When Will the Bear Market End? Macro 101 for Crypto Investors

Are the good times over?

A record influx of people flooded the financial markets during the pandemic — many first-time investors.

Propelled by…

- The availability of user-friendly trading apps;

- Crypto and stock prices surging;

- Enthusiastic finfluencers all too eager to fan the FOMO; and

- Downright boredom being stuck at home during lockdowns…

…newbies poured their hard-earned dollars into bitcoin, altcoins, memecoins, NFTs and web3 gaming.

The fun times were short-lived.

By early 2022, it became evident that the decade-long secular bull market that began in 2013 had come to an end.

Inflation worldwide exploded on the back of unprecedented stimulus in response to COVID-19, compounded by an economic and kinetic war that raged in Europe.

Central banks — spearheaded by the US Federal Reserve — began hiking interest rates and withdrawing liquidity in an effort to numb the effects of spiralling commodity prices and runaway inflation.

Risk-on assets like technology stocks plummeted.

The $3 trillion crypto market followed suit, exacerbated by a cascade of black swan events that inflicted ruin on bourgeoning blockchains (Terra), major CeFi and DeFi platforms (Celsius and Anchor), prominent venture capital firms (Three Arrows Capital) and leading exchanges (FTX).

2022 was a soul-crushing year. What’s ahead?

“Everyone is a genius in a bull market.”

— Warren Buffett

As we usher in a potentially multi-year secular bear market, the emotional and inexperienced have largely capitulated — often with their life savings parted from them.

Crypto investors determined to ride the next cycle find themselves needing to up-skill in areas that traditionally make smart money, well, smart:

- Discipline, patience and sound risk management;

- Strategic long-term decision-making;

- Understanding of business cycles and macroeconomics.

That’s why I penned this article.

My goal is to convert crypto investors into macro investors, so that they’ll become even better crypto investors.

Let’s dive in.

New to Medium? Join here and gain unlimited access to the best articles on the internet.

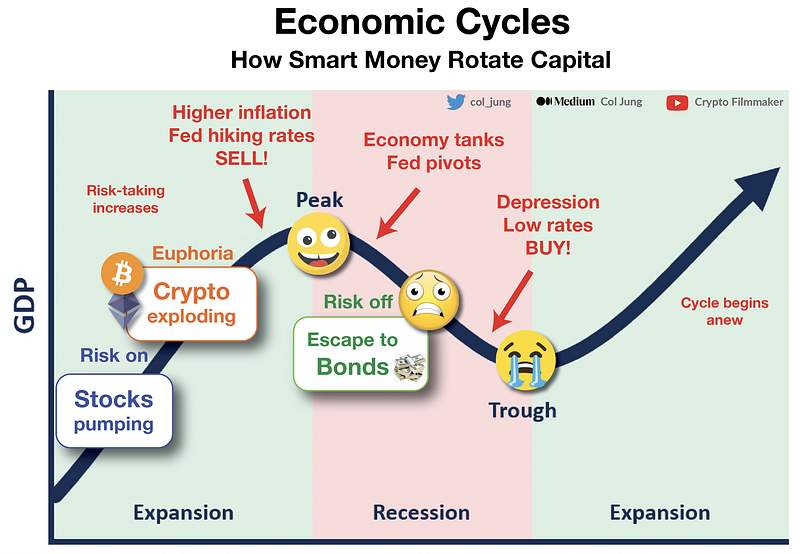

1. Good Times: Cheap & Plentiful Money

Your asset prices are ultimately at the mercy of economic cycles.

These are characterised by cycles of boom and bust.

If you’re new to economics, I’d suggest this brilliant video by Ray Dalio.

During good times, the economy expands, buoyed by cheap credit thanks to central banks keeping interest rates low. [Note: The US central bank is called the Federal Reserve, who sets the federal funds rate.]

Businesses borrow cheap money to grow, hire more employees and generate profits, which leads to more disposable income and spending throughout the economy.

This leads to more profits for businesses, more growth, more borrowing — it all continues in a virtuous cycle.

Financial markets are exuberant!

A secular bull market — the most recent of which started around 2012 — is in full swing.

Higher profitability jack up the prices of risk-on assets like equities (i.e. stocks) and cryptocurrencies.

In addition to conventional monetary policies like pulling the lever on interest rates, the US Fed can also engage in unconventional monetary policies like Quantitative Easing (QE), which for all purposes is akin to printing more money.

You’ll see this reported in the media as the expansion of the Fed’s balance sheet.

This excess money (i.e. liquidity) flows into the stock market, but especially into higher-risk assets like low-to-medium cap growth stocks and crypto.

During the pandemic, the world witnessed a new generation of newbie investors — lured by FOMO, the Fear of Missing Out— dive into these assets en masse with their savings and wages.

The smart ones exited in November 2021. Many — arguably most — did not.

2. Anxious Times: Inflation & Rate Hikes

Ideally, the economy should experience continuous expansion, yet the proliferation of borrowing and credit, a long-standing pillar of our society since the advent of banks, starts to drive higher inflation.

Demand for goods and services outstrips supply.

Things get expensive quicker.

The economy starts to overheat.

What do…?

Central banks worldwide take actions that unsettle risk-on investors, including raising interest rates (conventional monetary policy) and reduction of their balance sheet (reversing an unconventional measure).

Let’s first address rate hikes.

From now on, we’ll focus on the US markets considering their oversized contribution on global financial markets.

The US Fed steps in and starts rising the federal funds rate, which increases the cost of taking on debt.

This blunt instrument cools demand, which aids the Fed’s primary aim of achieving price stability — the idea that the price of stuff shouldn’t get expensive too quickly.

That is, avoid high inflation.

[Note: during a deleveraging in a secular bear market, price stability means prices shouldn’t get less expensive too quickly either, i.e. high deflation.]

Okay, great! Hiking rates addresses high inflation, so what’s the problem?

When the Fed hikes rates too fast and too high, it cripples businesses and hurts the the broader economy — increasing the cost of living, borrowing money and servicing mortgages.

This can trigger a new contraction phase in the economic cycle, ushering in a prolonged period of a secular bear market, similar to the lasting years we witnessed during the dot-com bust of the 2000s.

During these bad times, the economy contracts, businesses generate less profits — some making losses — which leads to downsizing, employee layoffs and bankruptcies. This means less disposable income, which leads to less consumer spending, which leads to even lower business profits, thus continuing a vicious cycle.

This is what we’re seeing throughout 2022 and 2023.

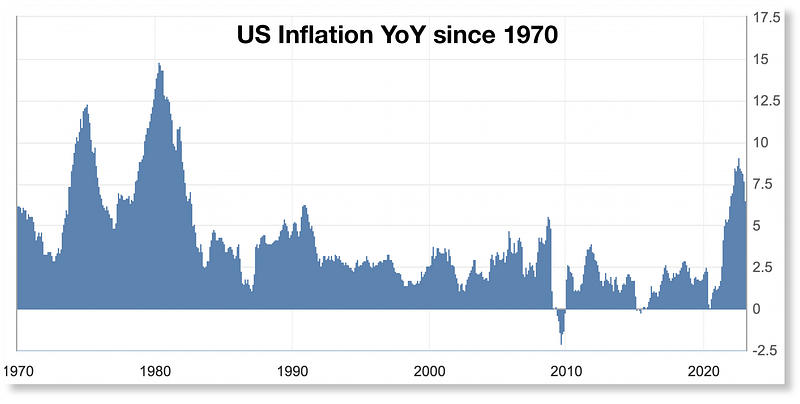

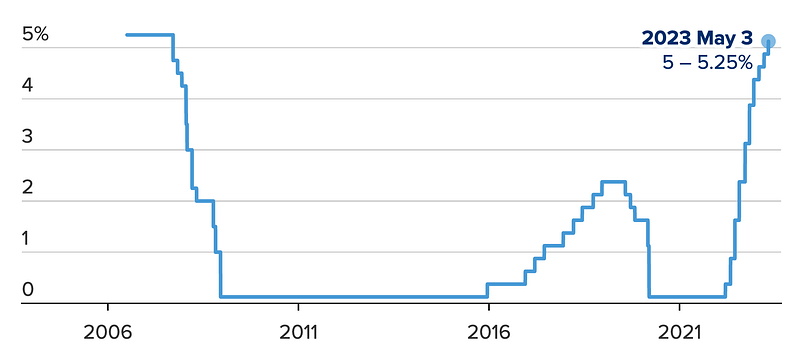

Ominous inflation numbers, whether you were looking at the Consumer Price Index (CPI) or Personal Consumption Expenditures (PCE), forced US Fed Chairman Jerome “Papa” Powell to begin aggressively hiking interest rates in America in March 2022.

This wasn’t just an issue limited to the US.

By the first quarter of 2022, average annual inflation rates had doubled or more compared to their pre-pandemic levels in 37 out of 44 developed nations within the OECD.

Inflation was simmering globally, but the unexpected invasion of Ukraine, along with its impact on commodity prices — a vital driver of inflation — transformed an arguably transitory inflation issue into a problem that demanded central banks change their tunes with urgency.

By Q2 2022, dovish Powell was dead.

Throughout the past century, there have been only two notable periods of significant inflation comparable to the severity witnessed today. The first transpired during the tumultuous WWII era of the 1940s, while the second unfolded in the 1970s, leading the then-Fed Chairman Paul Volcker to inflicting unprecedented rate hikes of almost 20%!

Powell, evidently wary of history’s rhyming patterns, has repeatedly warned investors:

“We will keep at it until we are confident the job [of achieving price stability] is done.”

Like clockwork, investors in 2022 avidly focused on the outcomes of the US Fed FOMC meetings, held at regular intervals of 1 or 2 months — nervously anticipating the decision on whether another rate hike was in store.

And indeed it was, every time, without fail.

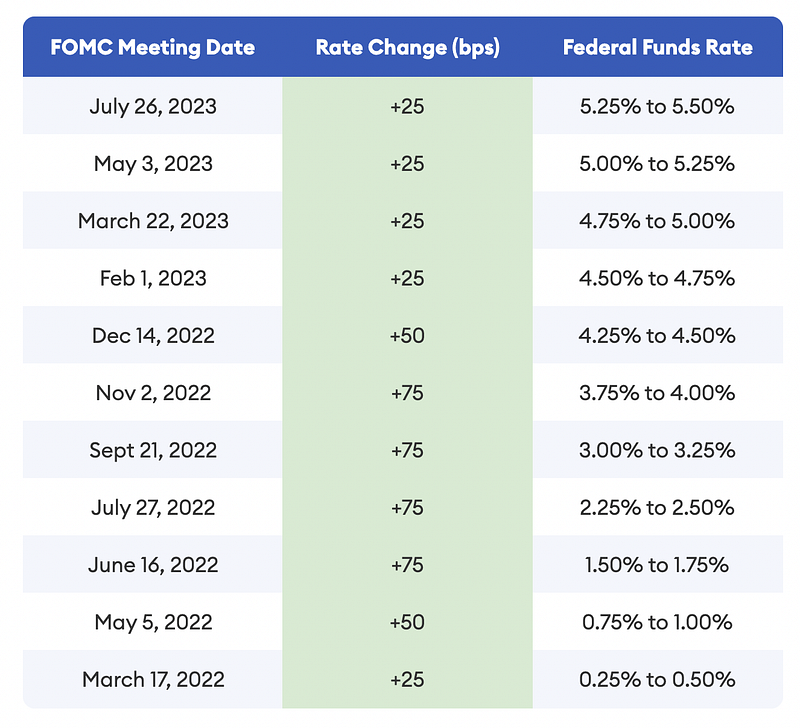

Since March 2022, Powell announced rate hikes in a perfect 10 out of 10 meetings — from 0.25% to a whopping 5.25% over 15 months.

The question becomes, as an investor, how do you get ahead of these announcements in time so that you can best position yourself?

Tip #1 — Dive into Drivers of Inflation

Let’s start with a few tips focusing on getting ahead of the inflation numbers.

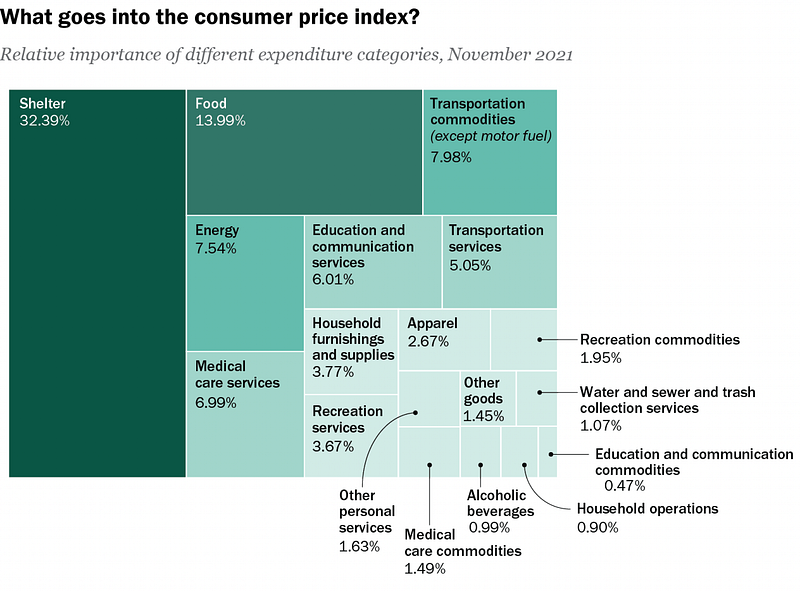

First, learn to read into the drivers of inflation.

Savvy investors will eagerly delve into the regular reports from the US Bureau of Labor Statistics, meticulously scrutinising the data to discern the key sectors of the economy and specific expenses that drive the CPI & PCE, which equips them with valuable insights for informed decision-making during subsequent FOMC meetings.

[Note: the Fed puts more focus on the PCE, the index that includes a broader range of goods and services than the basket defined in the CPI.]

For instance, a high PCE driven by high oil and gas prices is actionable information, as it’ll prompt you towards the direction of researching what’s going on in those markets. As it turns out, Western governments have been employing a strategy of letting Russian oil freely flow but suppressing their prices in an effort to starve the Russian war effort. What will that mean for oil prices in the next quarter, and hence the metrics feeding into the CPI and PCE?

That leads to my second tip of focusing on the charts that matter.

Tip #2 — Focus on the Right Charts

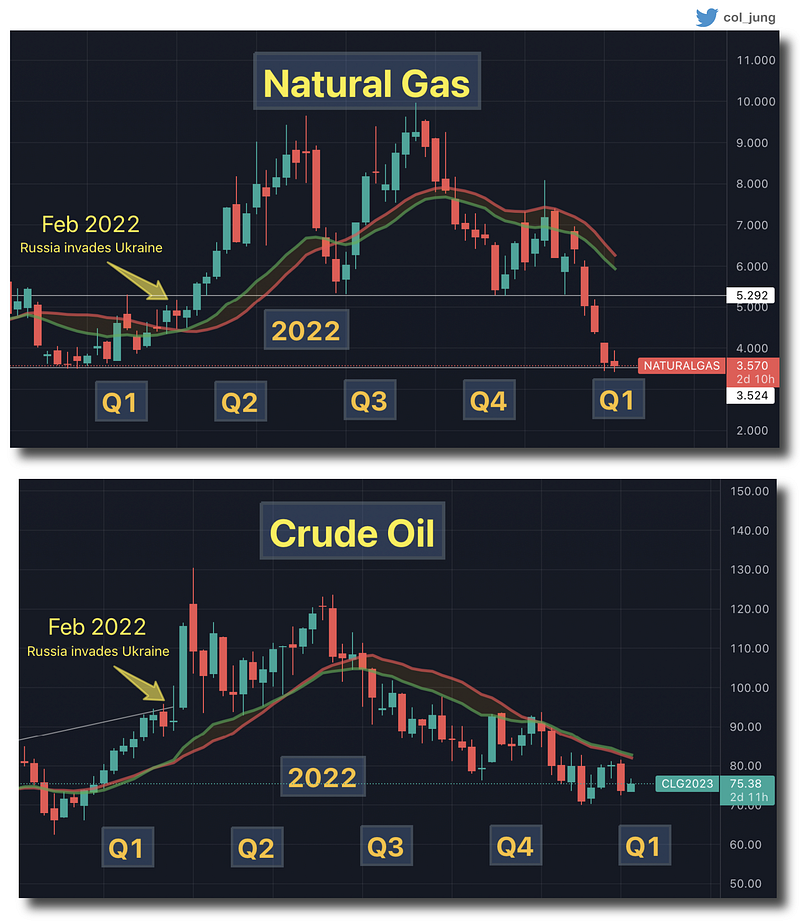

The bad inflation numbers were exacerbated by lingering supply chain issues from the pandemic and spiralling commodity prices from the raging war in Europe.

This is why the savviest crypto traders in 2022 were keeping a closer eye on commodity prices like natural gas and crude oil than BTC or ETH.

The higher these commodity prices, the higher the inflation numbers, the more likely the US Fed will keep jacking up rates that’ll continue to inflict pain on bruised investors.

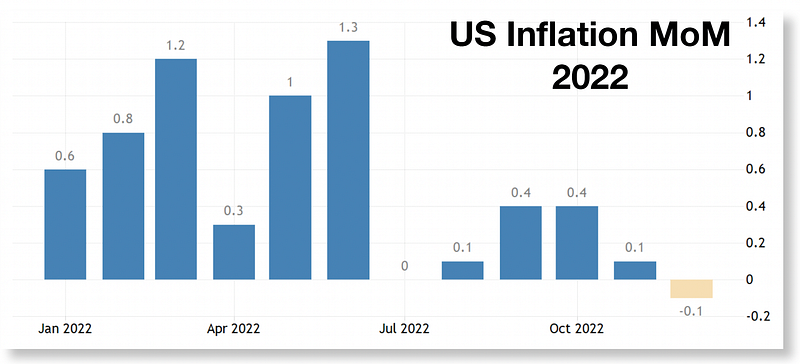

Tip #3 — Discerning YoY vs MoM Inflation

Next, think critically about the numbers.

Inflation — both CPI or PCE — is typically measured as either year-on-year (YoY) or month-on-month (MoM). Savvy investors recognise that the latter, with its shorter time frame, provides a more granular and accurate view of whether inflation is getting under control or not.

For instance, the low MoM inflation figures across 2022 H2 and the deflation of 0.1% over the month of December was a major driver of the stock market rallying in Q4 2022.

This is because projecting forward the inflation results from July 2022 onwards for a full year would have led to ~2%, which happens to exactly be the magic target the US Fed is aiming for!

Something that would help Papa Powell and his army of investor groupies sleep well at night.

Let’s now delve into a couple of tips for peering into the market’s crystal ball and anticipating what’s expected for upcoming FOMC meetings.

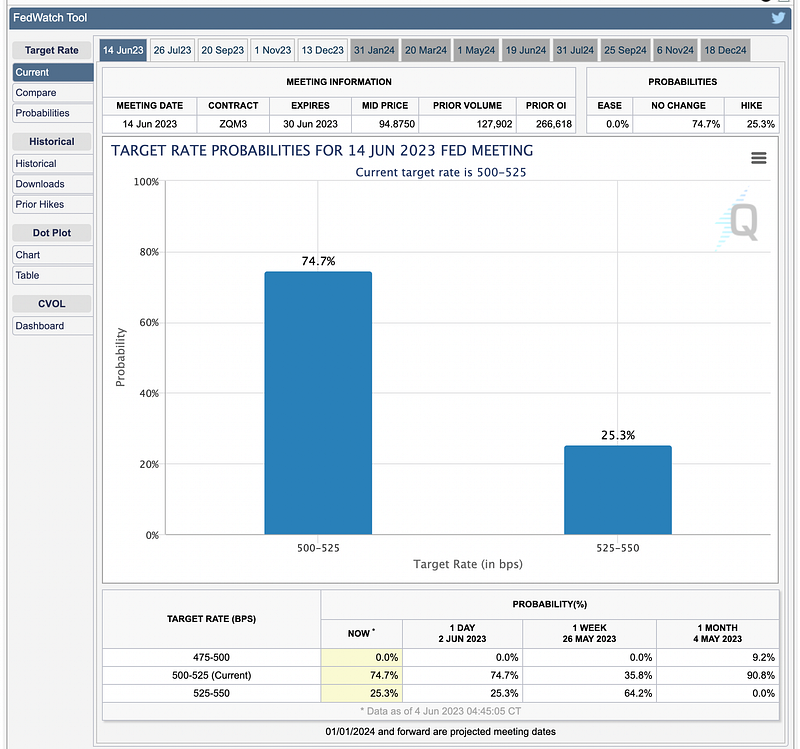

Tip #4 — US Fed Funds Futures

Use the 30-day US Fed Fund Futures to see what rate hikes are being priced into the markets.

This chart acts as a window into the collective expectations and wagers placed by market analysts, providing valuable insights into anticipated monetary policy moves.

As an example, at the time of writing, with the funds rate standing at 5.25%, the Funds Futures market predicts a significant probability (75%) of a pause in rate hikes at the next FOMC meeting. (A quarter of analysts still anticipate another 25 basis points hike, raising the rate to a formidable 5.50%.)

After each FOMC meeting, stock and crypto prices can jump or dive depending on whether these anticipated fund rate changes become reality.

Tip #5 — Bond Markets

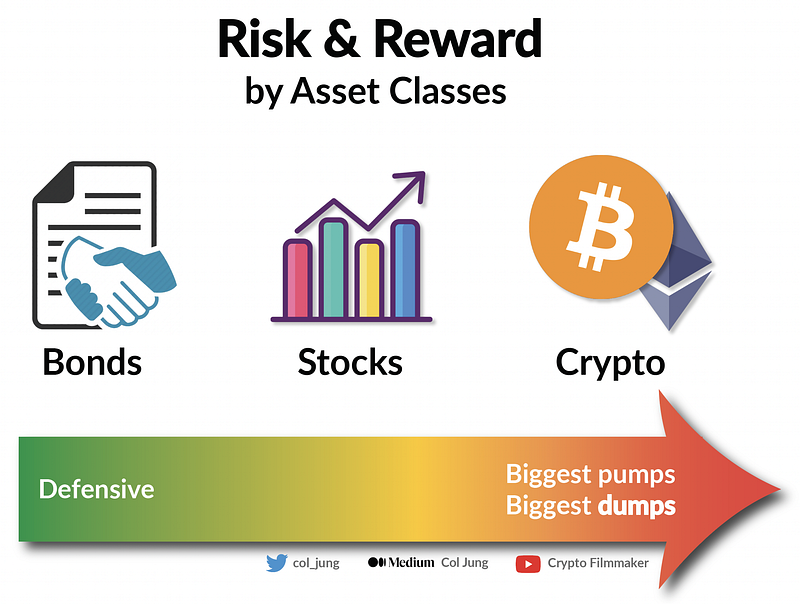

Another way to glimpse into the future is to understand bonds.

Bonds are known as fixed-income investments.

When you invest in bonds, you are essentially lending money to governments or purchasing their debt. In return, you receive a relatively modest yield and a commitment to repay the principal amount at a specific maturity date. It can be viewed as an IOU backed by the financial stability and creditworthiness of the issuing country.

Short-term bonds have a maturity length of just a month, while longer bonds can span 30 to 50 years.

Bonds are highly-defensive assets often favoured by smart money: hedge funds, institutions, portfolio managers and retirements funds, who prioritise certainty, safety and risk management over returns.

Bonds offer a reliable income stream, capital preservation, and act as a hedge against volatility in other asset classes, making them a preferred choice for investors seeking stability and long-term wealth preservation.

The US bond market is also the world’s biggest and most liquid market.

This makes bonds, particularly US government debt, a safe-haven destination during bear markets when the sentiment is risk-off. During such periods, when equities and crypto are dumping, bonds provide a relatively stable and predictable return tied to the central bank funds rate.

In bull markets, bonds typically offer relatively modest yields, often around 1% per year. Such low returns make them completely unattractive to the degen investors (cough, gamblers) in the fast-paced world of cryptocurrencies, who are accustomed to their altcoins doubling or halving in value within a day.

Bonds are the antithesis of crypto — the latter attracting largely emotional retail investors who trade on sentiment over fundamentals and lack experience in managing large-scale portfolios and proper risk management.

Alright…where am I going with this?

Here’s where it matters to you:

The defensive, risk-averse and institutional nature of bond-holders means that the bond market is very efficient for pricing in rate hikes.

Bond yields are the best indicator for what central banks are going to do.

If you want to get an accurate gauge of how smart money feels about the trajectory of the US Fed, look at short-term US bond yields like the US 1 Month Treasury. For instance, below, the bond markets — overseen by influential portfolio managers responsible for trillions of dollars — are predicting the Fed fund rates to remain unchanged at 5.25% in June 2023.

An assessment they would have no doubt performed with great due diligence.

Tip #6 —Strength of the Dollar

We know that interest rates positively correlate with bond yields.

Another correlation relates to the US Dollar Index (DXY), which measures the strength of the US dollar against a basket of other major currencies.

In short, the DXY increase and decrease alongside rate hikes.

This is because rate hikes in response to a strong economy leads to increased demand for US dollar-denominated assets while signalling confidence in the US dollar. Meanwhile, hikes during uncertain times increase the attraction of USD as a safe-haven assets.

Either way, the DXY rolls along with the funds rate.

Furthermore, we know that rate hikes are detrimental to the prices of risk-on assets, which is why we see the famous inverse relationship between the DXY and BTC.

Many crypto investors keep a close eye on the ‘Dixie’ in order to anticipate where the market is going next.

Enjoying this story? Get an email when I post similar articles.

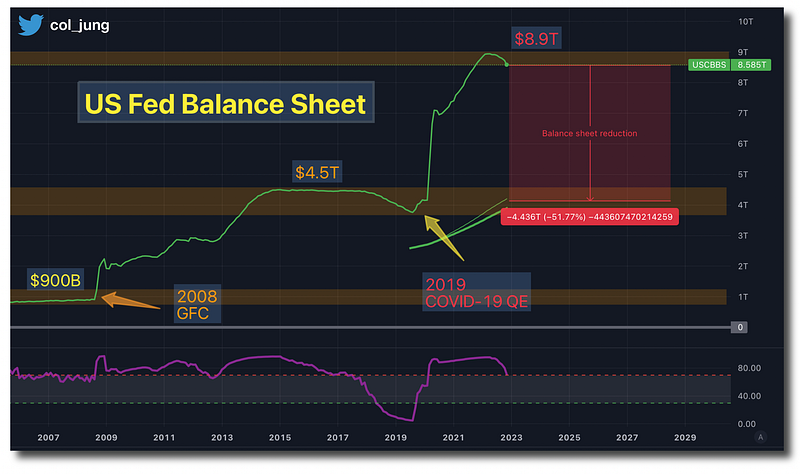

3. Fun’s Over: Fed’s Balance Sheet Reduction

In 2022, alongside rate hikes, the Fed initiated the opposite process of printing money by withdrawing liquidity from the financial markets.

This is known as Quantitative Tightening (QT), often reported as the reduction of the Fed’s balance sheet.

This is notable for a couple of important reasons.

Central banks worldwide printed an unprecedented amount of money in response to the pandemic in order to save their locked-down economies.

In America alone, the US Fed doubled their balance sheet between 2020 to 2022 from $4.5 trillion to almost $9 trillion dollars.

Powell has ordered this money supply be withdrawn at a pace of roughly $100 billion per month, thereby sucking up capital from markets and the broader economy.

This is bad for investors because cryptocurrency is a highly efficient absorber of liquidity, with bitcoin’s valuation (market cap) almost perfectly correlated with level of liquidity swimming around the world.

Crypto needs liquidity and easy money to splash around. That’s the reality.

When central banks pump money into markets, crypto — alongside the growth-oriented sectors of technology and disruptive innovation — emerge as major beneficiaries, amplifying valuations and prices.

When central banks reel in excess liquidity with no end in sight, the ramifications reverberate throughout these markets, leading to prices bleeding and bleeding.

However, one should be nuanced about the data. In the first quarter of 2023, the US Fed continued to reduce their balance sheet while the Bank of Japan — concerned about the Japanese economy — began printing again! Hah. This mixed signal resulted in some positive gains for crypto and growth stocks.

4. When Will the Markets Bottom?

We now arrive towards the climax of the article, which is to answer the all-important question:

When will the markets bottom?

The common sensical answer is when the US Fed pivots from a hawkish regime of raising rates into a dovish regime of lowering rates.

This suggests that the moment the FOMC announces their intention to begin reducing rates (slated for 2024), the bear market should be over.

This is a historical fallacy.

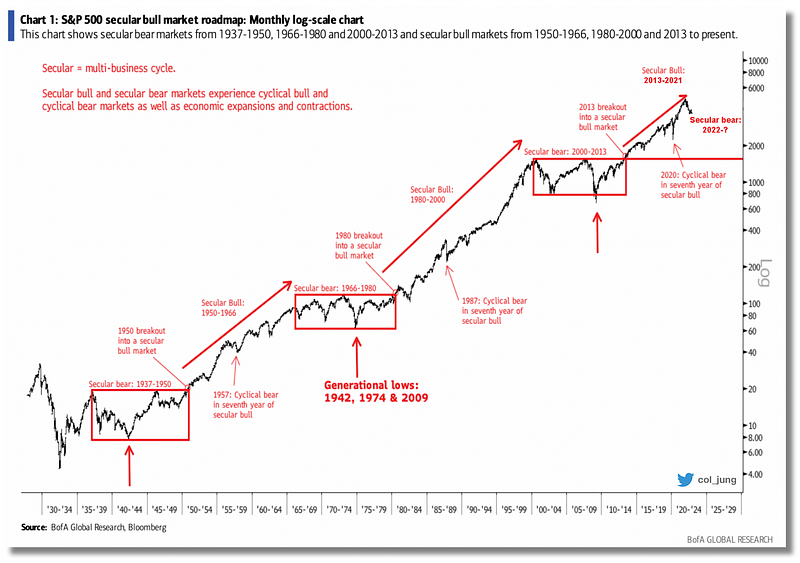

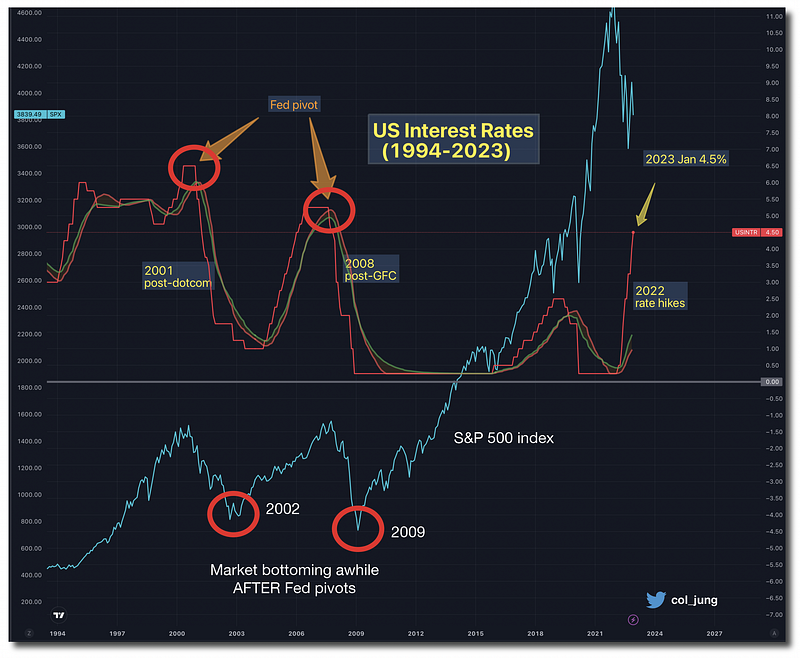

In the past, markets almost always bottom sometime after the US Fed pivots. Usually years after.

As we can see from this chart, during both the 2000 dot-com bubble and 2008 GFC, financial markets tanked further as the US Fed began reducing rates, and actually bottomed when rates had hit their own bottoms — years after the pivot.

The reason why this happens is kind of tragic.

The Fed wants to keep hiking rates…or at least keep them suspended in order to conquer inflation and re-establish price stability.

At some point, the economy buckles and something breaks. Major recession, banking crisis, financial crisis, what have you.

The Fed is forced to either allow such crises to reach systemic proportions, or capitulate on inflation. It often picks the latter and begins slashing rates.

That is, often rate cuts have historically coincided with crisis.

Such a predicament — often accompanied by mass layoffs, economic recession and even violence — further dumps the already cratered markets, until the US Fed fully capitulates on its goal of defeating inflation and backtracks in order to stabilise the economy and kickstart a road to recovery.

The lessons here are clear.

Don’t buy assets at the precise time the Fed pivots. You might think that’s when markets begin flying again — but it’s not.

Keep stacking cash like a madman so that you can deploy them after the Fed has reduced rates all the way down, which is historically when markets hit their final low.

Rather than buying when there’s blood on the streets, as articulated by Nathan Rothschild in the 19th century, the optimal time to buy is during the clean-up!

You can bet your sweet horses that smart money will be accumulating assets at heavily discounted prices here, while retail investors — who have either ran out of money buying dips or are pre-occupied with remaining employed and feeding themselves — are largely out of the market.

Let’s now look at a couple of tips to get a grip on where we are in the bear market.

The general idea is you want to use metrics to identify when we’re about to slide into a recession or have something break, so that the US Fed will consider pivoting away from its hawkish monetary policies.

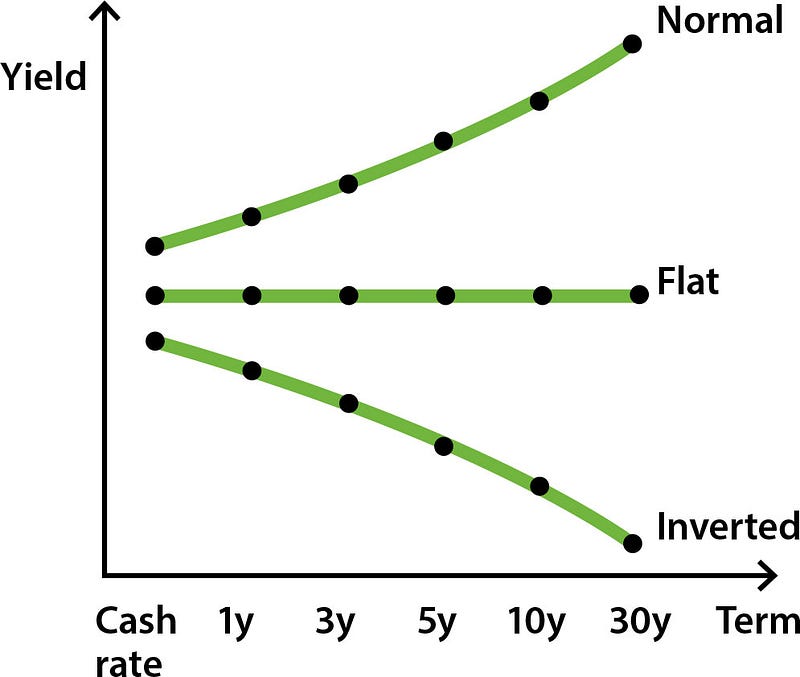

Tip #1 — Bond Yield Curve

One of the most consistent recessionary indicators in history is the bond yield curve. Historically when it inverts, we almost always slide into a recession within 18 months.

Powerful stuff. So what is this curve?

Remember that bonds have different maturities. during normal times, the yields (returns) on shorter bonds (e.g. 2-year Treasury) is lower than yields on longer bonds (e.g. 10-year). This generates an upward-sloping bond yield curve.

As we slide towards the bad times, shorter bonds (less time risk) begin paying higher yields relative to longer ones, resulting in an inverted yield curve.

Here’s the real magic.

We can plot what the curve looks like over time using a Treasury Spread graph. At any point, the curve represents the longer Treasury yield minus the shorter Treasury yield.

This means if the yield curve is normal (upwards) during that year, the spread curve is above 0%. When the yield curve is inverted, the spread curve dives under 0%, represented in red below:

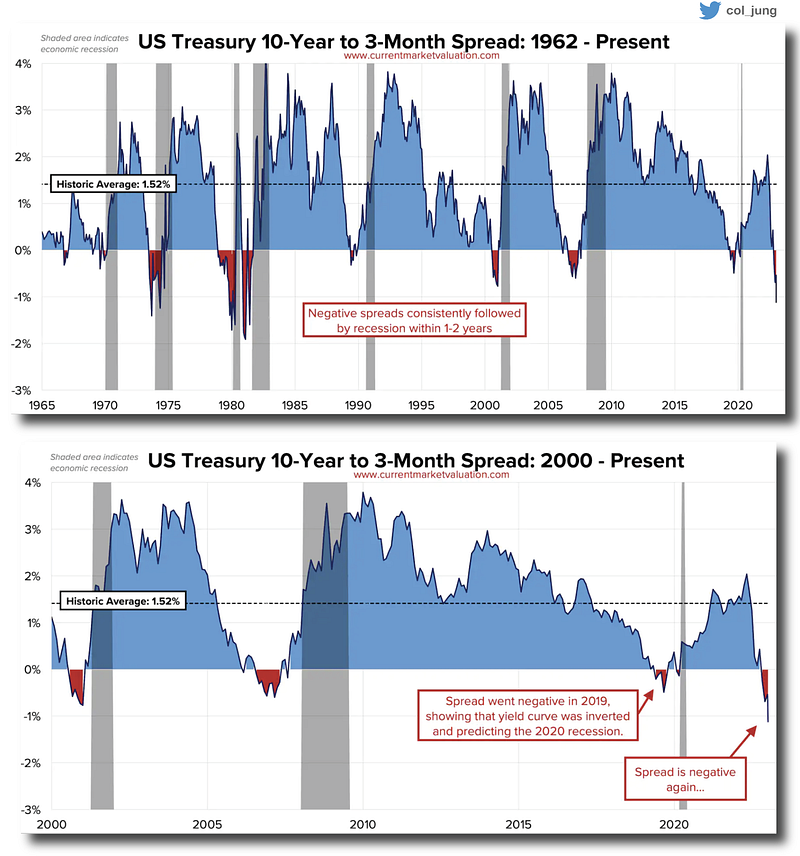

As you can see, we have small pockets of red over the past 65 years, representing times when the yield curve has inverted, followed almost always by a recession, represented by shaded grey.

Right now, the 10-year to 3-month spread is very negative, because the 10-year to 3-month yield curve is heavily inverted.

This lends evidence to the suggestion a recession is coming.

You can make your own Treasury Spread charts in TradingView too. Here’s mine for the past 30 years, where I’ve overlaid the S&P 500 index to highlight a very important observation:

Markets tend to bottom a couple of years after the bond yield spreads begin recovering.

Tip #2 — Economic Data

Put it simply, you’re looking for data pointing to signs of a…

- Strong economy, which means inflation and more hikes; or

- Stressed economy, which means recession fears and possible Fed pivot.

What are some of these data points?

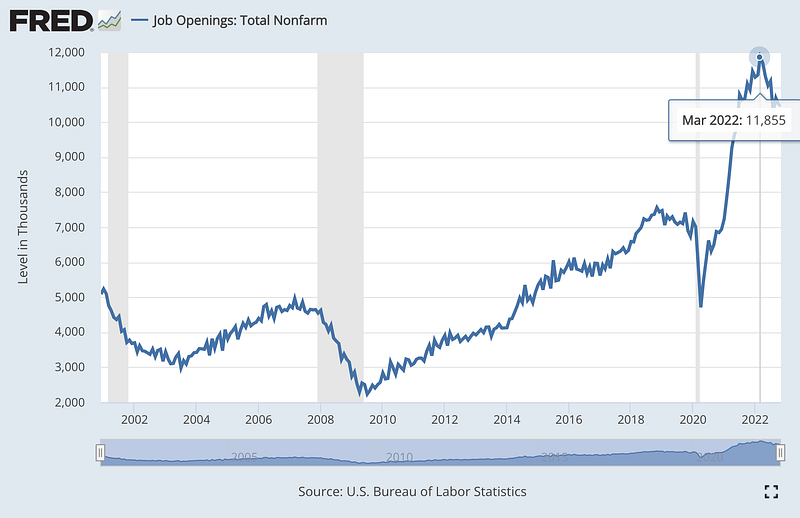

Jobs

During a strong economy, low unemployment rates fuel competition for workers and therefore fast-rising wages. This creates high labour cost for businesses and puts upward pressure on their service costs. Hence, inflation, and more rate hikes, or higher rates for longer.

We saw this throughout 2022. Unemployment remained stubbornly low, as we can see here with the number of job openings reaching record highs:

Job figures matter for another important reason: it’s part of the US Fed’s mission.

The US Federal Reserve has a dual-mission of ensuring:

- price stability;

- full employment.

And its magic powers is controlling the supply of money in order to achieve those aims.

In a stressed economy, where businesses are having a hard time and workers are laid off, the US Fed often has to pick two poisons: either it capitulates on inflation or puts a lot of people out of work.

When it gets bad enough and something breaks, the Fed will pivot.

So keep an eye on those job numbers.

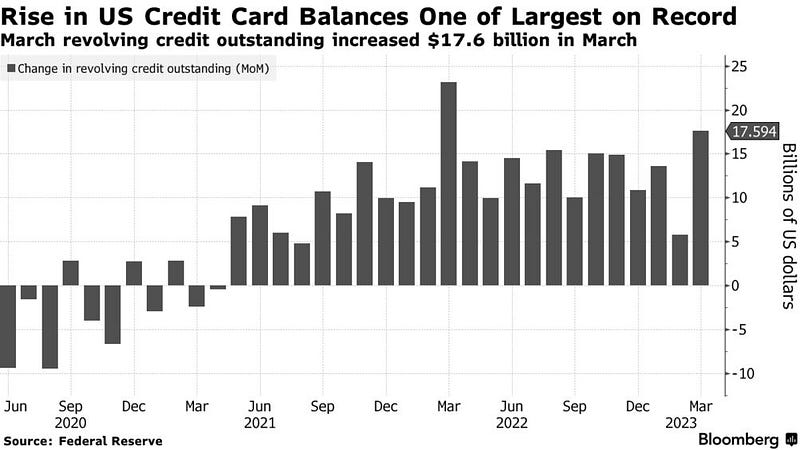

Consumer Credit

The story here is straight-forward: as inflation starts to bite, people begin maxing out their credit cards just to buy essential goods and services, such as food to eat and paying for shelter.

This is made worse by increasing job insecurity and worker layoffs, forcing stressful debt-taking just to get by.

Since 2022, US consumers were borrowing a combined extra $10–15 billion dollars on their credit cards each month.

Consumer credit is a data point investors and economists watch to see how close we are to a recession.

Earnings

Next are earnings reports by major companies within the:

- S&P 500 — 500 largest public companies in the US;

- NASDAQ — home of the large growth and tech stocks;

- Dow Jones — 30 large, stable public companies across various industries.

When inflation bites and the economy begins to suffer, this trickles into poorer earnings, which:

- dumps stock prices (and often crypto prices);

- takes us closer to a recession.

As a result, investors and economists pay close attention to earnings season, which typically occurs four times a year at the end of each quarter, with the numbers serving as a measurement of economic performance

Real Estate

The price of shelter affects investors in two major ways:

- It plays a significant role in key inflation measures (CPI/PCE), which informs US Fed policies;

- It gives information about the state of the economy and the balance sheet, which again informs US Fed policies.

When rates are hiking, yet the real estate market remains robust, it means there is still significant demand in the economy and plenty of cash being splashed around, which simply tells the US Fed that the “job isn’t done” and that the hikes and balance sheet reductions need to continue.

Tip #3— Black Swan Events

Yes yes, we all know that the cryptoverse suffered a cascade of black swan events in 2022, but the $3 trillion (at its highest) crypto market is ultimately a drop in the water compared to the $50+ trillion global equities market and $400+ trillion real estate market.

Besides, the government and central banks don’t really care about us. If anything, they’ve been working hard to regulate us and make life difficult.

I’m referring to black swan events in the broader economy and traditional financial sector.

In 2023, we slipped close towards two major black swan events.

First, a potential banking crisis as major banks began failing, starting with Silicon Valley Bank in March, followed quickly by Signature Bank. Analysts, economists and the government are rattled by the suggestion that half of banks are — on paper — underwater. This would result in a full-on crisis if everyone decided to go on a bank run.

Second, a potential debt ceiling crisis in May 2023, which Goldman Sachs economists estimated would immediately halt roughly 1/10th of US economic activity had the ceiling been breached. Think tank Third Way warned that a default would have cause the loss of three million jobs and add $130,000 to the cost of an average 30-year mortgage. Treasury Secretary and former US Fed Chair Janet Yellen even wrote to Congress warning that:

“Failure to meet the government’s obligations would cause irreparable harm to the U.S. economy, the livelihoods of all Americans and global financial stability.”

Either of these black swan events materialising would have sought economic turmoil and created havoc in the markets, likely necessitating US Fed involvement — potentially a sharp pivot.

5. Final Words

This article is dedicated to help crypto investors who only know crypto survive their first bear market.

Until recently, we were riding the wave of an epic and euphoric bull market, like surfers on a wave of cheap and easy money that seemed to never break. After injecting trillions into the economy, effectively doubling the money supply in a couple of short years, the markets were swimming in a sea of cash.

Just an unbelievable level of liquidity, really.

Times are different now.

The decade-long secular bull market is no more.

Expanding beyond the crypto bubble and having a good understanding of how macro narratives feed into the tiny crypto market is critical to best position yourself for the next bull market.

A cloud of uncertainty hovers over the bitcoin and wider crypto market as it has yet to experience a market cycle bull market (driven by the 4-year halving cycles) without NASDAQ support.

To put it simply, the entire lifespan of the crypto market has unfolded within the cozy embrace of accommodating monetary policies, with each of Bitcoin’s halving-driven bull markets occurring within the broader secular bull market of recent times.

Yep, that’s kind of scary for crypto investors.

Will there be a BTC bull market after the 2024 halving, even during a deep recession?

C’mon…

We’re at the end of an economic cycle. Liquidity is drying up.

The Fed is squeezing off the tap. Don’t fight the Fed.

Yes, they have a history of appeasing markets by kicking the inflation can down the road with premature rate cuts and a resumption of money printing, but Powell has signalled over and over again that this time is different.

Why?

The man is terrified of a 1970’s Volcker-era scenario that took years and a 19% federal funds rate to finally bury the problem.

Like a clingy ex, inflation is sticky and stubborn.

A regime of stop-start easing of monetary policies when the job is not done merely beckons inflation’s return down the road. No one want that, least of all Powell.

Thus don’t hold high expectations for the foreseeable future.

Persistent inflation, high rates and the steady reduction of central bank balance sheets will cripple some parts of the economy. Do you think people are going to be chasing to buy bitcoin when they have little disposable income and are struggling to feed themselves and make their mortgage repayments?

The dream of BTC prices decoupling from the stock market is — at least for now — still a dream, which means crypto’s fortunes are still tied to that of basic macro-economics.

Staying in one’s cozy crypto bubble may be tempting, but not if you want to stay poor.

Follow me on Twitter & YouTube for regular analyses and guides.

My Crypto Articles

Unlock unlimited access to Medium by joining here.

- When Will the Bear Market End? Macro 101 for Crypto Investors

- A Review of the Cryptocurrency Market in 2022

- Web3 Gaming — What do Crypto, NFTs & Metaverse offer?

- FTX’s Collapse & Solana’s Long-term Impact

- Polygon & Solana — 6 Killer Crypto/NFT Use Cases

- A Brief History of NFT Marketplaces

- Compound Interest is the 7th Wonder of the World

- How to Generate Passive Income with Crypto

- Crypto Passive Income on BNB Chain

- Move & Earn Crypto — 6 Month Review of STEPN

- PancakeSwap’s High APY Pools — What’s the Catch?

- Cardano, Avalanche, Solana Staking Guides (2022)

- Cardano, Avalanche, Solana Price Predictions (Bull Market)

- How to Make Crypto Price Predictions

- Top 3 Price Prediction Mistakes

- Crypto VISA Cards — Cashbacks for Every Purchase?

- How to Build Wealth like Smart Money

- Is Crypto.com’s Earn Program Worth It?

- Understanding Terra’s Anchor Protocol

- How to Participate in Initial DEX Offerings

- Memecoin Speculation — Is It Worth It?

- Why SHIB Can Never Reach $1 (or even close)

- Want to Retire Early? Buy Bitcoin

- Democrats vs Republicans — Which Party Better for Markets?

Crypto Sign Up Bonuses

- Binance — 5% off fees forever (link)

- Nexo — $25 free BTC with $100 deposit (link)

- Crypto.com — $25 free CRO with a Jade Green VISA Card (link)

Subscribe to DDIntel Here.

Visit our website here: https://www.datadriveninvestor.com

Join our network here: https://datadriveninvestor.com/collaborate