How to Invest When You Know Nothing About Investing

A comprehensive guide for anyone who wants to invest — but doesn’t know where to start.

You don’t need to be a financial advisor or wall-street big shot to invest.

It’s okay to have a lot of questions and doubts. It’s normal to be hesitant to start investing. That’s true of most of the firsts in our lives. Learning to drive, going on a first date, riding a rollercoaster, skydiving (I’ve never done it — but I’d be shaking in my boots). Investing is no different.

But, unlike skydiving, learning how to invest needs to be a priority.

If you’re serious about investing (and you must be, because you’re here), I urge you to read every step carefully.

This isn’t a short post because it shouldn’t be. Learning how to invest isn’t as complicated as you think, but you need to understand several concepts first. And we need to go over a few personal questions that you need to ask yourself.

Since this post is rather long, here’s a section-by-section overview:

Why is investing important?

Investing puts your money to work. It employs your money with a steady job. The sole purpose of that job? Making you more money. And that’s the key to wealth and financial stability — having your money work for you, rather than you work for money.

With your money working for you, you’ll be better positioned to turn your life goals into a reality. Buying a house, getting married, going back to school, traveling the world, comfortable retirement — you name it.

Investing allows you to take advantage of a powerful economic principle: compound interest.

“Compound interest is the 8th wonder of the world. He who understands it, earns it; he who doesn’t, pays it” — Albert Einstein

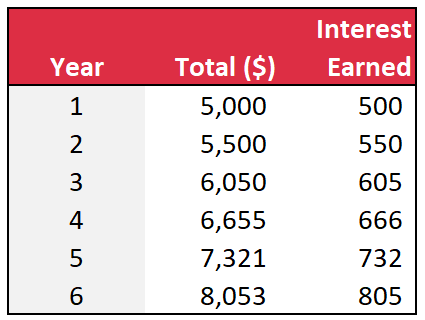

Compound interest is the process of your money earning money, and then THAT money earns more money. I know, that sounds kind of weird and might be hard to follow. So, here’s a simple picture overview

Here’s a numerical example. Let’s say you invest $5,000 today, and it earns 10% interest each year. In the first year, you earn $500 of interest. In the second year, you earn $550 of interest. In year three, you earn $605 of interest (see where I’m going?). Your investment compounds (hence, compound interest).

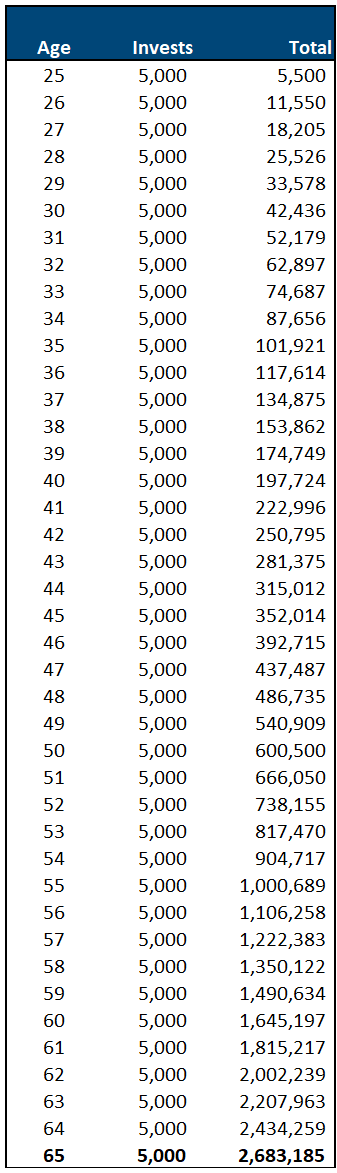

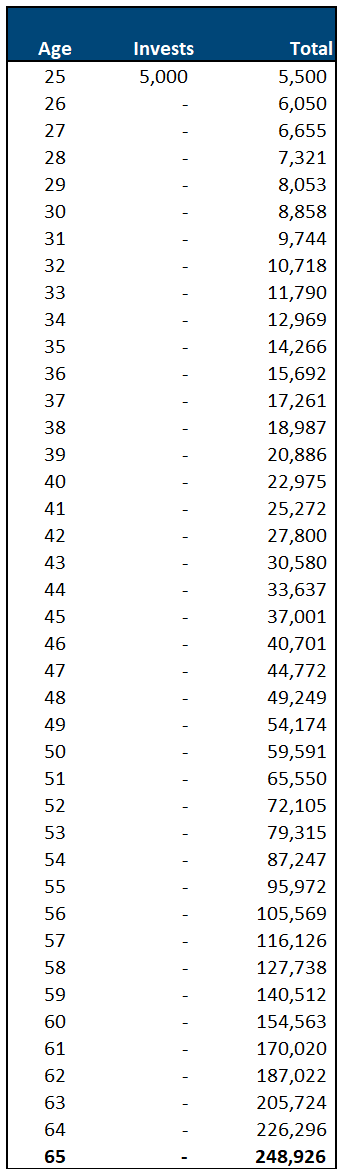

Going a little deeper, let’s assume you start investing at the age of 25. You open a brokerage account and invest $5,000 in a fund that mirrors the stock market’s performance. Each year (until you retire at 65), you invest another $5,000 in the same fund. By the time you retire, your portfolio could be worth over $2.6 million.

How? The market’s historical average annual return is approximately 10%. Over 40 years, annual contributions of $5,000 and a 10% annual growth rate result in a handsome seven-figure sum.

Here’s a year-by-year breakdown:

If you want to be more conservative and assume a 7% annual return, that still results in over $1.1 million after 40 years.

Now, before I move on, there are two things to keep in mind:

- That doesn’t mean your portfolio will increase by a clean 10% every year. The market is far more up-and-down. One year it could be up 33%, another it could be down 12%. The idea is that it has averaged out to ~10% each year since the 1920s. So, it’s “up” far more often than it is “down.”

- Past performance is not a sufficient indicator of future performance. Just because something happened doesn’t mean it’s going to continue happening.

Let’s start with the basics

People have written full-fledged books with multiple volumes about the stock market, investing, portfolio allocation, and much more. Simply put, this post couldn’t possibly cover everything. But I’d like to think it does a pretty good job of covering the fundamentals.

If I say so myself.

So, let’s start by answering a few basic investing questions to establish context.

What exactly is the stock market?

Without going too in-depth, here’s an overview of the stock market and how it works.

The stock market is a marketplace where you can buy shares of publicly-traded companies (like Apple or Microsoft). When you buy a share, you’re buying a sliver of ownership in a company. Like any marketplace, the stock market consists of buyers and sellers.

When investors buy and sell their shares, stock prices move. If tons of people start purchasing shares of Company A, the price of Company A is going to rise. If tons of people start selling shares of Company B, the price of Company B is going to fall.

The stock market consists of eleven sectors, such as information technology and energy. Here’s a list of all eleven sectors.

- Communication services

- Consumer discretionary

- Consumer staples

- Energy

- Financials

- Healthcare

- Industrials

- Information technology

- Materials

- Real estate

- Utilities

Each sector consists of several industries. For example, there are eleven industries within the consumer discretionary sector, such as automobiles and specialty retail. I won’t overload you with a long list of industries — but you can see a breakdown here.

To track the U.S. market’s performance, people use indexes like the Dow Jones Industrial Average (DJIA or “the Dow”) and the Standard & Poor 500 (“the S&P 500” or S&P). These indexes are hypothetical portfolios of the largest U.S. public companies.

So, if the S&P is up or down 2%, that’s being driven by the stock values of the 500 companies within the index.

What influences the stock market?

A lot of things influence the stock market, but if you want to sum it up with one word: information.

New information surfaces, investors react (buy, sell, or hold), and prices adjust accordingly.

Information is obviously a general term. New “information” could be a company’s performance report or the announcement of an acquisition. Or it could be broader — like the latest inflation rate…or a global pandemic. Here are several examples of economic indicators that affect the broader market, as opposed to a single company or industry.

- Job growth

- Consumer spending

- Housing sales

- Gross domestic product (essentially measures economic growth)

The 2020 global pandemic is a prime example of a market influencer. People are self-quarantining. Companies are either laying off large portions of their workforce or shutting down altogether. It’s forcing millions of people to file for unemployment. These reactions impact all of the above economic indicators — less job growth, less consumer spending, lower housing sales, lower GDP.

This ultimately led to a bear market, which means stocks fell by more than 20% off their recent highs.

Stock market news often includes references to bulls and bears. These animals are used to describe the current status and direction of the stock market. When the market is rising, it’s considered a bull market. And, as we stated, when the market falls by more than 20%, it’s considered a bear market.

Are there risks?

There are always risks with investments. Even Treasury Bills — which are deemed “risk-free” — carry a level of risk (it’s negligible, but technically risk exists).

Sure, it would take a monumental collapse of the U.S. government for that to take place. And if that happens, we would all have much bigger issues to worry about.

But, the point is, nothing is “risk-free.”

We’ll talk about this later, but that’s why it’s important to know and understand your risk tolerance (how much risk you’re willing to take). More risk, more reward. Less risk, less reward.

There’s an old investment question that captures the risk-return relationship: Would you rather eat well or sleep well?

In other words, are you going to stress out about your investments if they’re considered “riskier”? Then you should probably play it safer.

Do you need a lot of money to start investing?

Contrary to popular belief, you don’t need a lot of money to start investing. In fact, there are platforms out there that let you purchase fractions of shares.

For example, if you want to invest in Amazon — but don’t want to cough up a ton of money for a single share — you can buy a fraction of a share through platforms like Robinhood, Stockpile, and Stash.

Some platforms, accounts, and funds will have minimum investment requirements — but there are plenty of options that don’t. Companies like Fidelity, Ally, and TD Ameritrade offer brokerage accounts without account minimums or fee commissions (i.e. the amount you pay per stock trade).

But wait, the market is down, shouldn’t you wait?

First off, you cannot time the market. Waiting for the market to be at the right level is a waste of precious time.

Second, you should consider a down market to be an opportunity — not a warning sign. Remember buy low, sell high? That’s what the old adage refers to.

That doesn’t mean wait for a bear market to buy-in. It just means you can’t predict what’s going to happen (nobody can), so don’t avoid investing for that reason.

If you really want to reduce your risk of buying at the wrong time, you can ease into investing by making purchases in weekly or even monthly increments. Keep in mind that you could be limiting potential gains too (e.g. the market goes up while you’re gradually buying).

If you happen to start investing around a market correction or even a bear market, don’t panic. Historically, the market increases — and it’s not even close.

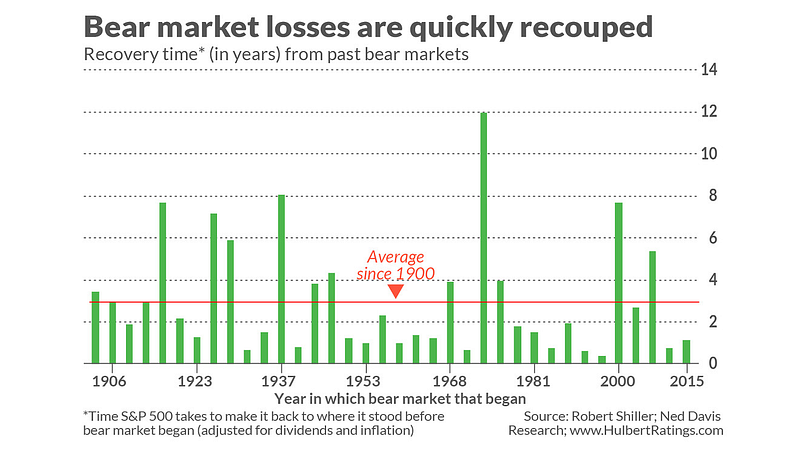

You might be wondering, “How long does it take for a bear market to recover?” That’s an excellent question.

The answer: three years, on average.

What kind of investor do you want to be?

Do you want to be a do-it-yourself investor or a laidback investor?

The DIY investor makes their own trades and takes full-responsibility for managing their portfolio. DIY investors stay updated on the market’s every move and do their own in-depth research into trends, funds, and stocks.

They’re trying to “beat the market” (i.e. outperform the S&P 500).

Laidback investors are more hands-off — but they still handle upfront research and portfolio allocation. Once they invest, they monitor every month or quarter. They don’t make a ton of trades, and they aren’t trying to beat the market. They also have long-term investment horizons.

Managing your investments is more time-consuming, but no one cares as much about your money as you do. Yep, that’s another investing adage.

But there’s a third option. If you don’t want to be responsible for picking and choosing investments, you can hire an advisor that will do the work for you (which comes with a price).

Like anything, financial advisory is a service that demands a fee. That doesn’t mean you’re relieved of your duty to monitor your investments from time-to-time, but the bulk of the work will be done by someone else.

For people who prefer to offload their investment decisions, the next step is choosing between a robo-advisor and a human advisor.

Robo-Advisors

Robo advisors have skyrocketed in popularity over the last few years. Robo advisors use sophisticated algorithms to create diversified investment portfolios.

These platforms tailor these portfolios to your personal preferences, such as your risk tolerance, desired returns, and investment horizon.

Wealthfront and Betterment are two of the most common robo-advisory platforms. For a detailed review and comparison of these platforms, check out this NerdWallet review.

While robo-advisors are generally cheaper than human advisors, these types of platforms only offer investment management services — not comprehensive financial planning.

Financial Advisors

Financial advisors offer a wider breadth of services compared to robo-advisors, including estate planning and retirement planning. They’re usually more expensive — but also more personalized.

Trusting someone with your money is hard, so I suggest tapping your family and network for advisor suggestions. Most financial advisors will offer free consultations, so you can use that time to feel them out and see if they’re a good fit for you.

Here’s a financial advisor that will connect with you free of charge.

What is your investment horizon?

Do not invest without your life goals in mind. You might not have these goals figured out, but it’s important to invest based on a timeline. Are you going to need these funds in one year? Three years? Ten years?

Your portfolio will look different based on your answer.

Why? Because if you’re pulling your money out in a year to buy a house, you’ll want to minimize your risk. Or else you’re susceptible to big market shifts that could spoil your home purchase.

You don’t want that kind of stress.

The opposite holds true too. If you don’t expect to need your investment funds for another 15 years, you can afford to take more risks.

What is your risk tolerance?

See, I hold true to my promises. Let’s talk more about risk.

Risk is more than just a board game or the decision path to a good story. Your risk tolerance is what it sounds like: your openness to risk. For investing, it’s your willingness to make and live with riskier investments.

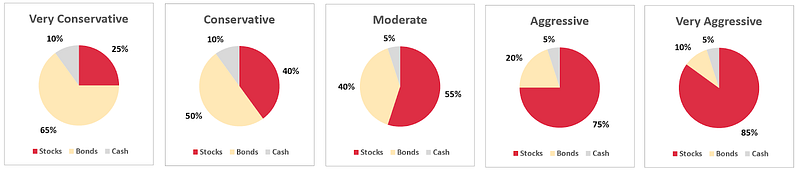

You can think of risk tolerance as a five-point scale:

- Very Conservative: risk isn’t your thing.

- Conservative: a little risk is okay.

- Moderate: some risk is okay.

- Aggressive: a lot of risk is okay.

- Very Aggressive: bring on the risk.

Risk tolerance is totally subjective. If taking risks makes you anxious, that’s totally fine. Being risk-averse isn’t a bad thing. The same goes for welcoming risk with open arms and a smile (so long as you don’t confuse “calculated decisions” with “mindless speculation”).

Speculation is pretty much like gambling. You throw your money at a hot stock with little to no research. I don’t recommend this approach. If you want to gamble, go to Vegas.

Your odds are better.

General wisdom suggests that younger people should be more tolerant of risk. Why? Because, in theory, there’s more time to recover from downturns and losses. In other words, a longer investment horizon affords you a larger cushion to take risks.

That doesn’t mean you have to be ultra-aggressive. You shouldn’t invest beyond your comfort zone. You know that saying, “step outside of your comfort zone”?

Yeah, don’t do that here.

In most people’s cases, investing is a long-term game, so there’s no reason to sacrifice your sanity and peace-of-mind.

Alongside your investment horizon, your risk tolerance will help you figure out how to construct your portfolio (also known as asset allocation). The typical portfolio is going to consist of three assets:

- Cash: the least risky, but lowest return.

- Bonds: riskier than cash (and a better average return), but not as risky as stocks.

- Stocks: the riskiest, but higher upside in terms of return.

The amounts you invest in each of these types will vary depending on your personal preferences. Here’s a graphic of possible asset allocations based on risk preferences.

For example, if your investment horizon is 10 years and you’re about a 3.5 on the risk scale, an “aggressive” asset allocation might make the most sense for you.

What is diversification?

If you’re going to invest, it’s important to understand the concept of diversification.

Ever heard the phrase, “Don’t put all your eggs in one basket”? That pretty much sums it up.

Diversification is the process of lowering risk by spreading out where you put your money. By diversifying your portfolio, you lessen the risk of any single stock tanking your overall return.

So, take the “Very Aggressive” asset allocation as an example. You wouldn’t want one stock to represent that 85% stock allocation. That would be an “undiversified” portfolio. In this situation, you’re totally susceptible to the ups and downs of that stock.

If it drops 10% after a bad earnings report, your portfolio drops 10% too. Undiversified portfolios are risky.

On the other hand, a diversified portfolio consists of anywhere from 15–30+ stocks. If one company has a bad year and tanks, your portfolio doesn’t feel as harsh of an impact.

Remember what we said about risk though? You can’t eliminate it altogether. But diversification helps minimize your risk.

What should you invest in?

There isn’t a one size fits all solution, unfortunately. Your investments should be tailored to your risk tolerance, desired return, and investment horizon.

That being said, unless you’re willing to commit hours of your time every week to researching and tracking, I don’t recommend hand-picking individual stocks. That’s much riskier and doesn’t guarantee a better return.

Even seasoned investors and funds fail to beat the market — and they have millions of dollars of resources at their disposal. Leave stock picking to avid investors.

Stick to exchange-traded funds (ETFs) and mutual funds. They make it much easier to diversify your portfolio.

When you buy a share of these types of funds, you’re buying a share of a portfolio of stocks. For instance, the SPDR S&P 500 Trust ETF (ticker: SPY) mirrors the movements of the S&P 500.

So, when you buy a share of SPY, you’re investing in the stocks within SPY’s portfolio.

Investment strategies

You shouldn’t start investing until you have a strategy. Together, your investment horizon and strategy keep you from straying down the wrong path and making a poor decision — such as buying a speculative stock or selling at the wrong time.

While there are numerous investing strategies, value investing and growth investing are two common ones.

Value investors focus on undervalued stocks. They operate on the belief that people are irrational at times, which leads to opportunities to find high-quality stocks at bargain prices.

Digging for value stocks requires hours of dedicated research. So, if you’re looking for value but don’t want to fish for stocks, you can invest in value ETFs and mutual funds.

Growth investors focus on stocks with large upsides. They aren’t concerned with mature companies that dish out healthy dividends. Instead, they’re trying to get in early before companies take off (like investing in Amazon or Apple before they boomed).

If you’re the kind of person who prefers a larger list of options to browse, here are comprehensive lists of value ETFs and growth ETFs (of course, there are blends of value/growth too).

Here’s a list of bond ETFs as well, so you can round out your asset allocation.

If you’re the kind of investor that wants a little guidance, you could look into funds that track the general market (like SPY) or start by looking at certain industries that look promising.

For instance, if you’re familiar with the biotech space and think it has a bright future — you could look into biotech ETFs or mutual funds.

If you want more guidance, I suggest speaking with an advisor.

Open a brokerage account

Thanks to the Internet, you can open a brokerage account in about 10 minutes.

There are tons of options — which, honestly, might be a little overwhelming. Nowadays, you can open a brokerage account for free and without a minimum deposit. Plus, you can avoid trading fees.

If you’re not partial to a company, to help you decide, here’s a NerdWallet review of 11 brokerage accounts.

I’ve experimented with a few, including Fidelity, Wells Fargo, Ally, Merrill Edge, and Wealthfront. Personally, I vouch for Fidelity, Ally, and Wealthfront.

But base your decision on your wants and needs.

Stay committed

The biggest hurdle between wannabe-investors and investors is starting — but it’s just as important to stay committed.

Even if you take the laidback or hands-off approach, you still need to schedule regular transfers from your checking/savings accounts to your brokerage account. Remember that table I showed you earlier? Annual $5,000 investments paired with a 10% return (or even 7%) can yield seven-figure results.

That pretty picture isn’t so pretty if you nix the annual investments. Here’s our example from earlier — but without yearly contributions.

That’s why you need to incorporate investing into your monthly routine.

Managing your personal finances takes time — which is frustrating because we don’t have a ton of free time. But, if you don’t commit to saving and investing, financial stability and wealth will elude you.

Our world is becoming more automated and user-friendly, so quit making excuses — organize your finances, clean up your budget, build an emergency fund, and start investing.

Want to calculate how much your portfolio could be worth in five years? Ten years? By retirement? Sign up for the Bits newsletter to receive a free Compound Interest Calculator in excel.

Disclaimer: The information in this post should not be misconstrued as investment advice. Under no circumstances does this information represent a recommendation to buy or sell certain securities. Although I write about personal finance, I am not a financial advisor. If you need personalized financial advice, I recommend speaking with a certified advisor.

In other words, do your own research and please don’t sue me.