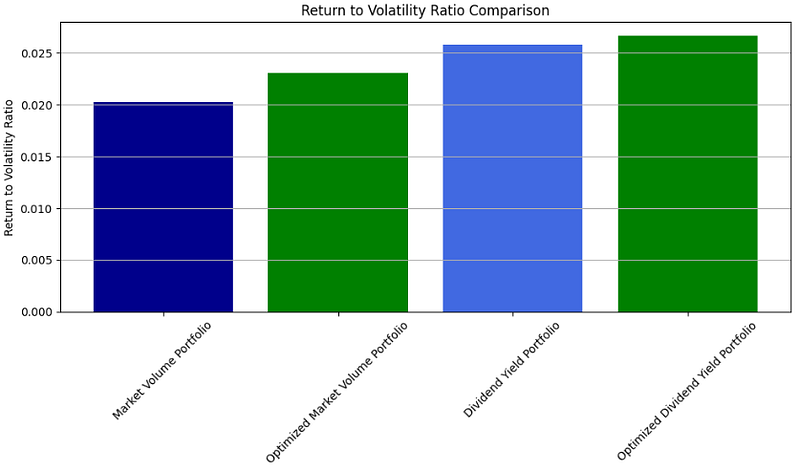

- Comparing the Return/Volatility Ratios before/after PO: Market Volume Portfolio vs Dividend Yield Portfolio

#E. Return to Volatility Ratio

def return_to_volatility_ratio(portfolio_returns):

mean_return = portfolio_returns.mean()

std_return = portfolio_returns.std()

ratio = mean_return / std_return

return ratio

# Calculating return_to_volatility_ratio for each portfolio

ratios = {

'Market Volume Portfolio': return_to_volatility_ratio(marketVolumeWeightsCumulativeReturn.diff().dropna()),

'Optimized Market Volume Portfolio': return_to_volatility_ratio(optimizedmarketVolumeWeightsCumulativeReturn.diff().dropna()),

'Dividend Yield Portfolio': return_to_volatility_ratio(dividendYieldWeightsCumulativeReturn.diff().dropna()),

'Optimized Dividend Yield Portfolio': return_to_volatility_ratio(optimizeddividendYieldWeightsCumulativeReturn.diff().dropna())

}

plt.figure(figsize=(10, 6))

plt.bar(ratios.keys(), ratios.values(), color=['darkblue', 'green', 'royalblue', 'green'])

plt.title('Return to Volatility Ratio Comparison')

plt.ylabel('Return to Volatility Ratio')

plt.xticks(rotation=45)

plt.grid(axis='y')

plt.tight_layout()

plt.show()

Breakout Strategy Stock Analysis (Portfolio 3)

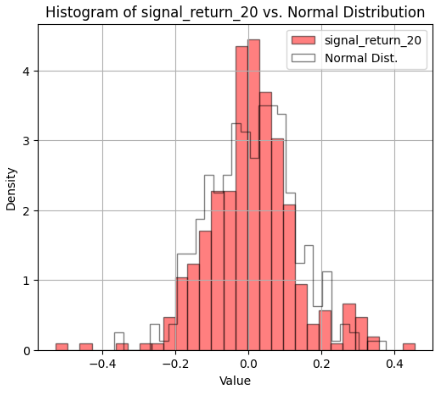

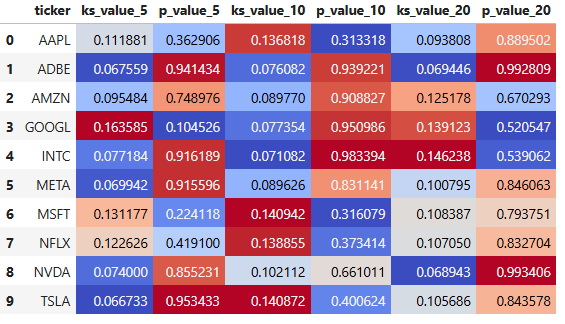

Here, we’ll discuss the Breakout Strategy with the emphasis on the Shapiro-Wilk (SW) and Kolmogorov-Smirnov (KS) statistical tests in analyzing stock return distributions, viz. Part 1: Fetching Stock Data; Part 2: Compute the Highs and Lows in a Window; Part 3: Compute Long and Short Signals; Part 4: Filter Signal; Part 5: Lookahead Close Prices & Price Returns; Part 6: Compute the Signal Return; Part 7: Analysis and Visualization of Signal Returns.

- Importing the necessary libraries and defining 5Y Portfolio 3 (10 stocks)

# Import necessary libraries

import yfinance as yf

import pandas as pd

from datetime import datetime, timedelta

import numpy as np

import json

import plotly.graph_objects as go

import matplotlib.pyplot as plt

ticker_list = ['AAPL', 'AMZN', 'MSFT', 'GOOGL', 'META', 'TSLA', 'NVDA', 'ADBE', 'NFLX', 'INTC']

years = 5- Part 1: Fetching Stock Data

#Part 1: Fetching Stock Data

def fetch_stock_data(ticker_list, years=5):

end_date = datetime.now()

start_date = end_date - timedelta(days=years * 365)

close_data_df = pd.DataFrame()

high_data_df = pd.DataFrame()

low_data_df = pd.DataFrame()

for ticker in ticker_list:

stock = yf.Ticker(ticker)

hist_data = stock.history(period='1d', start=start_date, end=end_date)

close_data = hist_data['Close'].rename(ticker)

close_data_df = pd.merge(close_data_df, pd.DataFrame(close_data), left_index=True, right_index=True, how='outer')

high_data = hist_data['High'].rename(ticker)

high_data_df = pd.merge(high_data_df, pd.DataFrame(high_data), left_index=True, right_index=True, how='outer')

low_data = hist_data['Low'].rename(ticker)

low_data_df = pd.merge(low_data_df, pd.DataFrame(low_data), left_index=True, right_index=True, how='outer')

return close_data_df, high_data_df, low_data_df

close, high, low = fetch_stock_data(ticker_list, years)- Part 2: Compute the Highs and Lows in a 50-day Window

#Part 2: Compute the Highs and Lows in a Window

def get_high_lows_lookback(high, low, lookback_days):

lookback_high = high.shift(1).rolling(lookback_days).max()

lookback_low = low.shift(1).rolling(lookback_days).min()

return lookback_high, lookback_low

lookback_days = 50

lookback_high, lookback_low = get_high_lows_lookback(high, low, lookback_days)- Part 3: Compute Long and Short Signals

#Part 3: Compute Long and Short Signals

def get_long_short(close, lookback_high, lookback_low):

long_signal = (close-lookback_high > 0).astype('int')

short_signal = -(close-lookback_low < 0).astype('int')

long_short = short_signal + long_signal

return long_short

signal = get_long_short(close, lookback_high, lookback_low)- Part 4: Filter Signal

#Part 4: Filter Signal

def clear_signals(signals, window_size):

clean_signals = [0]*window_size

for signal_i, current_signal in enumerate(signals):

has_past_signal = bool(sum(clean_signals[signal_i:signal_i+window_size]))

clean_signals.append(not has_past_signal and current_signal)

clean_signals = clean_signals[window_size:]

return pd.Series(np.array(clean_signals).astype(int), signals.index)

def filter_signals(signal, lookahead_days):

long_signals = (signal > 0 ).astype('int')

short_signals = -(signal < 0 ).astype('int')

long_signals = long_signals.apply(lambda s: clear_signals(s, window_size = lookahead_days))

short_signals = short_signals.apply(lambda s: clear_signals(s, window_size = lookahead_days))

filtered_signal = long_signals + short_signals

return filtered_signal

signal_5 = filter_signals(signal, 5)

signal_10 = filter_signals(signal, 10)

signal_20 = filter_signals(signal, 20)- Part 5: Lookahead Close Prices & Price Returns

#Part 5: Lookahead Close Prices & Price Returns

def get_lookahead_prices(close, lookahead_days):

lookahead_prices = close.shift(-lookahead_days)

return lookahead_prices

lookahead_5 = get_lookahead_prices(close, 5)

lookahead_10 = get_lookahead_prices(close, 10)

lookahead_20 = get_lookahead_prices(close, 20)

def get_return_lookahead(close, lookahead_prices):

lookahead_returns = np.log(lookahead_prices/close)

return lookahead_returns

price_return_5 = get_return_lookahead(close, lookahead_5)

price_return_10 = get_return_lookahead(close, lookahead_10)

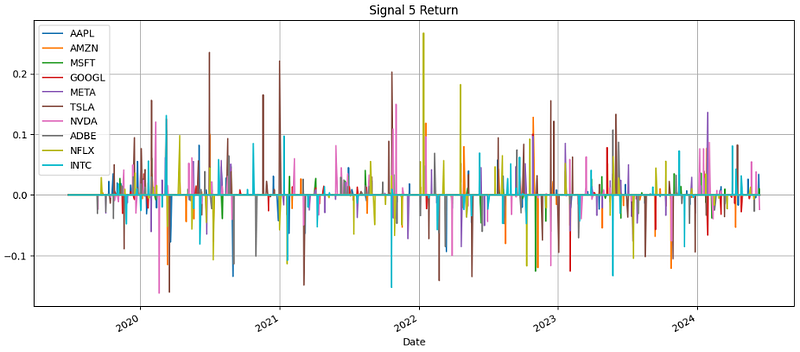

price_return_20 = get_return_lookahead(close, lookahead_20)- Part 6: Compute the Signal Return

#Part 6: Compute the Signal Return

def get_signal_return(signal, lookahead_returns):

signal_return = signal * lookahead_returns

return signal_return

signal_return_5 = get_signal_return(signal_5, price_return_5)

signal_return_10 = get_signal_return(signal_10, price_return_10)

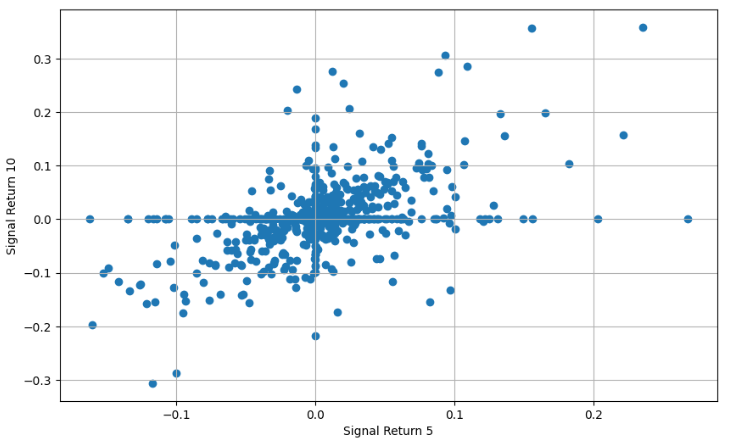

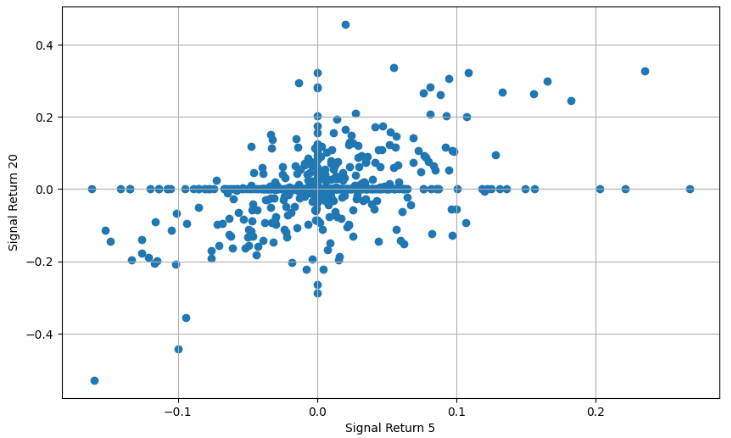

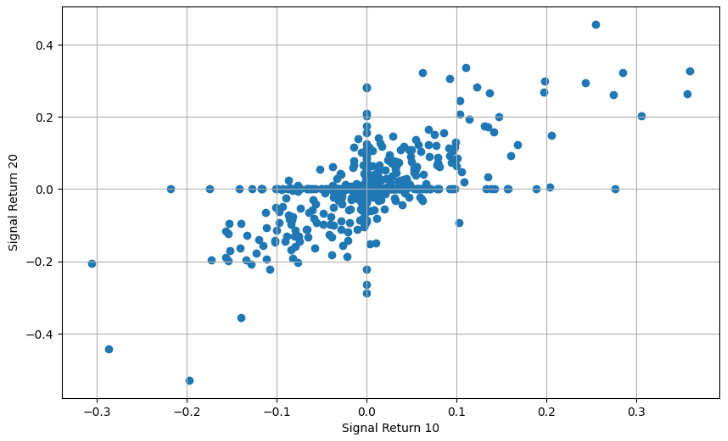

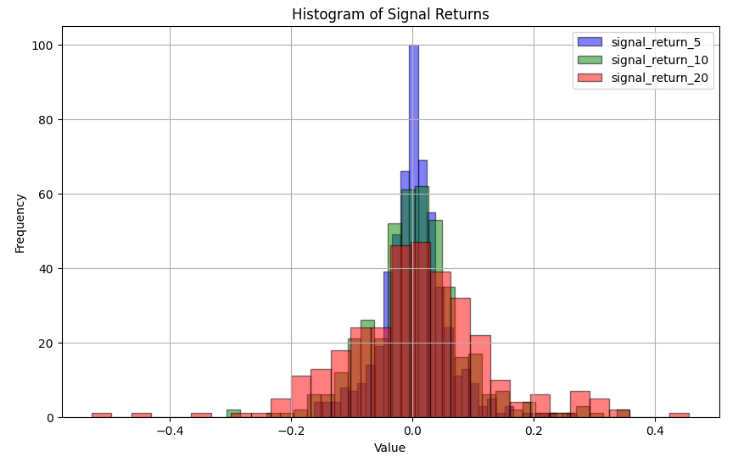

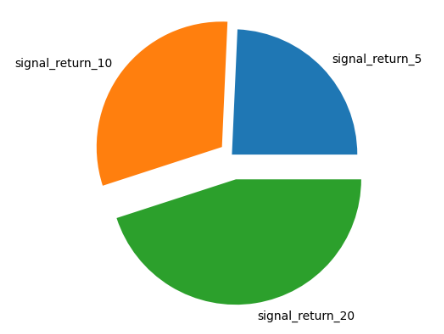

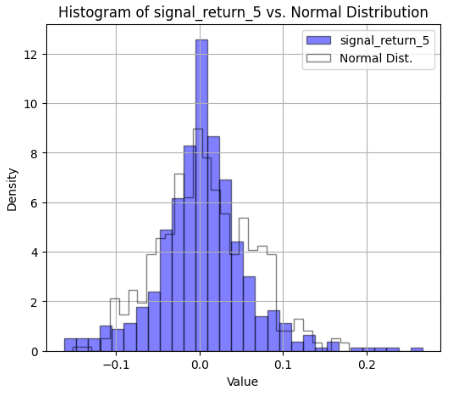

signal_return_20 = get_signal_return(signal_20, price_return_20)- Plotting Signal 5 Return

import matplotlib.pyplot as plt

signal_return_5.plot(figsize=(14,6))

plt.grid()

plt.title("Signal 5 Return")

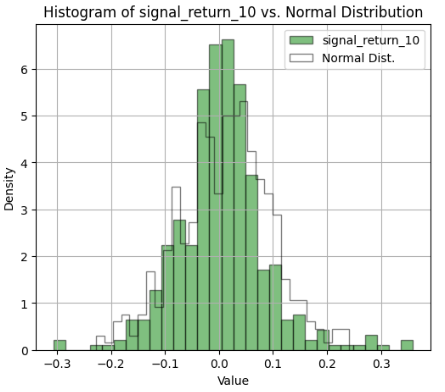

- Plotting Signal 10 Return

signal_return_10.plot(figsize=(14,6))

plt.grid()

plt.legend(loc="lower left")

plt.title("Signal 10 Return")

- Plotting Signal 20 Return

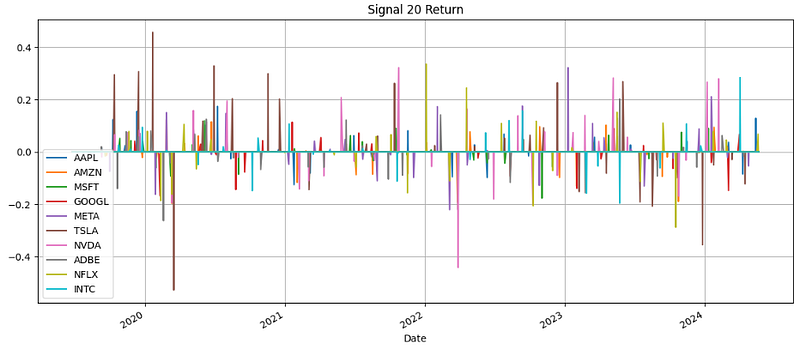

signal_return_20.plot(figsize=(14,6))

plt.grid()

plt.legend(loc="lower left")

plt.title("Signal 20 Return")

- See Appendix A v.i. for further details of the Breakout Strategy Stock Analysis (Portfolio 3).

Momentum Strategy Stock Analysis (Portfolio 3)

- In this section, we’ll share our experience with implementing a momentum trading strategy that relies on the price moving average, viz. Part 1: Fetching Stock Data; Part 2: Momentum Strategy Simulation; Part 3: Simulating Individual Stock Investments; Part 4: Calculating ROI/Risk Metrics; Part 5: Visualization Summary of Investment Results.

- Our focus will be the market momentum that measures an asset’s speed or velocity — the greater the momentum, the longer a price trend can sustain itself.

- Importing the necessary libraries

# Import necessary libraries

import yfinance as yf

import pandas as pd

from datetime import datetime, timedelta

import numpy as np

import json

import plotly.graph_objects as go- Part 1: Fetching Stock Data

#Part 1: Fetching Stock Data

def fetch_stock_data(ticker_list, years=5):

end_date = datetime.now()

start_date = end_date - timedelta(days=years * 365)

stock_data = pd.DataFrame()

for ticker in ticker_list:

stock = yf.Ticker(ticker)

hist_data = stock.history(period='1d', start=start_date, end=end_date)

close_data = hist_data['Close'].rename(ticker)

stock_data = pd.merge(stock_data, pd.DataFrame(close_data), left_index=True, right_index=True, how='outer')

return stock_data

# Fetch the data

ticker_list = ['AAPL', 'AMZN', 'MSFT', 'GOOGL', 'META', 'TSLA', 'NVDA', 'ADBE', 'NFLX', 'INTC']

years = 5

daily_data = fetch_stock_data(ticker_list, years)

daily_data

AAPL AMZN MSFT GOOGL META TSLA NVDA ADBE NFLX INTC

Date

2019-06-26 00:00:00-04:00 48.206604 94.891502 127.728485 53.954075 187.275162 14.618000 3.958648 288.720001 362.200012 42.258209

2019-06-27 00:00:00-04:00 48.192123 95.213997 127.938271 53.769791 189.111389 14.856000 4.057328 293.230011 370.019989 41.618061

2019-06-28 00:00:00-04:00 47.753010 94.681503 127.757080 54.077934 192.604202 14.897333 4.082186 294.649994 367.320007 41.977592

2019-07-01 00:00:00-04:00 48.628838 96.109497 129.397415 54.936951 192.604202 15.144667 4.130407 300.970001 374.600006 42.135429

2019-07-02 00:00:00-04:00 48.913532 96.715500 130.255768 55.566227 194.600113 14.970000 4.032472 301.390015 375.429993 42.196819

... ... ... ... ... ... ... ... ... ... ...

2024-06-14 00:00:00-04:00 212.490005 183.660004 442.570007 176.789993 504.160004 178.009995 131.880005 525.309998 669.380005 30.450001

2024-06-17 00:00:00-04:00 216.669998 184.059998 448.369995 177.240005 506.630005 187.440002 130.979996 518.739990 675.830017 30.980000

2024-06-18 00:00:00-04:00 214.289993 182.809998 446.339996 175.089996 499.489990 184.860001 135.580002 522.250000 685.669983 30.629999

2024-06-20 00:00:00-04:00 209.679993 186.100006 445.700012 176.300003 501.700012 181.570007 130.779999 522.950012 679.030029 30.620001

2024-06-21 00:00:00-04:00 207.490005 189.080002 449.779999 179.630005 494.779999 183.009995 126.570000 533.440002 686.119995 31.090000

1256 rows × 10 columns- Part 2: Momentum Strategy Simulation with initial_amount = 100k

#Part 2: Momentum Strategy Simulation

# Resample data to different frequencies: daily, weekly, monthly

def resample_data(data, period):

if period == 'D':

return data

elif period == 'W':

return data.resample('W').last()

elif period == 'M':

return data.resample('M').last()

# Simulate a simple momentum strategy based on log returns

def simulate_momentum_strategy(data, initial_amount, top_n, tax_rate, period='M'):

data = resample_data(data, period)

log_returns = np.log(data / data.shift(1))

simulation_details = pd.DataFrame(index=log_returns.index,

columns=['Selected Stocks', 'Profit Before Tax', 'Tax Paid', 'Portfolio Value'])

cash = initial_amount

# Logic to select top stocks and calculate portfolio value

for i in range(0, len(log_returns) - 1):

# Identify the top_n performing stocks based on past log returns

top_stocks = log_returns.iloc[i].sort_values(ascending=False).head(top_n)

# Filter out stocks with negative returns

top_stocks = top_stocks[top_stocks > 0]

if not top_stocks.empty:

simulation_details.loc[log_returns.index[i + 1], 'Selected Stocks'] = json.dumps(top_stocks.index.tolist())

# Calculate the amount to allocate for each stock

num_stocks = len(top_stocks)

allocation_per_stock = cash / num_stocks

# Calculate new portfolio value based on the next day's returns

new_value = sum(allocation_per_stock * np.exp(log_returns.loc[log_returns.index[i + 1], stock]) for stock in top_stocks.index)

# Calculate and deduct tax if there is a profit

profit = new_value - cash

simulation_details.loc[log_returns.index[i + 1], 'Profit Before Tax'] = round(profit, 2)

if profit > 0:

tax = profit * tax_rate

new_value -= tax

simulation_details.loc[log_returns.index[i + 1], 'Tax Paid'] = round(tax, 2)

simulation_details.loc[log_returns.index[i + 1], 'Portfolio Value'] = round(new_value, 2)

else:

# No allocation, so portfolio value remains the same

simulation_details.loc[log_returns.index[i + 1], 'Portfolio Value'] = cash

# Update cash amount for the next round

cash = simulation_details.loc[log_returns.index[i + 1], 'Portfolio Value']

# Assign the initial amount to the first row

simulation_details.loc[log_returns.index[0], 'Portfolio Value'] = initial_amount

return simulation_details

# Configuration for the momentum strategy simulation

initial_amount = 100000

top_n = 3

tax_rate = 0.15

frequency = 'M'

simulation_details = simulate_momentum_strategy(daily_data, initial_amount, top_n, tax_rate, frequency)

simulation_details

Selected Stocks Profit Before Tax Tax Paid Portfolio Value

Date

2019-06-30 00:00:00-04:00 NaN NaN NaN 100000

2019-07-31 00:00:00-04:00 NaN NaN NaN 100000

2019-08-31 00:00:00-04:00 ["GOOGL", "TSLA", "AAPL"] -3513.24 NaN 96486.76

2019-09-30 00:00:00-04:00 ["MSFT"] 818.87 122.83 97182.8

2019-10-31 00:00:00-04:00 ["INTC", "AAPL", "TSLA"] 16687.67 2503.15 111367.32

... ... ... ... ...

2024-02-29 00:00:00-05:00 ["NVDA", "NFLX", "META"] 128147.57 19222.14 736860.1

2024-03-31 00:00:00-04:00 ["NVDA", "META", "AMZN"] 37672.64 5650.9 768881.85

2024-04-30 00:00:00-04:00 ["NVDA", "GOOGL", "INTC"] -70586.48 NaN 698295.37

2024-05-31 00:00:00-04:00 ["GOOGL", "TSLA"] 10942.48 1641.37 707596.48

2024-06-30 00:00:00-04:00 ["NVDA", "NFLX", "AAPL"] 71516.88 10727.53 768385.83

61 rows × 4 columns- Part 3: Simulating Individual Stock Investments

#Part 3: Simulating Individual Stock Investments

# Simulate how each individual stock would have performed over the same period

def track_individual_investments(data, initial_amount, simulation_details, period='W'):

# Resample data based on the specified period

data = resample_data(data, period)

# Calculate returns based on the resampled data

returns = data.pct_change()

# Create a new DataFrame to store individual stock values over time

individual_investments = pd.DataFrame(index=data.index, columns=data.columns)

for stock in data.columns:

# Simulate an investment in each stock

individual_investments[stock] = (1 + returns[stock]).cumprod() * initial_amount

# Include the Portfolio Value from the momentum strategy

individual_investments['Portfolio Value'] = simulation_details['Portfolio Value']

individual_investments['Baseline'] = individual_investments.iloc[:, :-1].T.mean()

# Adjust the first values to match the Initial Amount.

individual_investments.iloc[0, :] = initial_amount

return individual_investments.fillna(0).astype(int)

individual_investments_df = track_individual_investments(daily_data, initial_amount, simulation_details, frequency)

individual_investments_df

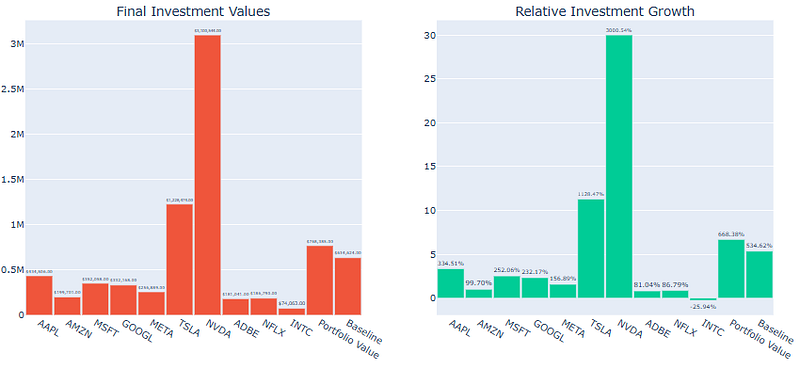

AAPL AMZN MSFT GOOGL META TSLA NVDA ADBE NFLX INTC Portfolio Value Baseline

Date

2019-06-30 00:00:00-04:00 100000 100000 100000 100000 100000 100000 100000 100000 100000 100000 100000 100000

2019-07-31 00:00:00-04:00 107639 98582 101724 112504 100637 108122 102733 101428 87931 105598 100000 102690

2019-08-31 00:00:00-04:00 105867 93803 103254 109949 96202 100962 102098 96558 79971 99707 96486 98837

2019-09-30 00:00:00-04:00 113591 91671 104130 112776 92269 107791 106096 93755 72857 108372 97182 100331

2019-10-31 00:00:00-04:00 126164 93822 107380 116254 99300 140929 122522 94325 78245 118887 111367 109783

... ... ... ... ... ... ... ... ... ... ... ... ...

2024-02-29 00:00:00-05:00 377997 186689 323187 255744 254222 1355141 1937731 190151 164140 102139 736860 514714

2024-03-31 00:00:00-04:00 358611 190512 328719 278777 251862 1180009 2213240 171254 165340 104797 768881 524312

2024-04-30 00:00:00-04:00 356206 184830 304193 300664 223122 1230287 2116388 157077 149907 72292 698295 509497

2024-05-31 00:00:00-04:00 402592 186351 324936 318618 242137 1195381 2685424 150945 174676 73491 707596 575455

2024-06-30 00:00:00-04:00 434506 199701 352058 332168 256889 1228474 3100544 181041 186790 74063 768385 634624

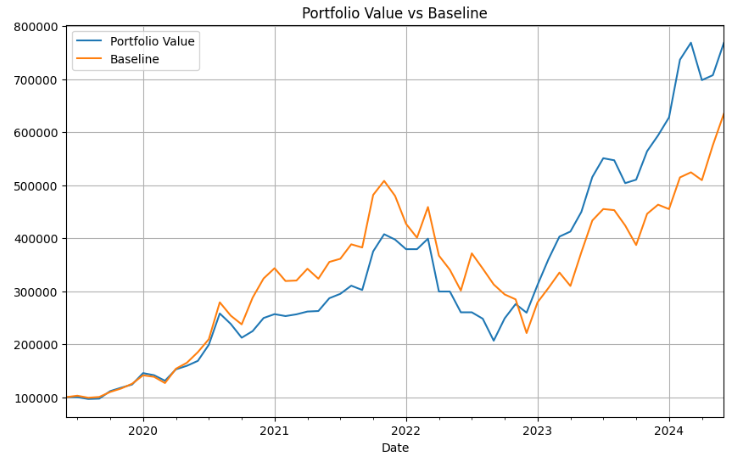

61 rows × 12 columns- Plotting Portfolio Value vs Baseline

plt.figure(figsize=(10, 6))

individual_investments_df['Portfolio Value'].plot(label='Portfolio Value')

individual_investments_df['Baseline'].plot(label='Baseline')

plt.legend()

plt.grid()

plt.title('Portfolio Value vs Baseline')

plt.show()

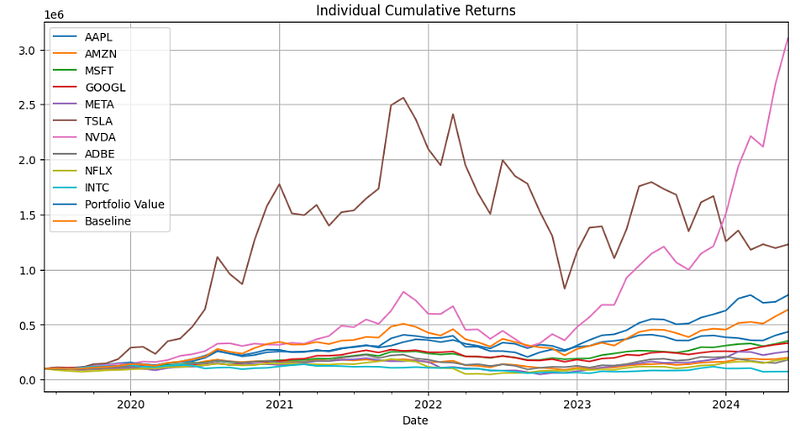

- Plotting Individual Cumulative Returns vs Portfolio Value & Baseline

individual_investments_df.plot(figsize=(12, 6))

plt.title('Individual Cumulative Returns')

plt.grid()

plt.show()

- Part 4: Calculating Metrics

#Part 4: Calculating Metrics

from scipy.stats import ttest_1samp

def calculate_sharpe_ratio(returns, annual_risk_free_rate=0.01, frequency='D'):

# Adjust the risk-free rate based on the frequency

if frequency == 'D':

adjusted_rfr = (1 + annual_risk_free_rate) ** (1/252) - 1

elif frequency == 'W':

adjusted_rfr = (1 + annual_risk_free_rate) ** (1/52) - 1

elif frequency == 'M':

adjusted_rfr = (1 + annual_risk_free_rate) ** (1/12) - 1

excess_returns = returns - adjusted_rfr

return excess_returns.mean() / excess_returns.std()

def t_test_portfolio_returns(portfolio_returns, bench_annual_rate=0.1, frequency='D'):

# Adjust the risk-free rate based on the frequency

if frequency == 'D':

adjusted_rfr = (1 + bench_annual_rate) ** (1/252) - 1

elif frequency == 'W':

adjusted_rfr = (1 + bench_annual_rate) ** (1/52) - 1

elif frequency == 'M':

adjusted_rfr = (1 + bench_annual_rate) ** (1/12) - 1

t_stat, p_value = ttest_1samp(portfolio_returns[1:], adjusted_rfr) # [1:] to exclude the NaN from pct_change

return t_stat, p_value

def calculate_metrics(dataframe, initial_amount, bench_annual_rate, frequency='D'):

# Calculate the final and relative values

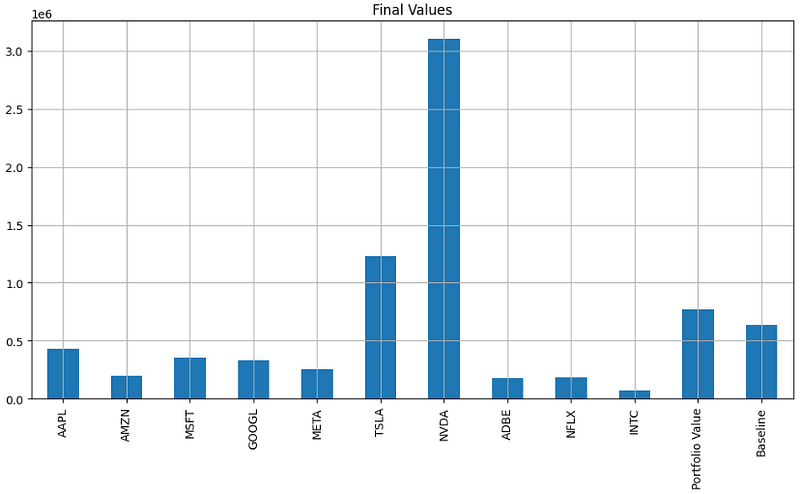

final_values = dataframe.iloc[-1]

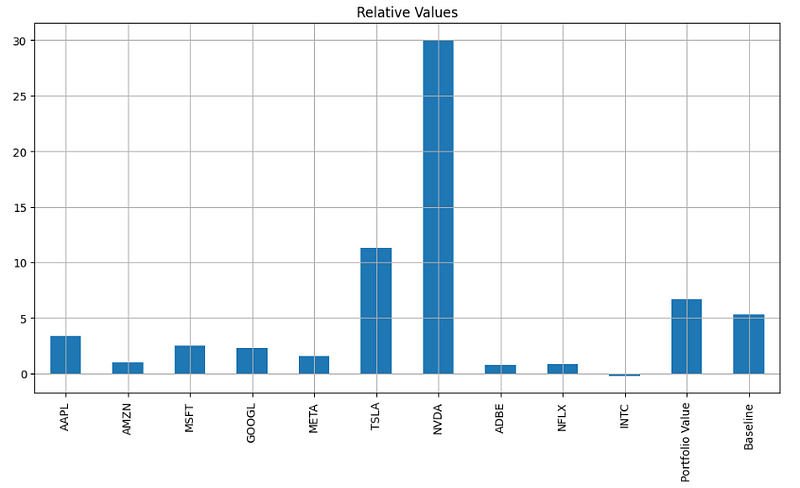

relative_values = final_values / initial_amount - 1 # Subtract 1 to get the growth proportion

# Calculate mean return and Sharpe Ratio

returns = dataframe.pct_change()

if frequency == 'D':

annualization_factor = 252

elif frequency == 'W':

annualization_factor = 52

elif frequency == 'M':

annualization_factor = 12

# Corrected annualization of mean returns

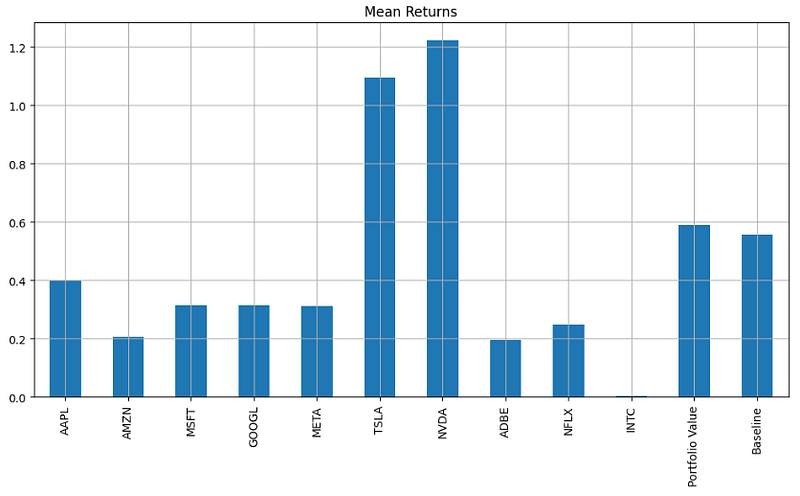

mean_returns = (1 + returns.mean()) ** annualization_factor - 1

sharpes = returns.apply(calculate_sharpe_ratio, annual_risk_free_rate=0.01, frequency=frequency)

# Test if the portfolio returns are greater than the adjusted risk-free rate

portfolio_returns = dataframe['Portfolio Value'].pct_change()

t_stat, p_value = t_test_portfolio_returns(portfolio_returns, bench_annual_rate, frequency=frequency)

return final_values, relative_values, mean_returns, sharpes, t_stat, p_value / 2

bench_annual_rate = 0.1

# Calculate the metrics

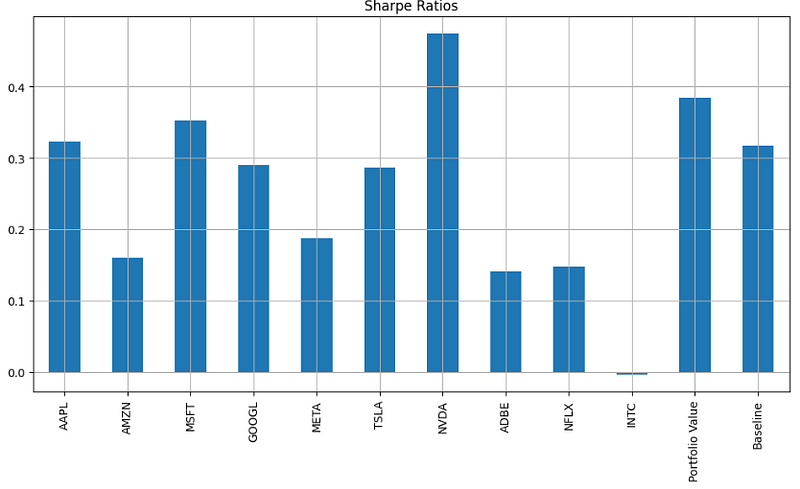

final_values, relative_values, mean_returns, sharpes, t_stat, p_value = calculate_metrics(individual_investments_df, initial_amount, bench_annual_rate, frequency)- Plotting the Sharpe Ratios

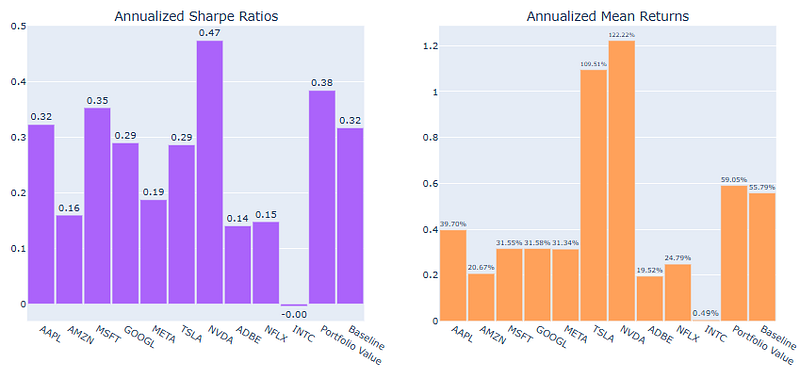

sharpes.plot.bar(figsize=(12, 6))

plt.title('Sharpe Ratios')

plt.grid()

plt.show()

- Printing the p-value and t-statistic

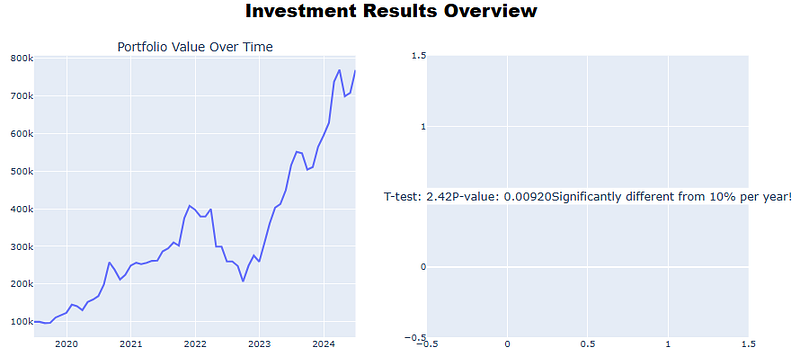

print(p_value)

0.009201411022319347

print(t_stat)

2.424687499520688

mean_returns.plot.bar(figsize=(12, 6))

plt.title('Mean Returns')

plt.grid()

plt.show()

- Plotting Relative Values

relative_values.plot.bar(figsize=(12, 6))

plt.title('Relative Values')

plt.grid()

plt.show()

- Plotting Final Values

final_values.plot.bar(figsize=(12, 6))

plt.title('Final Values')

plt.grid()

plt.show()

- Part 5: Final Visualization

#Part 5: Visualization

import plotly.graph_objects as go

from plotly.subplots import make_subplots

def plot_combined_charts(dataframe, final_values, relative_values, sharpes, mean_returns):

labels = final_values.index

colors = ['#636EFA', '#EF553B', '#00CC96', '#AB63FA', '#FFA15A']

fig = make_subplots(rows=3, cols=2,

subplot_titles=('Portfolio Value Over Time',

'',

'Final Investment Values',

'Relative Investment Growth',

'Annualized Sharpe Ratios',

'Annualized Mean Returns'),

vertical_spacing=0.08)

# Portfolio Value line chart

fig.add_trace(go.Scatter(x=dataframe.index,

y=dataframe['Portfolio Value'],

mode='lines',

name='Portfolio Value',

line=dict(color=colors[0], width=2.5)),

row=1, col=1)

# T-test and P-value

significance_text = f"T-test: {t_stat:.2f}P-value: {p_value:.5f}"

if t_stat > 2 and p_value < 0.05:

significance_text += f"Significantly different from {bench_annual_rate:.0%} per year!"

fig.add_annotation(

text=significance_text,

showarrow=False,

xref="x2", yref="y2",

x=0.5, y=0.5,

font=dict(size=15),

bgcolor="white",

align="center"

)

# Final values

fig.add_trace(go.Bar(x=labels,

y=final_values.values,

name='Final Values ($)',

text=[f"${v:,.2f}" for v in final_values.values],

textposition='outside',

marker_color=colors[1]),

row=2, col=1)

# Relative Growth

fig.add_trace(go.Bar(x=labels,

y=relative_values.values,

name='Relative Growth',

text=[f"{v:.2%}" for v in relative_values.values],

textposition='outside',

marker_color=colors[2]),

row=2, col=2)

# Sharpe Ratios

fig.add_trace(go.Bar(x=labels,

y=sharpes.values,

name='Annualized Sharpe Ratio',

text=[f"{v:.2f}" for v in sharpes.values],

textposition='outside',

marker_color=colors[3]),

row=3, col=1)

# Mean Returns

fig.add_trace(go.Bar(x=labels,

y=mean_returns.values,

name='Annualized Mean Returns',

text=[f"{v:.2%}" for v in mean_returns.values],

textposition='outside',

marker_color=colors[4]),

row=3, col=2)

# Update layout

fig.update_layout(title_text="Investment Results Overview",

title_font=dict(size=24, color='black', family="Arial Black"),

title_pad=dict(t=10),

showlegend=False,

height=1500,

title_x=0.5,

bargap=0.05,

)

fig.show()

plot_combined_charts(individual_investments_df, final_values, relative_values, sharpes, mean_returns)

Using Stock Fundamentals (Portfolio 4)

- Some momentum strategies emphasize fundamental analysis factors, such as quarterly or annual earnings per share (EPS) and other metrics, to avoid making emotional decisions.

- In this section, we will explain in detail how to retrieve stock data and financial statements using yfinance [13, 14] and relevant data visualizations [14].

- For simplicity, let’s consider only 2 big tech stocks, such as MSFT and NVDA (Portfolio 4).

- Importing libraries

import pandas as pd

import yahoo_fin.stock_info as si

import yfinance as yf

import plotly.express as px

import plotly.graph_objects as go

import matplotlib.pyplot as plt

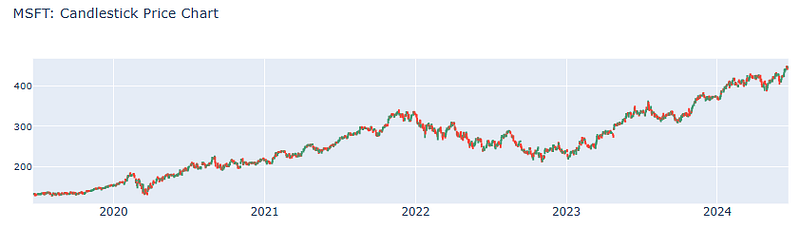

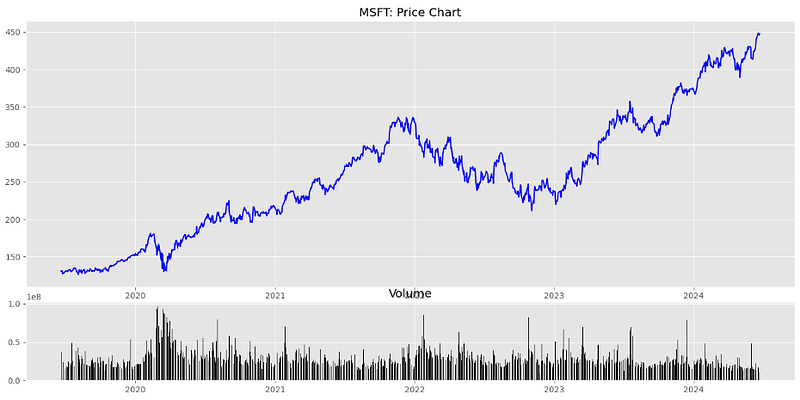

%matplotlib inline- MSFT 5Y Candlesticks, Price Charts vs Volume

company = 'MSFT' # Ticker of the company to be analyzed

df = yf.Ticker(company).history(period='5y',interval='1d')

fig = go.Figure(data=[go.Candlestick(x=df.index,

open=df['Open'],

high=df['High'],

low=df['Low'],

close=df['Close'])])

fig.update_layout(title = f'{company}: Candlestick Price Chart', xaxis_tickfont_size = 14)

fig.update_layout(xaxis_rangeslider_visible = False)

fig.show()

plt.style.use('ggplot')

top = plt.subplot2grid((4,4), (0, 0), rowspan=3, colspan=4)

top.plot(df.index, df["Close"], color='blue')

plt.title(f'{company}: Price Chart')

bottom = plt.subplot2grid((4,4), (3,0), rowspan=1, colspan=4)

bottom.bar(df.index, df['Volume'], color='black')

plt.title('Volume')

plt.gcf().set_size_inches(17,8)

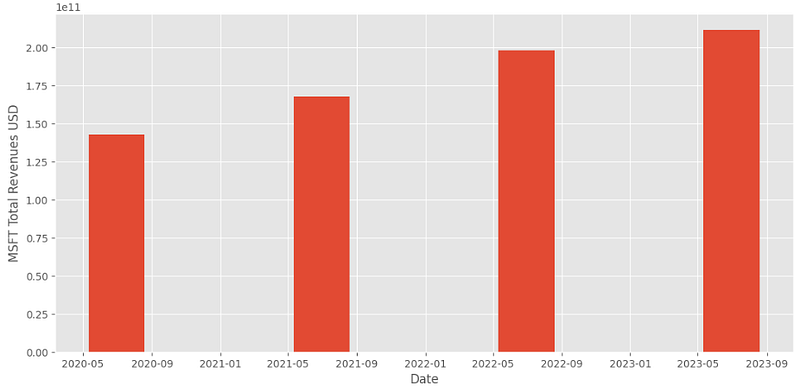

- Examining the MSFT Total Revenues USD for the available time period

# Import yfinance

import yfinance as yf

# Set the ticker as MSFT

msft = yf.Ticker("MSFT")

# show revenues

plt.figure(figsize=(13,6))

revenue = msft.financials.loc['Total Revenue']

plt.bar(revenue.index, revenue.values,width = 100)

plt.ylabel("MSFT Total Revenues USD")

plt.xlabel("Date")

plt.show()

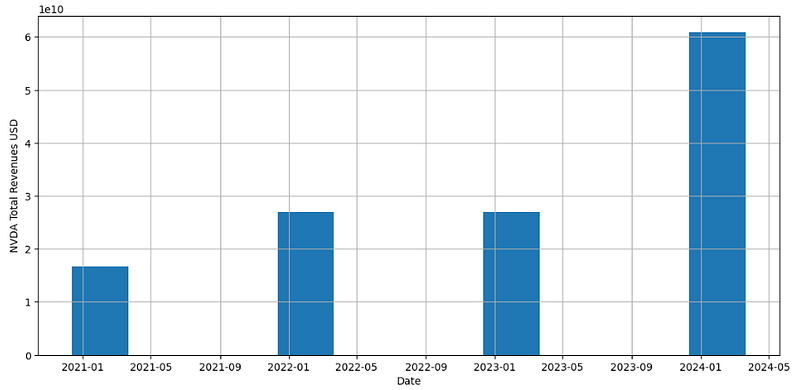

- Plotting the NVDA Total Revenues USD for the available time period

nvda = yf.Ticker("NVDA")

plt.figure(figsize=(13,6))

revenue = nvda.financials.loc['Total Revenue']

plt.bar(revenue.index, revenue.values,width = 100)

plt.ylabel("NVDA Total Revenues USD")

plt.xlabel("Date")

plt.grid()

plt.show()

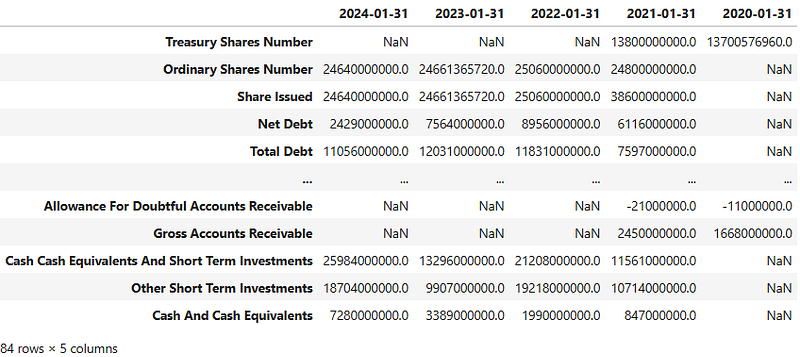

- Printing and plotting the NVDA balance sheet

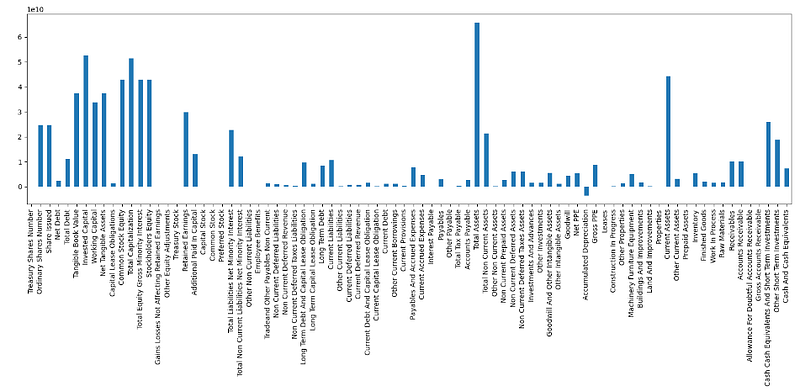

nvda.balance_sheet

bs=nvda.balance_sheet

bs['2024-01-31'].plot.bar(figsize=(20,5))

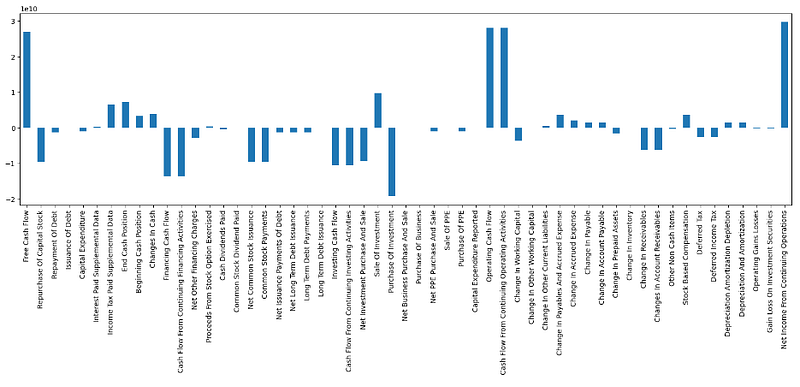

- Plotting the NVDA cashflow on 2024–01–31

cf=nvda.cashflow

cf['2024-01-31'].plot.bar(figsize=(20,5))

- Fetch the full company info

nvda.info

# cf. Appendix B

ninfo=nvda.info

ninfo['revenueGrowth']

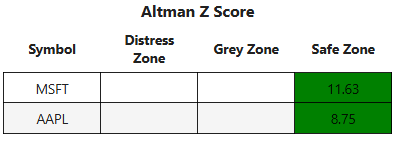

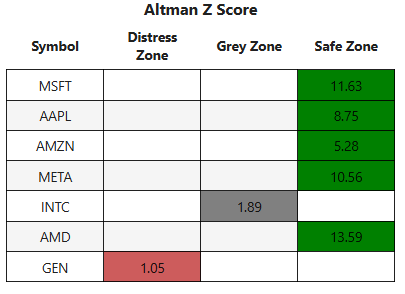

2.621The Altman Z-Score Revisited (Portfolio 5)

- Based on the above fundamental analysis , we’ll calculate the Altman Z-Score [12] by adopting the relevant Python functions and importing the required libraries such as

- yfinance: to access financial market data; imported as yf

- pandas : DataFrame and other utilities; imported as pd

- numpy: for nan; imported as np

- The Altman Z-Score assesses a company’s financial health and likelihood of bankruptcy based on multiple fundamental financial metrics to be discussed below.

- We’ll consider 5Y Portfolio 5:

ticker_list = ['MSFT','AAPL','AMZN','META','INTC','AMD','GEN']- Working with the MSFT balance sheet

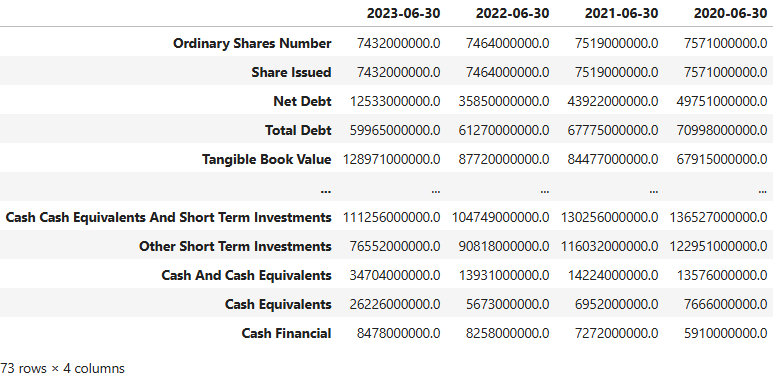

msft.balance_sheet

- Example fetching the MSFT Cash Financial on 2023–06–30

msbs=msft.balance_sheet

msbs1=msbs['2023-06-30']

msbs1['Cash Financial']

8478000000.0- Calculating ratio_x_1: working capital / total assets [12]

msbs1['Current Assets']

184257000000.0

working_capital = msbs1['Current Assets'] - msbs1['Current Liabilities']

total_assets = msbs1['Total Assets']

ratio_x_1=working_capital/total_assets

print(ratio_x_1)

0.1944482202846768- Calculating all 5 fundamental ratios [12]

import yfinance as yf

msft = yf.Ticker("MSFT")

ticker="MSFT"

date='2023-06-30'

# ratio_x_1: working capital / total assets

def ratio_x_1(ticker,date) -> float:

msft=yf.Ticker(ticker)

msbs=msft.balance_sheet

df=msbs[date]

working_capital = df['Current Assets'] - df['Current Liabilities']

total_assets = df['Total Assets']

return working_capital/total_assets

ratio_1=ratio_x_1(ticker,date)

print(ratio_1)

0.1944482202846768

def ratio_x_2(ticker,date) -> float:

msft=yf.Ticker(ticker)

msbs=msft.balance_sheet

df=msbs[date]

retained_earnings = df['Retained Earnings']

total_assets = df['Total Assets']

return retained_earnings/total_assets

ratio_2=ratio_x_2(ticker,date)

print(ratio_2)

0.28848282424218885

# earnings before interest and tax / total assets

def ratio_x_3(ticker,date) -> float:

msft=yf.Ticker(ticker)

msbs=msft.income_stmt

df = msbs[date]

ebit = df['EBIT']

msbs1=msft.balance_sheet

df1=msbs1[date]

total_assets = df1['Total Assets']

return ebit/total_assets

ratio_3=ratio_x_3(ticker,date)

print(ratio_3)

0.22156387750742762

# market value of equity / total liabilities

def ratio_x_4(ticker,date) -> float:

msft=yf.Ticker(ticker)

msin=msft.info

equity_market_value = msin['sharesOutstanding'] * msin['currentPrice']

msbs=msft.balance_sheet

df=msbs[date]

total_liabilities = df['Total Liabilities Net Minority Interest']

return equity_market_value/total_liabilities

ratio_4=ratio_x_4(ticker,date)

print(ratio_4)

16.247171530197857

# sales / total assets

def ratio_x_5(ticker,date) -> float:

msft=yf.Ticker(ticker)

msbs=msft.income_stmt

df = msbs[date]

sales = df['Total Revenue']

msbs1=msft.balance_sheet