How Saving for Retirement Actually Screws a Lot of People

Are you saving too much for retirement?

Don’t overcommit to saving for retirement.

That sounds ridiculous, doesn’t it?

Why wouldn’t you prioritize building wealth and ensuring a smooth transition out of the workforce one day?

I’m not saying don’t save for retirement — just that you should revisit your strategy, especially if one of the next two sentences describes you:

- Your only form of investing is automatic contributions to a 401k or IRA.

- Your paychecks accumulate in a checking or savings account.

While these appear as two separate characteristics, they’re sequentially related. A lot of people are satisfied with only saving and investing for retirement. They think they’re financially prepared just because a percentage of every paycheck is set aside for the future. In turn, they let the rest of their income sit in a bank account.

That’s a problem.

Why? Because it ignores an important fact: retirement isn’t your only financial goal.

Before I show you how to adequately save for retirement and other life events, let’s explore the problem.

Retirement Is Not Your Only Financial Goal

You’re probably thinking: “Well, yeah, that’s pretty obvious.” (And if this surprises you, I’m concerned for your financial well-being.)

Life is expensive as hell. Everything costs money. Yay capitalism!

There are plenty of other major life events that require significant sums of cash, such as buying a house, going back to school, raising kids, paying for those kids’ education, and so on. And these events will likely take place before you retire.

Unless you have a money tree in your backyard, it’s a good idea to allocate savings and invest toward your other life goals too.

Yet, I know countless people whose only form of “saving” is their automatic contributions to a 401k or IRA. Many of these same people let the remainder of their excess earnings accumulate in a checking or savings account, which isn’t really saving. That’s just hoarding.

Since these accounts yield minimal interest income, they lose value over time thanks to inflation.

When you overcommit to retirement (or only commit to retirement), you’re handcuffing a significant portion of your money, while simultaneously neglecting the remainder. You typically can’t access your retirement funds (without penalty) until you reach the prime age of 59 ½. Needless to say, there’s a good bit of life to live before you hit 60.

If you’re ultra-conservative and don’t trust financial markets, that’s your prerogative. I’ve seen plenty of personal essays about people’s distrust of the stock market, cryptocurrencies, and pretty much anything that isn’t cash. If you have the cash savings to achieve your goals, that’s incredible — good for you.

Otherwise, a calculated investment plan can help your savings grow to a point where you can afford to put a down payment on a house, reduce your student loans, pay for your kid’s college education (tuition isn’t going down anytime soon), and save for retirement.

The solution: reverse engineer your financial needs to strategically balance your savings.

The Solution to a Life of Many Financial Needs

The solution is pretty straightforward, but it takes some calculating.

Make a list of your goals, including expected funds needed and an estimated timeline. (Time is important because it helps you prioritize more pressing goals.) Then you can back into the amounts you need to save for each goal and then apply allocations.

And, of course, you can adjust these amounts as you sit fit.

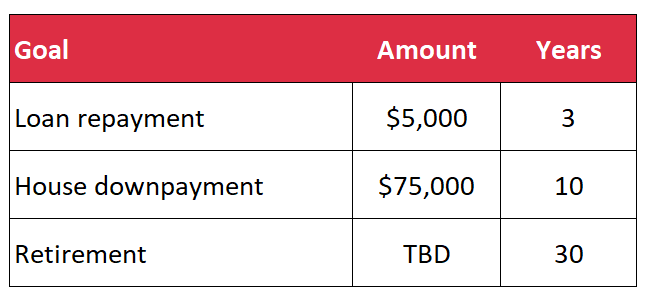

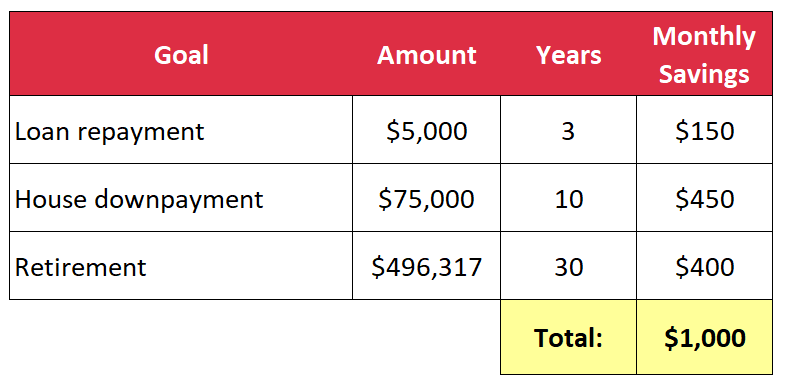

For example, let’s assume you have $1,000 of savings each month (and you’ve already established an emergency fund). Let’s also assume you want to save for three milestones:

- Paying off a $5,000 loan in 3 years

- Putting a 20% downpayment on a $350,000 house in 10 years (i.e. $75,000)

- Retiring in 30 years

Here’s a summary chart:

For simplicity, we’ll use a 5% interest rate for your loan and a 7.5% rate of return for your investments; we’ll also conservatively assume your monthly savings stay the same and that you haven’t saved a dollar up until now.

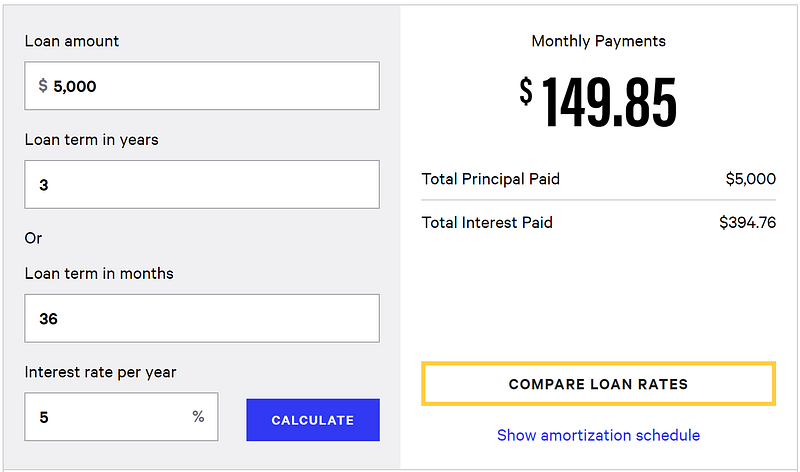

Let’s start with your loan. How much of your savings do you need to apply to your loan to pay it off in three years? Using a loan payoff calculator, you can determine that you need to set aside roughly $150 per month for debt payments.

That leaves $850 for your investments.

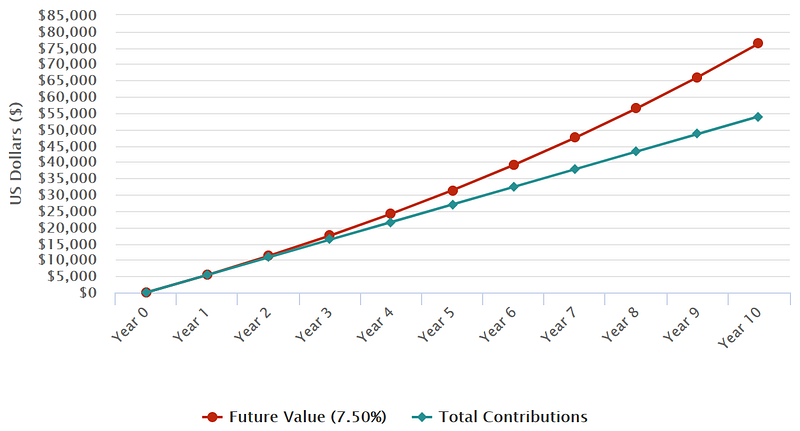

Next, your future house. Using a compound interest calculator, you can back into how much you need to allocate toward your house to reach a $75,000 downpayment in 10 years. Based on our assumptions, you’ll accomplish this goal with monthly contributions of $450.

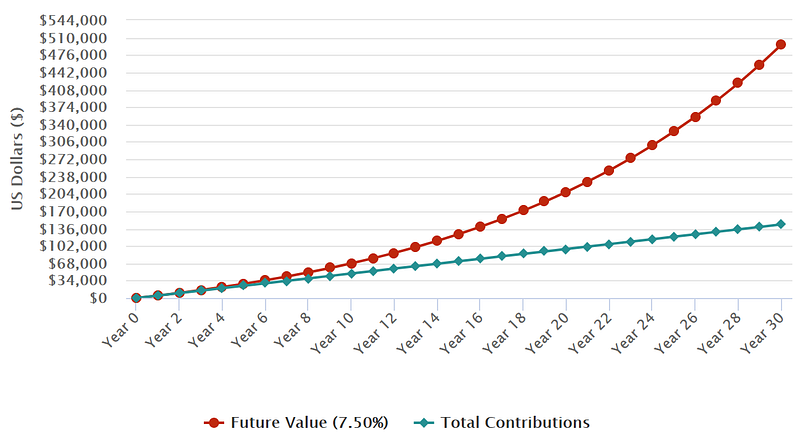

That leaves $400 per month for retirement in 30 years. Using the same compound interest calculator and assumptions, your retirement portfolio could be worth roughly $500,000.

In reality, as you approach the end of your investment timeline, you should reallocate your portfolio to prioritize safer investments to avoid undue risk; the stock market tends to increase over time, but you can’t predict what it will look like in a particular year.

Considering retirement is changing, that may not be enough to cover a full-fledged, work-is-for-suckers retirement — which would be solid justification for finding ways to save money. That said, half a million dollars enables you to at least scale back and/or pursue other interests.

With our calculations complete, let’s revisit our updated summary table, which now includes our saving allocations.

Again, this is just an arbitrary example with simplified assumptions. Obviously, life is much more complicated with many more variables. But the process for splitting your savings is still the same.

Long story short, don’t forget about (1) your pre-retirement life and (2) the wealth-building power of investing. Instead of aimlessly going through life, set some goals (which can change) and devise a plan for how you will afford them.

If you want to understand what makes a “good” investment, sign up for the Due Diligence newsletter. We provide free reports so that you can make logical and informed decisions instead of speculative risks.