Paradigm Shifts: A Nickel Crisis of Epic Proportions Reveals Insights on China-Russia Strategy

As the world marches on into the future after the Global COVID-19 Pandemic, understanding how Paradigm Shifts affect everyone’s structure and function in life is going to be a necessary element for everything related to the economy: how to make money; how to pay bills; how to find a job; how to influence people; how to you name it.

It’s also about Geopolitics. I’ve already written about two examples of recent international events in the global economy and commodities sector to indicate how conflict in the Indo-Pacific is likely to revolve around resource conflicts and energy security.

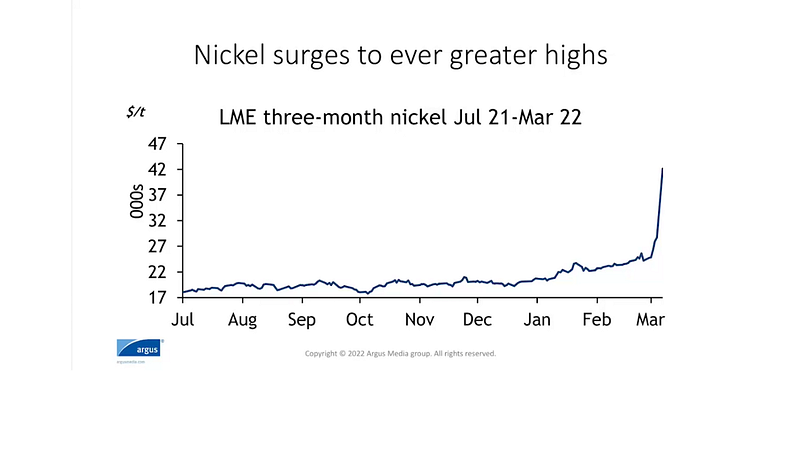

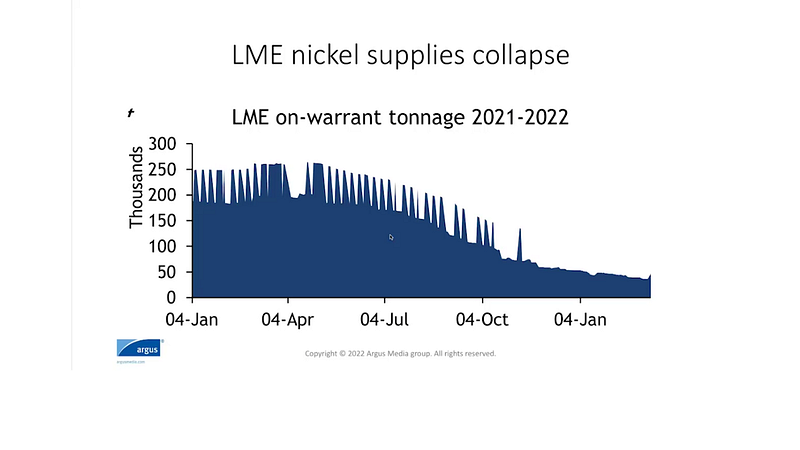

Paradigm Shifts are always prevalent in the Global Economy and Financial Markets. Looking at the future of the Global Economy from the perspective of Paradigm Shifts is one way to understand and live with uncertainty during volatile events. I’m writing here about one of the most volatile — I’d say the MOST volatile — event to occur in the economy this year: the London Metals Exchange (LME) had to shut down its nickel trading segement.

China’s Nickel Strategy in Indonesia

In March 2022, there was a substantial crisis for China’s nickel trading giant — Tsingshan Holding Group — led by Chinese Wenzhounese billonaire Xiang Guangda who bet zealously on the growth of nickel production and supply this year at the London Metals Exchange (LME). When the price of nickel surpassed $100,000 per tonne the LME had to stop nickel trading at an instant.

In response to the EV battery production shortages, Tsingshan Holding Group devised a strategy that would keep prices lower, and thus allow for cheaper production of battery ingredients, especially from areas of Southeast Asia like Indonesia. But unfortuantely the events in Ukraine have caused the markets to act in an extraordinary way — a way that was adverse to Tsingshan’s nickel production investment strategy.

New to trading? Try crypto trading bots or copy trading

Since March 8, 2022, international investors and bankers have been awaiting Tsingshan’s response. It wasn’t until March 15, 2022, that they finally announced an agreement with bank creditors, such as JP Morgan and CCBI Global Markets, to discuss a “standby secured liquidity facility” arrangement to solve the company’s problems. This agreement is being referred to by most sources as a standstill agreement for which it is expected that the haphazard nickel trading will once again stabilize.

The company released a statement, saying:

“As an integral feature of the agreement, there is provision for the existing hedge positions to be reduced by the Tsingshan group in a fair and orderly manner as abnormal market conditions subside.”

Any new rules will be applied by regulatory authorties in Great Britain: the Financial Conduct Authority (FCA) and the Bank of England.

For a more technical and financial point of view about what happened with LME nickel trading, read here: https://www.finews.asia/finance/36507-tsingshan-reaches-standstill-agreement-with-banks

This story about China’s Tsingshan Holdings Group sheds light on how critical the metals markets are becoming for global finance and investment banks.

With China’s capabilities to produce cheaply in Indonesia, and raise capital from the world’s largest international banks and financial institutions, I’d call this a recipe for stability and disaster offset by the production and supply of metals. This essential truth is even hidden within this story about the nickel industry: the whole point of the standstill agreement was to stabilize pricing and trading mechanisms to prevent a disaster in global markets.

Australia’s Nickel Strategy in Western Australia

The story begins with a scheme implementation deed (SID) agreed to in December 2021 when Australia’s IGO Ltd sought to acquire another Australian metals miner outfit, Western Areas Ltd, to boost its nickel and lithium portfolio. By adding some of the highest-grade nickel and lithium mines that Western Australia has to offer, IGO would be able to significantly take on the metal production base that is crucial to Electric Vehicles (EV) and Clean Energy Technologies.

Originally valued at A$1.096 billion, IGO would takeover Western Areas Ltd assets with a 100% interest in the mines in Western Australia. IGO appeared to be on its way to a massive acquisition that would put it at the top of Western Australia’s nickel production capacity. Until recently when the nickel trading mechanisms on the London Metals Exchange (LME) got out of control, causing China’s Tsingshan Holdings Group to hedge production against a surging nickel price that hit a whopping $100,000 a tonne.

Due to the events on LME the company was expecting only a “relatively short delay” for the takeover deal at first. It was then reported on April 5, 2022, that IGO would completely back out of the deal to acquire Western Areas — citing only an independent expert report as the rationale for foregoing the acquisition.

The example of Australia’s Western Areas conundrum reveals that the economy is going through what many experts are calling a Global Commodity Supercycle. The events on LME have been exacerbated by the Russia-Urkaine Conflict as well as China’s global economic and geopolitical dilemmas. That’s why I argue that Fertilizer and Metals are particularly vulnerable under these circumstances. Not to mention the various wars and geopolitical conundrums that have been widely ignored since the outbreak of the global Covid-19 pandemic. Many of these issues are not going to be resolved any time soon, and yet many of the most vulnerable areas are critical to global fertilizer and metals supply.

Fortunately, there seems to be a renewed vision of leadership in the Fertilizer and Metals industries around issues related to Environment, Social Governance (ESG). I have written extensively about the Nutrien Ltd. CEO transiton and BHP Group’s CEO Mike Henry.

And no one understands these problems better than Elon Musk.

Tesla’s and BHP’s Nickel Strategy

In Janurary 2020, Tesla began negotiations with Switzerland-based Glencore plc to purchase long-term supplies of cobalt at its Shanghai Gigafactory.

One of Tesla’s most important lithium suppliers is a Chinese company, Contemporary Amperex Technology (CATL). The two companies partnered up on a deal for CATL to supply Tesla with lithium-ion batteries from 2022–2025. This is possibly the most important partnership in the EV sector, as far as raw materials procurement is concerned.

This was soon followed up by Elon Musk’s famous quote to global metal miners:

“Any mining companies out there … wherever you are in the world, please mine more nickel…Tesla will give you a giant contract for a long period of time if you mine nickel efficiently and in an environmentally sensitive way.”

On July 21, 2021, BHP Group answered the call by signing a deal with Tesla to sustainably produce and supply battery metals from its Nickel West project in Western Australia. This was followed by another deal with USA-based Talon Metals to secure nickel supplies for a mine projected to begin production in 2026.

I wrote an extensive piece on Medium about deals for battery metals between Tesla’s CEO Elon Musk and BHP Group’s CEO Mike Henry. Read more about the deals for battery metals here: https://readmedium.com/elon-musk-made-a-deal-with-mike-henry-for-critical-metals-4354077b8c4d

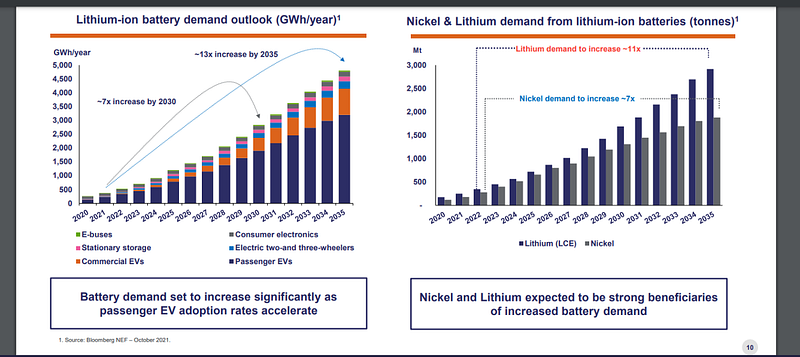

All of these developments in the critical metals space can’t be overstated for Tesla’s success as the world’s largest EV producer — the continuation of procuring raw materials will be the highest priority for the company going forward as new companies expand production and new partnerships emerge. It’s already been reported that automakers Ford and GM have secured lithium and cobalt supplies to enhance EV production.

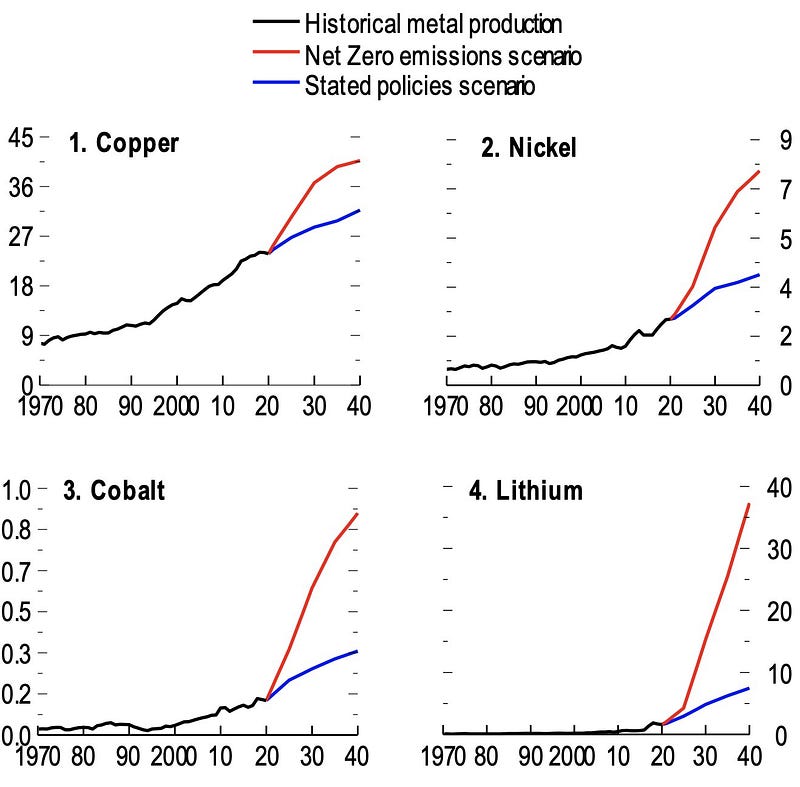

As the world is gravitating toward the Energy Transition, with a growing demand for Clean Energy Technologies and Electric Vehicles (EVs), more nickel is going to be needed.

The Strategic Implications of China-Russia Commodities

The world has seen numerous export bans on critical inputs to fertilizer and food production since the outbreak of Covid-19 in 2020. This circumstance has created a massive ripple effect on economies of the underdeveloped and undeveloped worlds, where civil unrest has become a source of tension for government stability in many countries of Middle East, Sub-Saharan Africa and South Asia.

Ukraine’s agriculture production has had an impact on the world’s food supply, notably due to wheat cultivation and production. Sanctions on China would only exacerbate the ongoing global food crisis which has seen significant strain to economic production all over the world, including in developing economies, where the historical highs in fertilizer prices has led to high crop prices and thus higher consumer prices at the wholesale and broader marketplace levels.

Imagine if the same tactics were applied by countries to target China’s metals production and supply? It would be disastorous for the Global Economy, as the massive rollout of EVs, renewable energy installations and more construction projects require massive amounts of copper and nickel — among other metals.

I wrote an extensive Medium story about Australia’s BHP Group and how the CEO is leading the mining indsutry’s future facing commodities — copper, nickel, potash — while on the front lines of ESG. Read more about this here: https://readmedium.com/why-is-the-worlds-largest-metal-miner-bhp-group-pushing-for-future-facing-commodities-on-the-1c6dd34ce681

There’s another trend happening whereby indigenous groups are organizing to stop economic endeavours in building and mining projects all over the world.

Just look at the example of the Amazon Rainforest. A British journalist is dead and the Brazilian government is looking deeper into an indigenous group’s claims that it was the result of rivalry between other indigenous groups over the government’s strategy to mine potash in the Amazon.

I say all of this to give an example of the larger trend — indigenous groups are coming out in opposition as more and more mining projects are being put in the works to spur economic activity during the gobal commodity supercycle.

Many of these mining projects, especially the ones for potash, copper and nickel, are critical to achieving both the Energy Transition and the Electric Vehicle (EV) production rollout.

Furthermore, rising prices for food and fertilizer will cause Ukraine’s agriculture industry to take a major hit, thus deteriorating Ukraine’s Global Domestic Product (GDP) growth. In Ukraine, food prices are going to be a long-term problem for the government’s stability in the aftermath of Russia’s invasion. This is a scenario that would play into Russia’s favor, whereby it is one of the world’s largest fertilizer producers and exporters. Russia is already engaging countries dependent on fertilizer imports with “fertilizer diplomacy.”

I argue that China is likely to face tough decisions in the future about the consequences from increasing exposure to Russian commodities, particularly metals such as copper and nickel, for which Russia has production capacity and strategic reserves to keep supplying China with these critical metals in the future.

China is also less likely to get tangled up in the ESG Paradigm Shift and the related issues to their economic projects abroad with a dependence on these vital commodity exports from Russia. This would be an advantage to China’s strategic dilemmas in the future.