Why You Need Leveraged ETFs for Long-Term Investing — IF You Find the Optimal Leverage!

Explore the myths & maths behind leveraged ETFs and learn how the first-ever “Optimal Leverage Indicator” helps you find optimal leverage.

When I was 20 years old, I was playing around with leverage (up to 200X) and subsequently blew up my brokerage account. Luckily, I didn’t lose that much money because I was just a student at the time. But back then, it felt like a huge blow because I had grown that account from $500 to $5,000 and then watched it go straight to zero.

Following that experience, I swore to never use leverage ever again.

This was until 5 years ago when I began to study and invest in leveraged ETFs.

Although I’ve previously written a complete guide on leveraged ETFs, today, I want to explore the concept of optimal leverage and discuss why leverage might be a suitable strategy for long-term stock investing.

Be sure to check out the comprehensive guide I recently published on leveraged ETFs:

They said, “Leveraged ETFs are not suitable for long-term buy and hold.”

Many people make such statements without doing the math. But have you asked the question: why are leveraged ETFs considered unsuitable for long-term investing?

If you follow these statements, you might miss out on significant returns.

In my previous articles about leveraged ETFs, I have always had readers who argue that they cannot be used as a long-term investment tool.

However, these claims are often not backed by math or data. In this article, I will present the mathematics that demonstrates the fact that leverage is not inherently negative, outline the ideal levels of leverage, and explain how to apply it effectively.

There’s one thing I do agree with: Excessive leverage can decimate your portfolio. It’s certainly not wise to apply 200X, or even 10X, or 5X leverage to an S&P 500 index ETF.

But what about more conservative levels, such as 1.5X, 2X, or 3X leverage?

The Volatility Decay Argument: Does Volatility Really Eat Away Long-term Returns?

Most people that argue against leverage ETFs talk how volatility decay will erode leveraged ETFs.

If volatility truly diminished returns, then non-leveraged funds would also be unsuitable for buy-and-hold strategies, since they are equally susceptible to volatility.

The fact that non-leveraged ETFs remain a staple in long-term investing strategies undermines the argument that volatility is the main factor behind the reduced returns in leveraged ETFs.

Let’s look at some math

I extensively explain the math of volatility decay here, but in a nutshell, this is where the myth that leveraged ETFs are ineffective for long-term investment started:

(1 — x)(1 + x) = 1 — x²

Let’s clarify this with an example. Imagine the market declines by x% one day and then increases by x% the next day. For instance, the market falls by 10% and subsequently rises by 10%. The net result is (1−0.1)×(1+0.1)=0.99, which equates to a decrease of 0.01, or 1%.

This can also be calculated with the leg 1-x² like this 1–0.1² = 0.99.

So whenever the market experiences volatility, the math says we lose money. The greater the value of x, the larger the impact of volatility drag. So for a leverage ETF that returns 2 times or 3 times of x, we will have multiples of the volatility drag.

But remember, even with a leverage of 1 (i.e., no leverage at all), we also have volatility drag. When a stock or ETF declines by 10%, it requires an 11% increase to return to the original level. If it drops 20%, it needs a 25% gain to recover. A 50% fall requires a 100% increase… and so on.

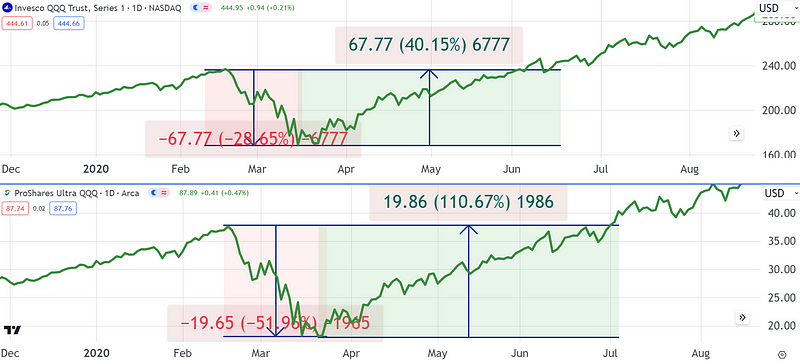

Let’s zoom in on the 2020 crash and analyze the effects of volatility drag:

The chart on the top shows QQQ, the non-leveraged Nasdaq ETF. When the market dropped by 28%, Nasdaq had to recover 40% (not 28%) in order to return to the same level.

However, QLD, the 2X leveraged Nasdaq ETF at the bottom, dropped by almost 52% and had to recover 110% (not 52%) to return to the same level.

So yes, 2X leverage has drag… but so does 1X leverage!

If everyone considers 1X leverage to be safe to hold forever, then what about 1.1X leverage? Is that also safe? And how about 1.5X leverage? Why is 2X leverage perceived as suddenly so ‘risky’?

Perhaps 2X leverage is safe and suitable for long-term holding. I’ve done the math for you.

The Myth Is False

The proponents of the myth have overlooked two critical factors that determine the returns of leveraged ETFs: benchmark returns and benchmark volatility (with the benchmark being, for example, the Nasdaq 100 or the S&P 500).

When the benchmark has a positive return, leveraged exposure can be beneficial and may offset the volatility drag.

However, it is important to note that while the return is proportional to the leverage, the drag is also proportional to the square of the leverage. As a result, there is a threshold beyond which the volatility drag will outweigh the additional returns gained from leverage. Therefore, there’s a limit to the amount of leverage that can be effectively employed.

This leverage simulator illustrates the concept very well.

So, What’s the Optimal Leverage?

The paper from Tony Cooper ran the numbers and created a model that I have further applied to determine the current ideal leverage for any asset.

In a nutshell, it calculates the optimal leverage using the following formula:

optimal_leverage = mean_return / (volatility^2)This simple formula shows that the optimal leverage is proportional to the ratio of the returns to the square of the volatility. Higher mean returns justify higher leverage, while increased volatility demands lower leverage to maximize the compound growth rate.

Too little leverage fails to capitalize fully on the positive expected return. However, excessive leverage results in volatility drag overwhelming the enhanced returns.

Optimal leverage achieves a balance by maximizing the difference between the amplified mean return and the volatility drag.

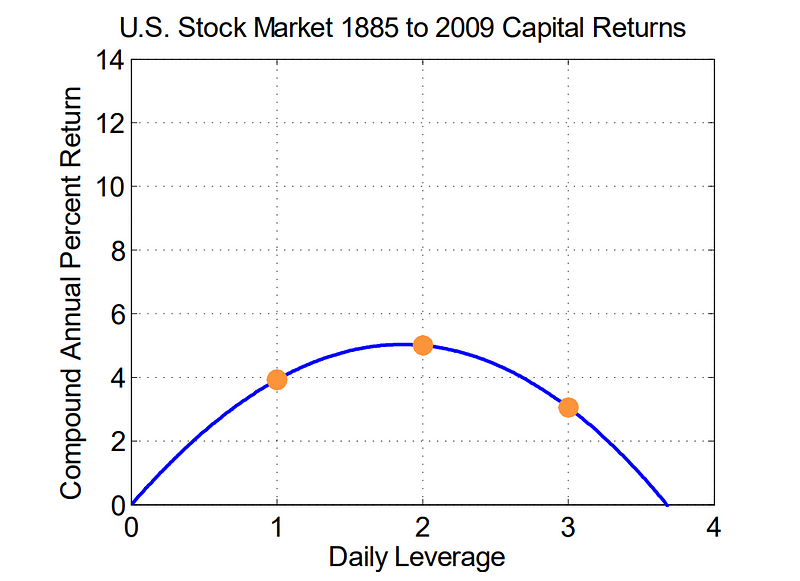

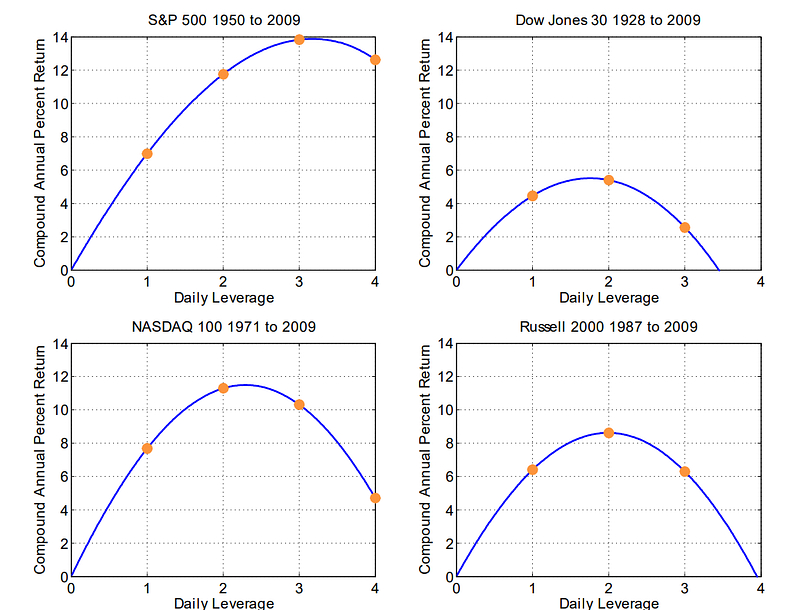

So after running the math, they produced a chart indicating that, over a 135-year period, the ideal leverage for the US stock market would have been 2X:

As you can see, 2X leverage would have optimized annual returns, whereas 3X leverage would not have been ideal. It’s important to note, however, that the 135 years of data include all the major market crashes, including the 1929 Great Depression.

What about other indexes? Let’s take a look:

According to large data samples, the ideal leverage for different indexes would have been:

- S&P 500 (60 years of data): 3X leverage

- Dow Jones (80 years of data): 2X leverage

- Nasdaq 100 (40 years of data): 2X leverage

- Russell 2000 (22 years of data): 2X leverage

So, yes, according to extensive data, even dating back to 1885 and including the worst market crashes with the worst volatility ever, you would still benefit from using at least 2X leverage.

However, there is an issue with these calculations — they appear outdated.

To determine the appropriate leverage we should use for current conditions, we must analyze not only large datasets but also more recent data — to achieve this, I have developed a script that calculates a more up-to-date optimal leverage for any index or asset that you want.

The First-Ever Created Optimal Leverage Indicator

This indicator that I have created on TradingView calculates the Optimal Leverage for any desired asset using daily returns, mean returns, and market volatility.

My Optimal Leverage Indicator tells us what the ideal leverage would be for past market conditions to optimize returns without being eaten away by volatility drag.

Here are some interesting results:

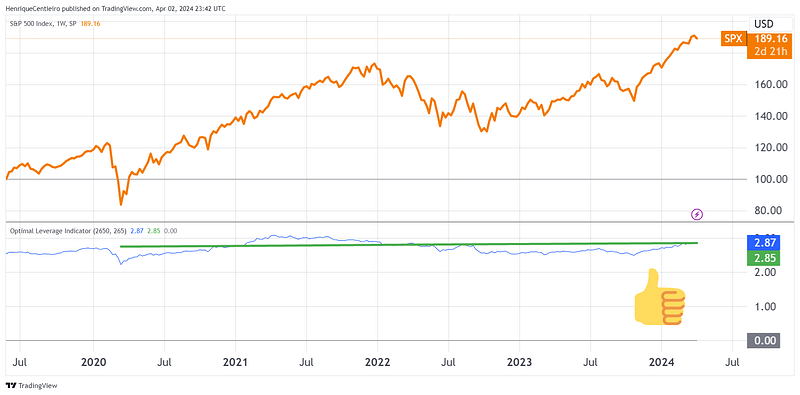

S&P 500

According to my indicator, the ideal leverage for the S&P 500 would have been 2.85X. This is pretty close to the 3X shown in the previous charts.

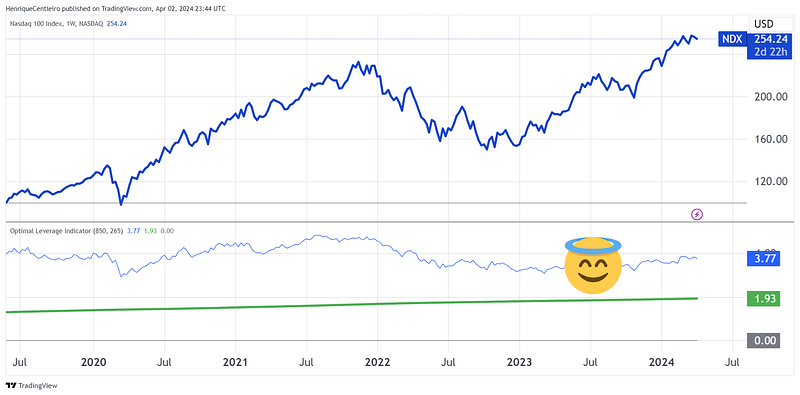

Nasdaq 100

Then, my Optimal Leverage indicator tells us that the optimal leverage for the Nasdaq 100 Index is 1.93X. Again, this is really close to the 2X seen before in the article.

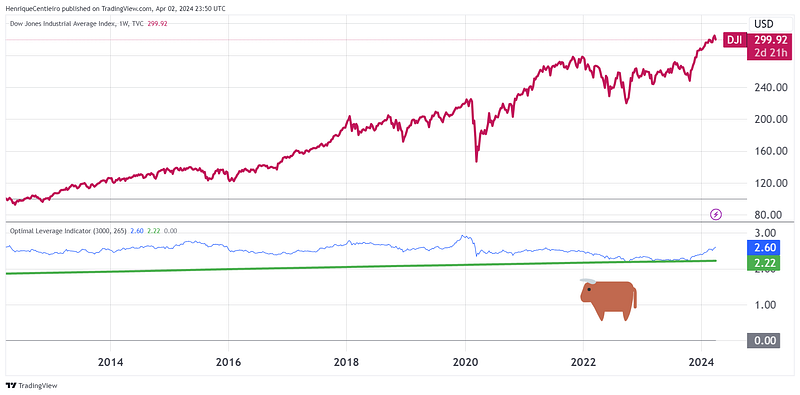

Dow Jones

What about Dow Jones? Well, the previous chart with 80 years of data gave us an Optimal Leverage of 2X, and my indicator gives us 2.22X.

Ok, what about Bitcoin?

My indicator advises against leveraging Bitcoin, and this is probably true for any other cryptocurrency.

It is important to note that the leverage discussed in this article applies to long-term investment strategies.

While Bitcoin may surge by 150% in one year, presenting a tempting opportunity for leveraging, it can also plummet by 70% — as observed in the previous bear market — which would be devastating for any leveraged positions.

Which Leveraged ETFs Fit The Optimal Leverage?

Here’s a (very short) list of Leveraged ETFs:

- SSO — ProShares Ultra S&P 500 (2x the S&P 500).

- UPRO — ProShares UltraPro S&P500 (3x the S&P 500).

- QLD — ProShares Ultra QQQ (2x the Nasdaq 100).

- DDM — ProShares Ultra Dow30 (2x the Dow 30).

There are other ETFs from other issuers with similar leverage levels that you can explore on the VettaFi website.

These ETFs rebalance automatically and have relatively low fees — usually under 1% — which is better than paying interest on a margin account or getting a loan in order to leverage.

To see my analysis on leverage ETF returns, make sure you read this article:

Conclusion

You don’t need to leverage your S&P 500 by 3X. Perhaps adopting a conservative approach with 2X leverage might be preferable. Alternatively, you could leverage the Nasdaq 100 by 1.5X — instead of the 2X previously discussed — by combining QQQ and QLD.

The point is that having a moderate amount of leverage can improve your returns while still aligning with your risk tolerance.

Remember:

- Leverage itself is not inherently bad; rather, the challenge lies in identifying the optimal leverage level.

- Volatility drag affects both leveraged and non-leveraged investments, not exclusively leveraged ETFs.

- Historical data shows that 2X leverage has been optimal for various indexes over extended periods.

- The optimal leverage is directly proportional to the ratio of returns to the square of volatility.

- My “Optimal Leverage Indicator” can help you determine the current optimal leverage for any given asset.

I would love to know your thoughts on this and keep the conversation going. This is a topic that definitely needs extensive discussion!

If you found any value in this article, throw me some Medium love!

🥰 To support my work: Clap up to 50, leave a message to share your thoughts & be sure to follow. 💌

🌞 Stay in touch: