How the Innovation Process Works in the Business World

A discussion on the five elements of innovation

To begin, it’s worth noting what Peter Drucker said about innovation:

“The business has…two basic functions: marketing and innovation. Marketing and innovation produce results; all the rest are costs” — Peter Drucker

This article will explore the following five elements:

- Introduction and Definitions

- Innovation and Change

- Why Companies fail to Innovate

- Types of innovation

- The Innovation Process

“Have the courage to follow your heart and intuition. They somehow already know what you truly want to become.”— Steve Jobs

1. Introduction

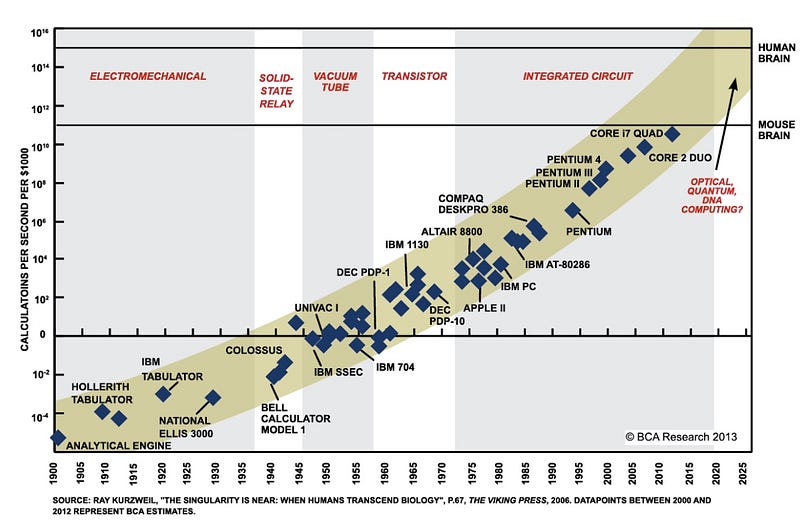

To begin, allow me to remind readers bout Moore’s Law.

Moores Law

In 1965, Intel co-founder Gordon Moore identified a trend that the number of components in integrated circuits doubled every 2 years.

This trend has continued for 50 years but by 2020 is expected to slow to every three years.

That said, this doesn't apply to all industries, the semiconductor industry is constrained by size — processer dimensions.

Definitions and quotes

Now let’s take a look at some noteworthy quotations:

Innovation quote #1

“A major innovation is one that sparks further innovations and investment (e.g. the computer) as opposed to other innovations which are primarily improvements” — N. Rosenberg (1986)

Innovation quote #2

In 2008, JP Deschamps said:

“Innovation is a process by which a company:

- Builds insights about its customers

- Identifies and evaluates unique market opportunities and prepares a plan to seize them

- Develops a stream of winning products” — JP Deschamps (2008)

Innovation quote #3

Prior to Deschamps, Doyle noted:

“An Invention is a new product; an Innovation is a new customer benefit” — P. Doyle (1995)

Innovation quote #4

Richard Duggan followed Doyle with his observation, describing it as:

“..the ability to look where everyone else is looking and see what no-one else can see.” — Richard J Duggan (1996)

Innovation quote #5

Lastly, two quotes from Geoffrey Nicholson of 3M:

“Innovation is the practical application and use of creativity. Creativity is thinking up new things. The invention shows it can be made, innovation is making it commercially valuable.” — Geoffrey Nicholson, 3M

Innovation quote #6

Nicholson also noted:

“Research is the Transformation of Money into Knowledge — Innovation is the Transformation of Knowledge into Money” — Geoffrey Nicholson, 3M

2. Innovation and change

Innovation is simply defined as the process of change. Or simply making change. Changes to products, processes or services. As such, the terms ‘innovation’ and ‘change’ are often used interchangeably.

- Change management is often treated as a generic type of change in organizations that includes broader issues such as the psychology behind the change.

- Innovation management is a more applied type of change and often focuses on idea generation and project management.

Nature of change

- Planned change is a formal and typically annual process of converting the organization from one state to another.

“Change can be planned or emergent” (Tidd, Bessant, et al. 1997)

- Emergent change is contingent on other changes taking place in the environment and recognizes that change is an open-ended process.

Airline case study

Low-cost airline Ryanair grew dramatically in the 90s because of innovations they adopted in their online purchasing and ‘no frills’ approach to air travel.

Giant rivals, such as British Airways, were quickly overtaken in terms of company value on the stock exchange, so much so that they had little choice but to adopt the same no-frills innovations in order to compete.

Customers no longer expected meals, but rather were attracted by the low cost and high efficiency that came with buying their own tickets online.

3. Why some companies fail to innovate

Most organizations invest in innovation today, but some don’t.

Organizations allocate a proportion of turnover to make changes to their products, processes, and services. There are particular reasons or objectives that should be achieved as a result of this investment.

Research has shown that a very large percentage of innovations fail to meet these objectives. The reasons behind failure give us clues on how to avoid failure in the future.

Each year, organizations spend a huge amount of turnover on innovation i.e. making changes to their established products, processes and services.

The amount of investment can vary from as low as a 0.5% of turnover for organizations with a low rate of change, to anything over 20% of turnover for organizations with a high rate of change.

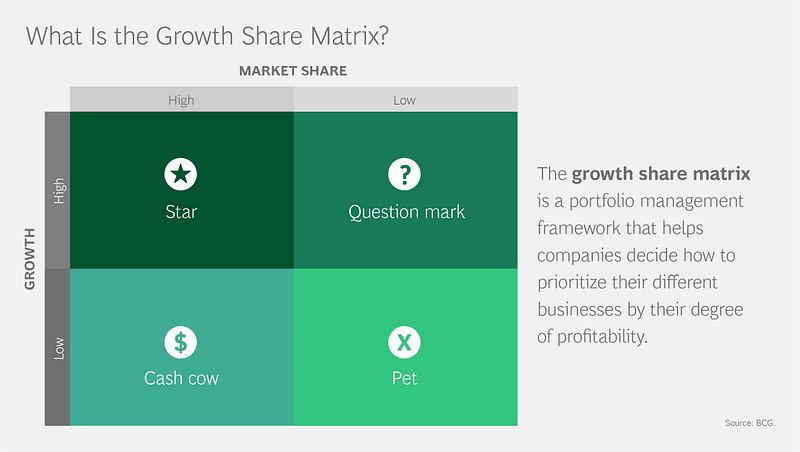

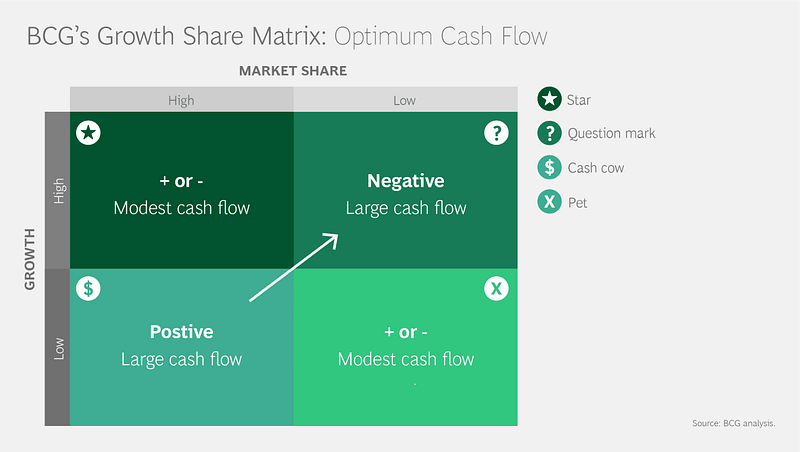

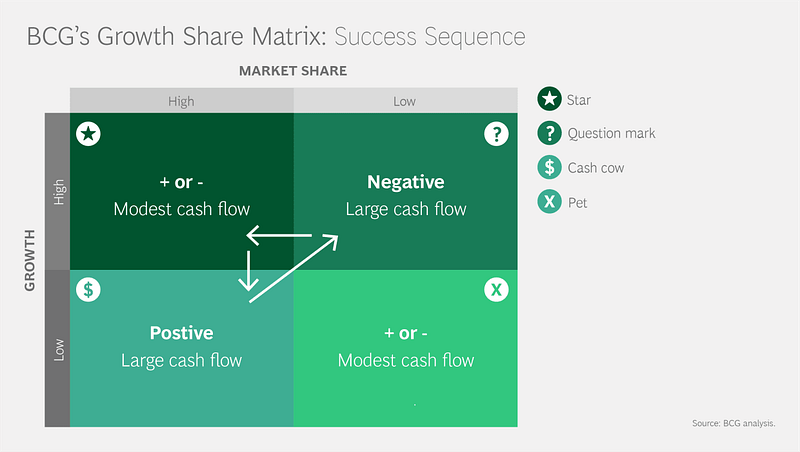

Boston Consulting Group Matrix

This matrix can guide companies as to where to invest in innovation.

The BCG matrix guides the allocation of funds based on market share and sector attractiveness into four quadrants:

- Cash cow

- Shooting star

- Dog

- Question mark

Companies fail at business model innovation because they’re so busy pedaling the bicycle of current business models (Cash Cow), they leave no time or resource to design new ones.

Most companies focus on innovation efforts on new products and on driving efficiencies into existing models.

Although important activities, they’re inadequate in the 21st century when business models don’t last as long in the face of disruption. This means business model innovation is the new strategic imperative.

The most obvious reason companies fail at business model innovation is because CEOs or senior leadership within organizations don’t want to explore new ways— Some CEOs just don’t want a new business model.

- They are content with the current one and want everyone in the organization focused on how to improve its performance.

- The clearest indication is when any discussion about emerging business models is viewed and treated solely as a competitive threat.

Product is king

The lines are blurring between product and service business models.

Take the iPod for example. Apple didn’t launch the first MP3 player in the market. Yet, the company changed the way we experience music by delivering on a value proposition that bundled product (iPod) and service (iTunes).

Industrial era thinking forces a false choice between product or service focus. A proud product heritage can get in the way.

Technology

Many companies fail because IT resources are disproportionately allocated to support legacy systems.

- Deploying new capabilities takes a back seat.

- The prevalence of enterprise systems is a barrier to business model innovation.

- A change anywhere within the organization affects every function, making it difficult to develop new capabilities, let alone an entirely new business model.

- Enterprise systems increase the efficiency of the current business model but can be a straightjacket-constraining business model innovation.

Organizational barriers

It’s hard enough to be at war with the competition, so why compete internally too?

- When some executives look at new business models they see them through the lens of the current business model and view them as competition.

- How change or innovation effects a department or function should be peripheral to the central goals of Innovation.

Financial Metrics

Financial metrics to assess alternative projects reflect the cost structure and required returns to sustain and grow today’s model.

- New business models are likely to have very different economics and must be assessed in that context.

- Most new business models will be dismissed out of hand if judged by the economics and constrained by the ROI requirements of the current model.

- Organizations fail at business model innovation because they apply the wrong financial lens in assessing the attractiveness and feasibility of new business models.

Embracing new ideas

Many organizations fail at business model innovation because they shoot their renegades. If they don’t shoot them they wear them down until they leave.

- Business model innovators go against the corporate grain. They see entirely new ways to create, deliver and capture value.

- Organizations must learn to celebrate and support people within the organization who are willing to challenge the status quo, to bring totally different perspectives on delivering value to the table and are willing to take experimental risks to explore new models.

- Leaders will have to overcome their resistance to exploring new business models even those that may be disruptive to the current one

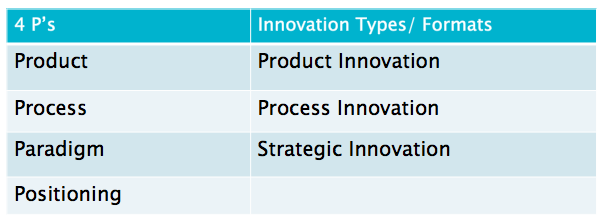

4. Types of innovation

According to Ahmed & Shepherd (2010) innovation has different formats that fall into two categories: those within the firm’s control and those outside of the firm’s field of influence. In general the fit into three areas:

- Product Innovation

- Process Innovation

- Strategic Innovation

Let’s compare the four P’s of Innovation largely used by Tidd & Bessant to the innovation types favored by many authors.

With the exception of positioning (which falls under Process Innovation), they essentially relate to the same concepts.

Product innovation

Most of our discussion to date has been with product innovation, which can be radical or incremental innovation.

- Product innovations are either technology-driven or Market-driven.

- The embodiment of an innovation is often observed in the visible functional characteristics of a product. For example, a shift from mechanical typewriters to word processors.

Ahmed and Shepherd (2010) highlight the value of marketing efforts in promoting innovative products using the “Wash & Go” example.

Unilever’s “2-in-1” shampoo failed despite possessing a technological advancement, not captured in any other competitive offer at the time.

P&G’s “Wash & Go” succeeded as it was accompanied by a very successful marketing and brand building campaign.

Process innovation

Process Innovation refers to the change in the conduct of business organizational activities:

- Operational efficiencies and improvements are all examples of innovation of process.

- Innovations can also be grouped by business function — marketing, sales, finance, engineering, and logistics.

Hundreds if not thousands of examples could be listed in this section alone.

Strategic innovation

Using the four P’s model involves innovations of the business paradigm.

“Strategic innovation often involves either a significant adaptive shift in the organization’s current business model or adoption of a new business model” (Ahmed et al, 2010)

Strategic innovation is not just driven by technological innovation.

The 2005 merger of Procter & Gamble with Gillette in the fast-moving goods sector was partly to build brand portfolio strength to combat the growing power of the retail giants such as Tesco and Wal-Mart.

In Ireland, Musgraves offers free franchise opportunities for small retailers to join together to take on Dunnes Stores and Tesco:

- Basket Shoppers — Centra

- Trolley Shoppers — Super Value

Hewlett Packard case study

In the past, HP excelled at strategic innovation.

- It transformed itself from an instrumentation company to a computer company in the 1980s and then into a leading manufacturer of printers.

- It extended to chips, components, computer networking and services for businesses this century.

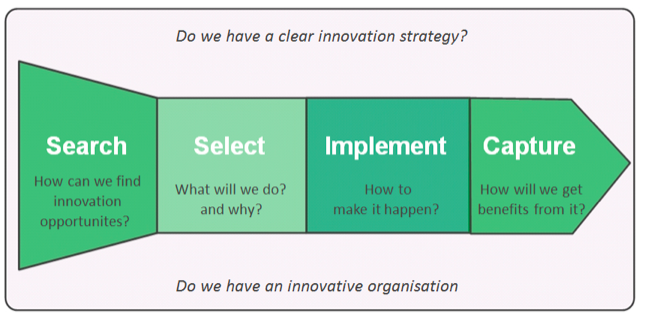

5. The innovation process

The process of innovation proposed by Rogers comprises of the following eights stages (Rogers, 1983):

- Recognition of a problem or need

- Preliminary evaluation

- Invention

- Research and development

- Evaluation

- Commercial development

- Adoption

- Post-adoption consequences

Tidd & Bessant (2009) proposed a four-stage process:

- Search

- Select

- Implement

- Capture

Search

The first stage in the Innovation Process is simply called Search. This is the creative phase in the process and in many respects the most difficult.

- How do we find innovative ideas?

- Ideas for incremental innovations mostly come from market research and feedback on current versions of products and services, but what about more radical forms?

“Idea generation seems to be the really innovative part of the whole process, the part that demands some spark of creativity, the essence of innovation” (Blythe, 1999)

Select, implement and capture

The article below discusses the post-search (ideation) stage in more detail.

Final thoughts

Sources of innovation can occur in various ways. Based on the information available from industry experts discussed above there are 5 key takeaways to remember:

- Knowledge Push — One obvious source of innovation is the possibilities that emerge as a result of research.

- Need Pull — Necessity is the mother of invention and innovation. WW2 saw huge developments in radar, rocket-power, aircraft, computing, jet engine, coding, and communications.

- Inspiration — Random eureka moments of inspiration.

- Regulation — The introduction of new laws can force companies to innovate to uncover new opportunities.

- Accidental— Penicillin, Plastic, Fanta and even Coca-Cola were all accidental discoveries.

Utterback (1976) found that around 70–80 percent of innovations result from ‘demand-pull’, whereas 20–30 percent from ‘technology-push’.

R&D engineers might argue that demand-pull provides plenty of ‘slight product modifications’ but truly innovative products and major breakthroughs have come from technology push (Shanklin, 1983).

To conclude, albeit small (20–30%) knowledge-push or technology-push (as adopted by Apple) has proven to be the source of highly profitable, true innovation — Revolutionary innovation.