A Complete Guide to the Power of Leveraged ETFs — Debunking Myths and Backed by Data

You Can Outperform the S&P 500 by 10X with This Simple Investment Strategy!

If you’re looking for a passive way to build extreme wealth, your search ends here. This investment strategy isn’t just a wealth enhancer; it’s a true fortune builder.

We all seek the same goal with our investments:

To maximize returns over time, minimize losses, and achieve this as passively as possible. Imagine high, steady returns without the need for constant hands-on management.

However, achieving both low risk and high return is rarely possible; many promises of this nature are, unfortunately, scams.

Yet, I’m about to share with you a passive investing strategy that aims to outperform 99% of other investments while still keeping risk at a manageable level.

Let’s explore how this investment strategy could potentially boost your profits by 10X compared to the S&P 500, all while mitigating long-term risks.

We’ll analyze a distinctive type of ETF — a subject of my extensive research.

A Brief Backrgound on ETFs

If you’ve been following my work, you know that I’m a big fan of diversifying investments across cryptocurrencies, the stock market, and exchange-traded funds (ETFs).

Among these 3 options, only one offers you a passive approach: ETFs. Most ETFs are designed for long-term ‘buy and hold’ strategies — they are excellent vehicles for building financial freedom and potentially retiring early.

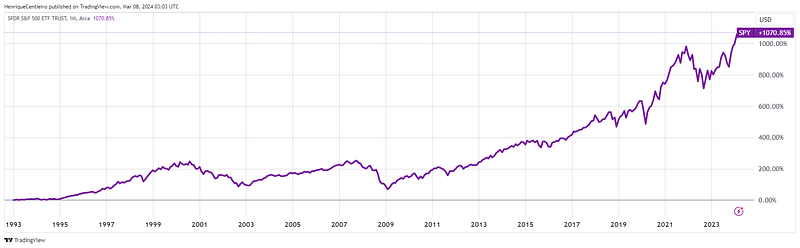

For example, the SPY ETF aims to mirror the performance of the S&P 500 index — comprising the 500 largest companies in the US. Since its inception in 1993, the SPY has yielded returns close to 11X the initial investment:

Sounds interesting to you?

Sit tight because I’m about to show you how you can MULTIPLY those returns.

Introducing Leveraged ETFs

I have spent years reading, studying, backtesting, and investing in leveraged ETFs. Therefore, I strongly recommend paying close attention to the entire article.

Usually, leverage means borrowing money to buy something.

Most people use leverage when they buy a house:

If you buy a $500k house, you put a $100k downpayment and borrow $400k from the bank.

In this scenario, you will leverage your investment by a factor of 4:1. This means that the bank will provide you with $400k while you will contribute $100k. You will have a $500k investment in the property market, giving you 5 times the exposure to the market with your initial $100k investment.

Isn’t it interesting to see that most people are comfortable using leverage to buy property, yet they are often too risk-averse to apply the same principle to investing in the stock market?

This doesn’t even make sense.

In a nutshell, leverage is an amplifier for your money. It will amplify both your profit and losses, bringing amazing returns or not-so-amazing losses.

By the way, please read this article where I explain that leverage is not a bad thing:

How Leveraged ETFs Work

Leveraged ETFs —Lever Without Loans

Unlike other forms of leveraged trading accounts, with leveraged ETFs, you don’t need to borrow money. Instead, these ETFs have “implicit leverage.”

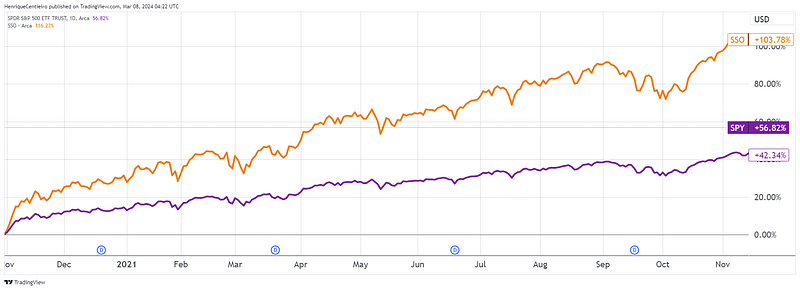

SSO, for example, is 2x the S&P 500 and automatically gives you 2x leverage. This type of leverage is also cheaper than borrowing money or having a margin account with your broker.

The “implicit leverage” of leveraged ETFs is great compared to using margin accounts because the fees/interest are much lower, and there’s no need for rebalancing your investments, i.e., the ETF will rebalance automatically every day to keep the margin at 2x.

Leverage = Faster Compounding Magic

Leverage ETFs will double or triple the daily returns of the index. This is important to understand because 2x leverage doesn't mean that you will do exactly 2 times the S&P 500 yearly return.

In the example above, during the period from Nov 2020 to Nov 2021, SSO (2x S&P 500 ETF) returned more than double what SPY returned (S&P 500). These are the 1-year returns of these 2 ETFs:

- SPY: +42%

- SSO: +103%

2x of SPY returns would be 84%, but SSO compounded in such a way that returned 103%.

During bull markets, leveraged ETFs will compound gains faster. Later in this article, I will show you some more examples of how leveraged compounding can give you superb outlandish returns.

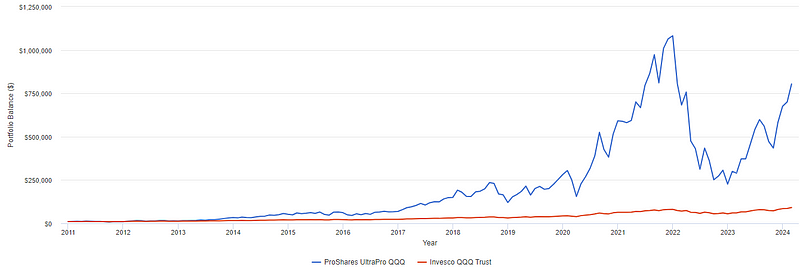

This compounding effect is such that the TQQQ — the Nasdaq 3x leveraged ETF — didn’t just return 3x QQQ but returned an astonishing 9 times QQQ since its inception in 2011:

This result is surprising and comes from the fact that leveraged ETFs will compound gains faster.

The same will happen during bear markets. Losses will compound faster too:

As you can see from the chart above, during the period from Apr 2022 to Apr 2023, while SPY lost -10%, SSO lost -25%. This is what most people are afraid of. Leveraged ETFs will amplify both gains and losses.

Volatility Decay — An Imaginary Cryptid

People who are against leveraged ETFs also highlight the “volatility decay” as a backdrop for leveraged ETFs.

Volatility decay is simply the principle that whenever the price of an investment drops, it takes more effort to come back to the same level. In other words, lots of ups and downs (volatility) will ‘decay’ the price.

If an investment drops by -20%, it will need a +25% to return to its initial value. If it drops by 50%, it will need a +100% to return to its initial value, and so on.

However, this volatility decays in nothing inherent to leveraged ETFs alone. Any regular non-leveraged ETF also has volatility decay.

The good thing is that leveraged ETFs can recover faster than non-leveraged ETFs from market drops and the effects of volatility decay. That’s what we see when looking at long-term data.

You can read more about the principles of volatility decay here:

We need to zoom out and look at the big picture when investing in leveraged ETFs. By looking at the whole picture — including the math of compounding — you will see that volatility decay is not a good reason not to use leveraged ETFs.

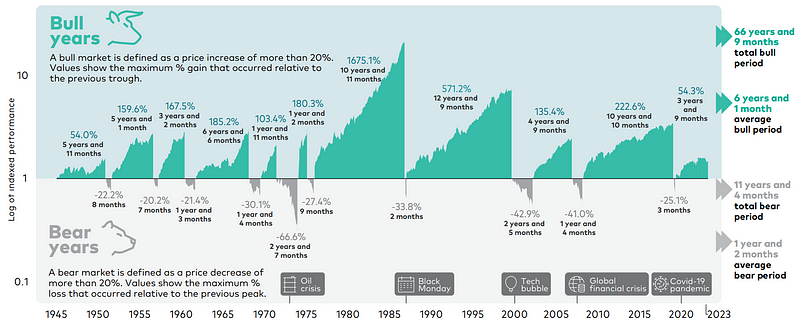

Bull market periods are usually longer than bear market periods.

If you manage to hold a Dollar-Cost Averaging during the bear market period, you can be rewarded wonderfully once the bull market kicks in and kills any volatility decay:

During bull markets, compounding will make a huge difference in your gains, dwarfing any volatility decay.

How Risky are Leveraged ETFs?

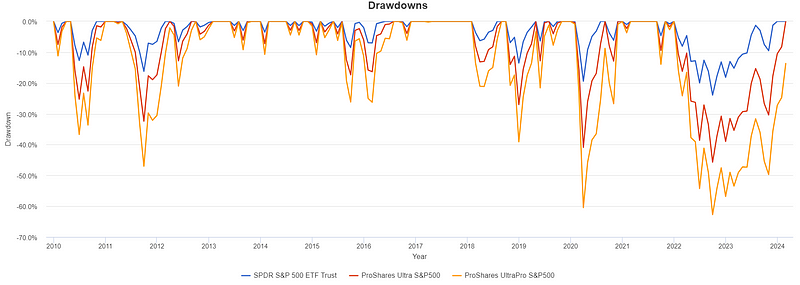

Drawdown is often used to measure an investment's risk. It measures the peak-to-bottom decline of an investment.

Drawdowns might be scary, and they are the main reason why most people stay away from leveraged ETFs. Stomaching a 60% decline in the value of your investment might be psychologically hard.

However, this fear exists only in the psychological realm.

The reality of the data is that leveraged ETFs recover very fast even from the worst drawdowns.

If you just ignore the market crashes and drawdowns, or better yet, if you use these moments to average down by adding to your ETF investments, you will do very well — the math doesn’t lie.

Even considering the drastic drawdowns, leveraged ETFs can produce outstanding results with very attractive risk-adjusted returns.

Let’s look at an example

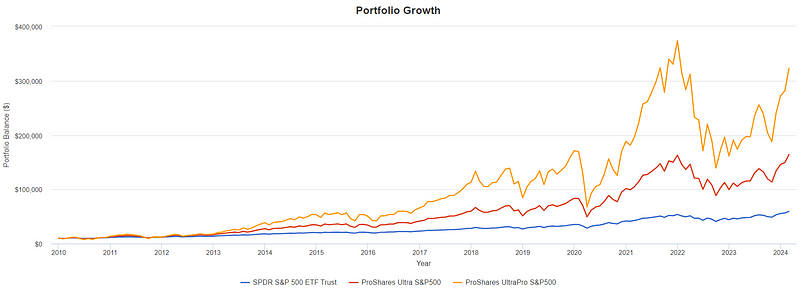

I’ve simulated the returns for 3 ETFs from 2010 to March 2024:

- SPY — SPDR S&P 500 - no leverage ETF: 490% return.

- SSO — ProShares Ultra S&P500 - 2x leverage ETF: 1,540% return.

- UPRO — ProShares UltraPro S&P500 - 3x leverage ETF: 3,120% return.

As you can see, the leveraged ETFs might have a better return, but they also have a higher Max. Drawdown.

If you want to follow this investment strategy, you need to be okay with this.

Drawdowns should be seen as part of the volatility of holding a high-performance asset, not as a loss.

Remember, you only lose if you press the sell button.

Looking at the historical data, 2x and 3x leveraged ETFs would always recover. You just need to hold them for the long term.

As I’ve been saying again and again, volatility is the price you pay for performance. In fact, as you can see according to the numbers above, over the 2010 to March 2024 period, the 2x leveraged SSO returned 3x what SPY returned, and the 3x leveraged UPRO also returned significantly more than 3x: an outstanding 6.3x times SPY.

These returns came this high even though SSO and UPRO suffered big drawdowns of 40% and 60%, respectively, in 2020 and 45% and 62%, respectively, in 2022.

The chart above shows the performance of the 3 ETFs over the 2021–2014 period.

So, are these ETFs risky? I’d prefer to call them volatile instead of ‘risky’.

Remember: There’s no such thing as great returns with little volatility.

Drawdowns are steep and painful to see, but there is no such thing as a low-volatility, high-return investment in the market.

Despite drawdown periods, leveraged ETFs can offer significant long-term returns, making it worthwhile for investors to hold onto them. Losses are typically temporary, and we can be confident in their ability to recover.

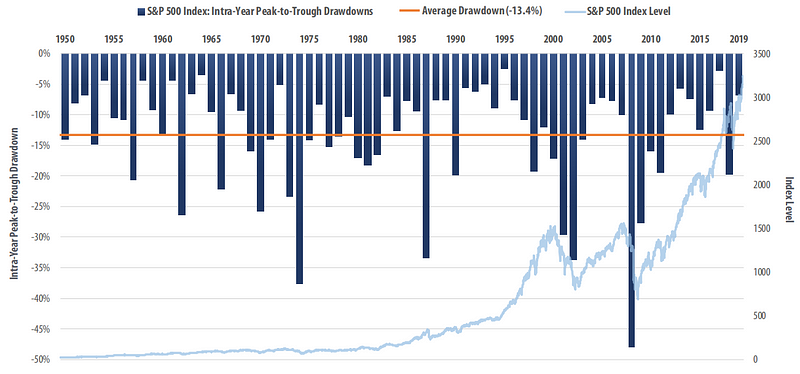

Drawdown periods or whenever the market crashes should be seen as a discount opportunity — a time to buy cheap — rather than a time to panic.

The chart above shows us the S&P 500 yearly drawdowns — these moments are great opportunities to buy. The comparison window is large enough for solid statistical measurements, and looking at the data from the last 70 years gives me confidence in this strategy.

I find it optimal to add to the investment whenever there’s a drop of 5% or more — think of this as buying products in a shop only whenever they are on sale. These sales are almost guaranteed to happen every year.

Another alternative is DCA — Dollar Cost Averaging. DCA is a great way of smoothing out volatility.

Nothing Ventured, Nothing Gained

I started my TQQQ investing journey in late 2021, and soon after, there was the 2022 market downturn. From the peak to the bottom, TQQQ dropped 80%.

Was I worried? No. Not at all.

Did I lose any money? Nope.

Despite the “scary” drawdown, my TQQQ investment is one of my best baggers.

Yes, drawdowns might be psychologically hard, but in the long term, these ETFs are expected to increase in value (unless there is an ultra-rare black swan event).

Still, to make this strategy work, you should only invest money that you don’t foresee needing over the next coming years.

Rest assured that leveraged ETFs such as the SSO, UPRO, and TQQQ would recover even from the harshest crashes and end up giving patient investors amazing returns.

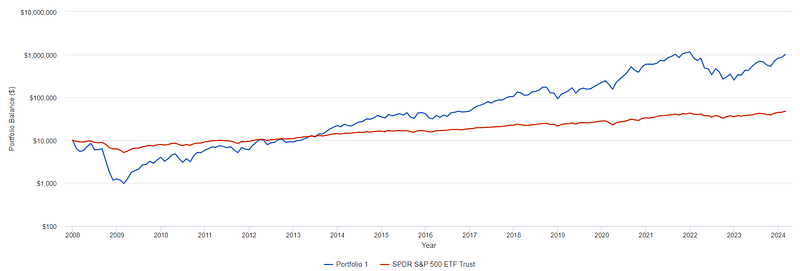

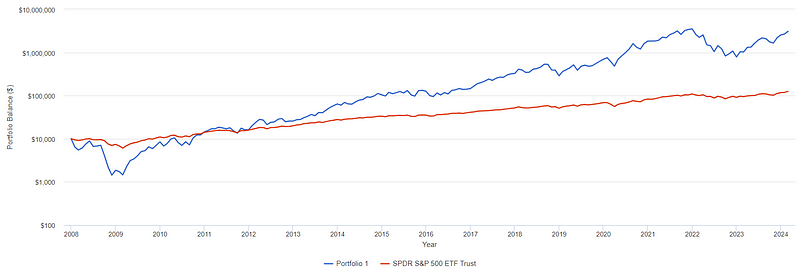

Let’s assume a worst-case scenario and see what happens to an ETF like the TQQQ, shall we?

Imagine: You invested $10,000 in TQQQ (3x Nasdaq 100 ETF) right before the 2008 crash—one of the biggest crashes in stock market history.

The drawdown would be pretty big — at the lowest, your account balance would be down to $1,000, i.e., a 90% drawdown.

It is pretty scary, but we need to look at the chart to see the whole picture:

As you can see, TQQQ (here, simulated in blue) would not only recover but also exceptionally outperform the S&P 500.

Even if you had invested at the peak of the subprime bubble and held through the 90% drawdown, your compound annual growth rate would be 32.8% compared to the S&P 500's 10.1%.

This means that if you had invested $10,000, it would now be worth $1 million. All this despite the 90% drop.

Dollar-Cost Averaging Leveraged ETFs

The best way to benefit from the drawdowns is to continue investing through these times.

If you have simply added $333 every 3 months to TQQQ, the results would definitely mean an early retirement:

In this case, you would have invested the initial $10,000 plus $333 every quarter, totaling a $25,000 investment.

If you did this using the SPY ETF (no leverage S&P 500), you would now have $125,144, but investing in TQQQ would have amassed over $3 million — that’s 24 times the return of SPY, showing how powerful compounding works.

Remember that during this period, there were several crashes and bear markets, including the big 2008 crash, the 2011 and 2015 selloffs, the 2020 coronavirus crash, and the 2020 bear market.

Despite all this, a $25,000 would have turned into $3 million — a 120 multiple on investment, which greatly gives me confidence that leveraged ETFs can and should be held for the long term.

When to Use Leveraged ETFs?

Leveraged ETFs should only be used if you don’t need the money for the next 10 years.

As we saw before, if, after investing, there’s a crash at the level of the 2008 crash, it might take years to fully recover.

This means that you should only invest a portion of your portfolio that you don’t plan to use soon, like for buying a house or paying the bills.

Young investors should consider allocating a larger portion of their portfolio to leveraged ETFs and eventually decreasing the leverage as they approach retirement age.

Leveraging Can Reduce Risk Over Time

— What?? Are you saying that leverage can reduce risk?

— Yup! That’s precisely what I’m saying.

Leveraging can help you diversify risk across time. Hear me out:

Typically, when you are young, you don’t have much money to invest in stocks. But later in life, you do allocate more money to stocks. This means that most of us will have less market exposure and risk less when we are young and higher market exposure when we are older.

By increasing your stock exposure earlier, you can diversify risk across time.

This is how people normally invest:

- When you are 30 years old, you have only $50,000 invested.

- Later, when you are 40 years old, you have $150,000 invested.

In this case, you are concentrating way more risk when you are 40 than when you are 30. What if you could diversify across time by using leverage ETFs?

In this case, by investing those $50,000 in a leveraged ETF such as SSO or UPRO, you would bring your market exposure to a level closer to what you would have a few years later. This way, you will have better diversification across time.

The strategy of using leverage ETFs, especially when you are younger, and then deleveraging later in life will increase your portfolio performance and your retirement nest egg.

I highly recommend reading the book Lifecycle Investing to dive deeper into the concept of using leverage to reduce risk.

What Are The Best Leveraged ETFs?

There is a wide range of leveraged ETFs to choose from, but you need to be very careful when choosing the right one.

Sector ETFs should be avoided because sectors are very often seasonal, unpredictable in the long term, and are more volatile than broad market ETFs. For this reason, I would not invest in ETFs such as:

- SOXL — Direxion Daily Semiconductor Bull 3x (ETF that invests specifically in the semiconductor industry).

- FAS — Direxion Daily Financial Bull 3X Shares (ETF that invests in the financial sector).

- NRGU — MicroSectors U.S. Big Oil Index 3X (ETF that invests in the oil sector).

Commodities ETFs should also be avoided (the market is hard to predict):

- UCO — ProShares Ultra Bloomberg Crude Oil 2X (ETF that invests in crude oil).

- AGQ — ProShares Ultra Silver 2X (ETF that invests in gold).

Here are the leveraged ETFs that, according to the data, would be eligible for long-term investing. They are all index ETFs that track the biggest stock market indexes — the S&P 500 and Nasdaq-100:

- SSO — ProShares Ultra S&P 500 (2x the S&P 500).

- UPRO — ProShares UltraPro S&P500 (3x the S&P500).

- QLD — ProShares Ultra QQQ (2x the Nasdaq-100).

- TQQQ — ProShares UltraPro QQQ (3x the Nasdaq-100).

- TMF — Direxion Daily 20+ Year Treasury Bull (3x treasury bills).

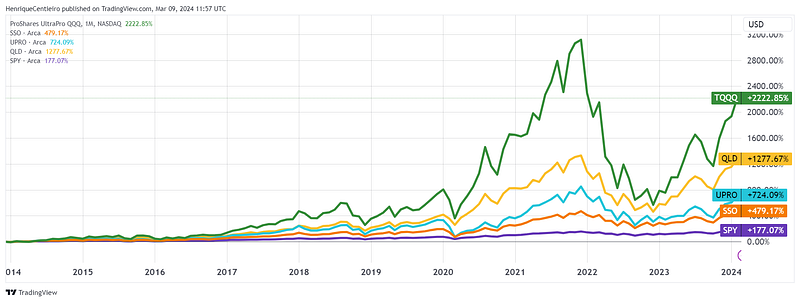

Here’s the 10-year chart with TQQQ, SSO, UPRO, QLD and SPY:

The 10-year returns are amazing, but after reading this article, they should not surprise you.

While SPY returned 177%,

SSO is up 479%, UPRO 724%, QLD 1,277%, and TQQQ 2,222%.

Other than the ETFs listed, others give you equivalent results. For example, SPXL — Direxion Daily S&P 500 Bull is the same as UPRO, just from a different issuer. It’s up to you to decide which ETFs you should invest in.

Finally, you are probably wondering why TMF, the Treasury Bill ETF, is on the list.

I have included it because Treasury bill performance is often uncorrelated to stock market performance. This ETF might be added to smooth out volatility. I might write another article about it, but Daniel Fernandez already did an amazing job covering it in the book Passive Investing on Steroids.

Where Can You Get More Information on Using Leverage ETFs for Long-Term Investing?

I would HIGHLY RECOMMEND reading the two books below that cover using leverage for long-term investing. These two books explain in way more detail and depth why and how to use leverage ETFs to fund your retirement:

To Wrap Up

This article shows you how to use leveraged ETFs for successful long-term investing — we have looked at the volatility, returns, drawdowns, and strategies to maximize performance, such as adding to your investments when the market has a downturn and using DCA — dollar cost averaging.

Leverage ETFs are not necessarily extremely dangerous or unpredictable, as many people point out — by analyzing the numbers and historical data, we understand that leverage ETFs can greatly maximize your returns, and they have great potential as part of a diversified portfolio.

Although the assumptions in this article are not without risk, I do have my money where my mouth is. Leveraged ETFs correspond to approximately 30% of my entire portfolio.

It took me years of research, reading books and papers, and backtesting to finally have the conviction to write this article.

I highly recommend you do the same before investing.

Should we revisit this article in 10 years?! 😊💰📈

If you found any value in this article, throw me some Medium love!

🥰 To support my work: Clap up to 50, leave a message to share your thoughts & be sure to follow. 💌

🌞 Stay in touch: