How to Become an Anti-Fragile Investor and Always Profit

The Best Strategy for the Market Recession Is Surprising…

After reading this article, you will know exactly what to do if there’s a market crash.

Here’s your guide to becoming an anti-fragile investor — who not only survives but thrives during market volatility.

Once you’ve embraced this approach, you’ll no longer fear market downturns and will possess the confidence needed for long-term, profitable investing.

Market Volatility is Your “Frenemy”

To protect yourself from market volatility, market corrections, and crashes, you need to first understand it:

The market will crash again. It is a fact that we cannot escape from. It’s just part of the game.

Over the last 150 years, the S&P 500 declined by 10% or more on 294 occasions. In 22 out of these 294 occasions, stocks dropped 25% or more, meaning that major bear market crashes occur every 6.8 years on average.

If we look at the Nasdaq-100 (an index for tech companies), it’s even worse: Nasdaq has dropped 10% or more 192 times since 1985 alone. It happens literally every year.

Market corrections can be scary, but that’s largely because we humans are wired to weigh losses more heavily than we weigh gains. It’s worth noting that, despite all the daunting dips, since 1985, the S&P 500 has returned 2,800%, and the Nasdaq has yielded an astounding 14,600%.

Given these statistics, it’s reasonable to expect another “scary” market correction in the near future. Acceptance is key.

As previously mentioned in this article, embracing market volatility is crucial. Remember, volatility is the price you pay for performance.

Now, let’s get you prepared. 😎

The Anatomy of a Correction and How to Prepare

Preparing for a market downturn is very different from preparing for a natural disaster. Humans have survived for thousands of years by being prepared for typhoons, hurricanes, and snowstorms.

In contrast, preparing for a market downturn can be counterintuitive and even counterproductive. History shows that investors have often lost more money trying to predict market corrections than they have in the corrections themselves.

Hedging is a Deadly Sin

The first mistake many investors make is attempting to hedge their portfolios. They buy “insurance” against market corrections by dabbling in VIX, futures, options, and short positions, hoping to offset potential losses with profits during market declines.

However, this kind of “insurance” comes at a steep price. Many hedge funds underperform or even collapse due to the inherent difficulties in hedging effectively — difficulties that are not spared even for multi-billion dollar funds. Often, hedging results in losses and limits potential gains.

Additionally, effective hedging will require you to time the market, which is an almost impossible mission.

Trying to Sell Before a Crash = A Wild Goose Chase

The second common mistake investors make is trying to time a market correction and sell off assets ahead of it. Fearing that a correction is imminent, skittish investors often sell part of their portfolio of stocks or ETFs and sit on their cash, waiting for the crash.

Their strategy? To scoop up bargains after the market bottoms out. Seems clever, right? Not quite.

The problem is: predicting the timing of a market correction is a gamble. It could happen next month, in half a year, or even two years down the line. All the while, you’re missing out on potential market gains — which, ironically, can be more expensive than enduring the correction itself.

Even if a correction occurs, pinpointing the absolute bottom is nearly impossible. You might keep waiting for even lower prices, convinced the market hasn’t quite hit the bottom yet, only to miss out on the rebound.

Our obsession with trying to outsmart the market often leads us to outsmart ourselves in the end. The fear of losing can be powerful, but sometimes, playing it too safe can be just as risky.

Another thing investors sometimes do is use Stop Losses. You need to understand that where some investors place stop losses, smart investors place buy orders.

I absolutely hate Stop Losses, and here’s why:

Timing the Market — A Losing Game

Consider the COVID crash as a prime example. From February 20, 2020, to March 20, 2020, the Nasdaq plummeted by 29%. Yet, impressively, after March 20, the market surged, recovering 18% within just a week. In merely two months, the market had completely recovered.

Had you been completely unaware of the world events in 2020 — say, metaphorically kidnapped for the year — you might have concluded it was a stellar year for the stock market, which finished 17% higher than where it started.

The optimal strategy for an investor during such turbulent times? Just keep cool and use the opportunity to add more value stocks or ETFs to the portfolio.

History has shown that markets have a tendency to recover, often more quickly than one might expect.

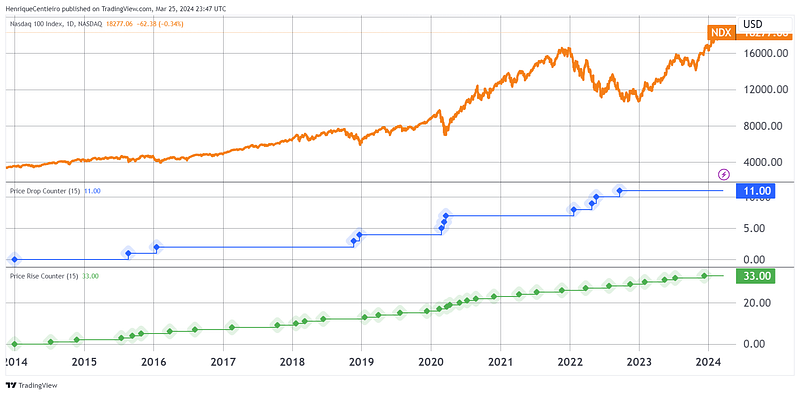

The chart below shows it very well. The blue dots represent corrections of 15% or more, while the green dots represent price rises of 15% or more. As can be clearly seen, green dots always come soon after any blue dots. This means it would be very hard to time a bottom without missing the price surges that always happen after a bottom:

This chart also provides another interesting bit of information: During this 10-year period, the market declined by 15% on 11 occasions, but it rose by 15% on 33 occasions.

Attempting to avoid market corrections or crashes could indeed cost you dearly.

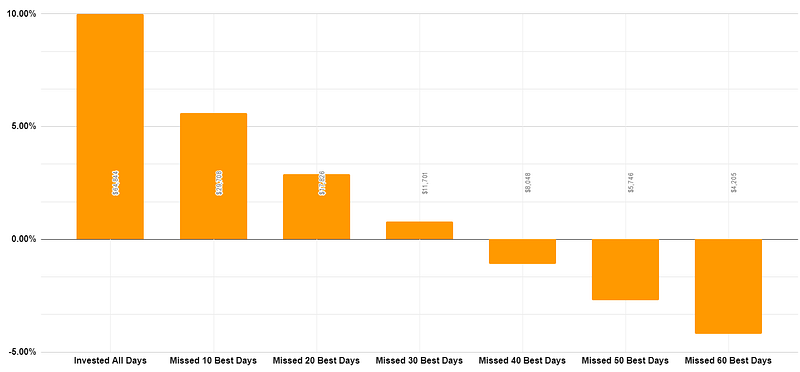

Let’s look at the chart below that shows different scenarios for a $10,000 investment in the S&P 500 from 2003 to 2024. The chart effectively highlights the impact of missing the market’s best days versus remaining fully invested:

By simply missing the 10 best days in the market, you would cut your return by half. These “best days” are critical to compound your capital.

When do these 10 best days occur? Interestingly, they often take place very close to, or immediately after, a market crash.

For example, in 2020, the second-best day of the year occurred right after the worst day of the year.

The strategy to get the best returns is simple, yet, most people won't do it. It’s called “Sit on your ass,” “Shut up and Wait,” or my favorite, “The Sleeping Beauty Strategy” — You just need to learn how to be patient!

In the long run, it doesn’t matter if you are good at timing the market. What matters is that you stay invested for the long term.

The richest stock investors of all time, like Warren Buffett and Charlie Munger, were not stock traders. They were very, very long-term investors who didn’t care much about stock crashes, other than seeing them as opportunities to scoop up some more stocks.

The Zero Bond Strategy — Why Owning Bonds Will Hurt You

I know some people might be asking,

“What about adding bonds to the portfolio? Bonds are less risky and stable, right?”

In the long term, the answer is no. The only time bonds outperformed the stock market was 90 years ago.

While many people prefer to allocate a percentage of their portfolio to bonds, this strategy inevitably results in lower returns.

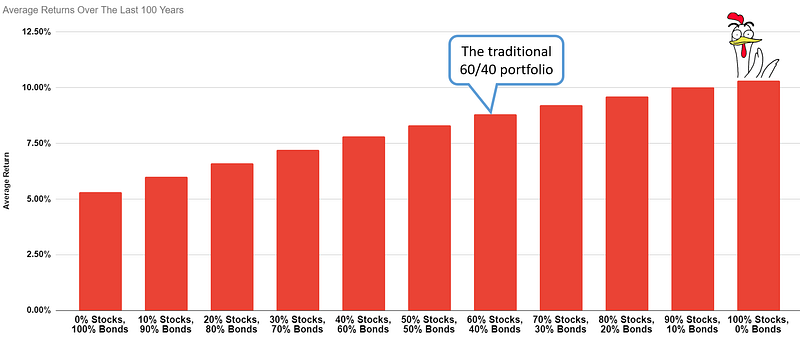

The chart below shows the average returns of a portfolio with different weights between bonds and stocks. A 100% stock portfolio will give investors the best returns:

If we know this, why would anyone add bonds to their portfolio? Why would anyone intentionally lower their portfolio’s return by adhering to the traditional 60/40 stock/bond allocation?

The likely answer is probably that people are too volatility averse, and it’s true that a stock portfolio will indeed be more volatile. But hey, once again, is there any investment in the world that offers good returns without any volatility? The answer is…nope!

Additionally, long-term bonds and even treasury bills meet volatility and losses, especially when interest rates are increased. The chart below shows how the 20-Year Treasury Bond ETF lost 51% from 2020 to 2023:

If you want a steady yield on your investments, dividend stocks are a much better option than bonds. Bonds might pay a “coupon,” but their upside is always limited to their “face value.” On the other hand, dividend stocks pay dividends, and their upside is uncapped.

Holding bonds can also be seen as a form of hedging, which is a good way to lower one's returns.

5 Strategies to Become an Anti-Fragile Investor

If I have to reduce these 5 strategies to just one, I would say that the best way to deal with a correction or a crash is to DO NOTHING!

- Focus on long-term profitability rather than trying to predict or react to short-term market moves.

- Embrace volatility as a stoic investor would. Historical data show that, although regular market corrections occur, long-term gains outweigh the drops.

- Buy stocks in value companies and add to your holdings whenever the prices are low. This article explains how to do this.

- Buy Index ETFs. They have lower fees and perform better in the long term. You can consider adding leverage ETFs to the mix as well.

- Make sure you place your bets in the right country. Given the dominance of USD, the best bet is still US stocks and ETFs.

These 5 simple strategies can help you become an anti-fragile investor.

Conclusion

Embracing market volatility is the key to long-term investment success. If you are afraid of volatility, market corrections, and crashes, you will simply miss the returns.

The market is like a marriage: you need to be there for both the good and bad times in order to make it work.

The winning formula is simple: stay invested, load up on value stocks and index ETFs, and kick bonds to the curb. Historical data proves that a 100% stock portfolio is the way to go.

So, forget about playing it safe. Embrace the volatility, and watch your wealth soar.

Follow these 5 strategies, and you’ll become an anti-fragile investor who laughs in the face of market mayhem. Don’t be a wimp — be a winner!

If you found any value in this article, throw me some Medium love!

🥰 To support my work: Clap up to 50, leave a message to share your thoughts & be sure to follow. 💌

🌞 Stay in touch: