Go on Living Sprees, Not Spending Sprees

Think of all the things you can do when you have money left over every month

In a recent Making of a Millionaire article, I did the basic math on buying a $1.3 million home in Los Angeles on monthly take-home pay of $10,000.

I imagined going from my $1,342 a month rent payment in the same neighborhood as this actual $1.3 million house for sale to the roughly $6,000 a month mortgage payment it would take to “own” this home. I won’t even include the approximately $264,000 down payment in our discussion.

In this article, we consider how you can control how much money you have left over at the end of the month and the things you can do — other than service a mortgage — with the excess cash.

Let’s go with my actual cost of living, putting it on the high side at $3,000 a month. This includes my current $1,342 rent payment. If I’m taking home $10,000 a month, this leaves $7,000 left over at the end of the month.

I could funnel that cash into a savings account for a down payment on the aforementioned house. It would take me just under three years to accumulate the $264,000 down payment I said I wouldn’t include in our discussion. Sorry, but it’s difficult to remove this element from the equation.

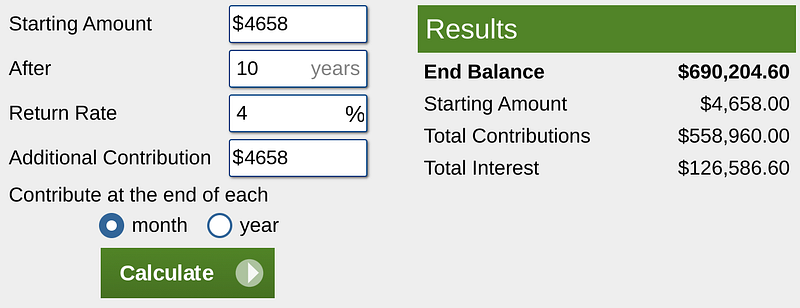

Anyhow, let’s say I buy the house. The $264,000 miraculously fell from a tree, but only let me pick it up if I agreed to make it a 20% down payment on a $1.3 million house. From here, I take on the $6,000 monthly mortgage obligation, increasing my $1,342 housing payment by $4,658. This is $4,658 I could spend elsewhere that I’ll be spending on a mortgage.

Am I making a value judgment here? Yeah, I am. It’s sort of tough not to when you do some math and run potential budget scenarios.

Forget anything beyond the $4,658 difference between renting and owning.

If I do nothing with this $4,658 savings on housing other than straight up save it, I will amass $167,688 in just three years. In ten years, I’d have $558,960. Rack the latter number up alongside a mere 4% interest, and we’re looking at:

Calculate our returns at the more often-cited 8%, and we approach $850,000.

I require no further convincing.

For me, it begins and ends with cash security. On a relatively modest salary, there’s no choice to make here. Maybe I’m running with an abnormally high aversion to risk, but I’m not taking any chances sinking nearly five grand into a mortgage when I can put it in the bank and/or stocks. I’d rather ride the gravy train to a relatively quick six figures than pay more for housing than I absolutely need to or consider otherwise reasonable.

However, for the fun of it, let’s think of other ways I could allocate $4,658.

Let’s go on a living spree.

$4,658 — scenario one:

- Direct $1,000 a month to your various pots of money.

- Invest $1,000 a month.

- Spend $1,000 a month.

- Give $1,000 a month to your kid.

- Give $658 a month to charity.

$4,658 — scenario two:

- Direct $500 a month to your various pots of money.

- Invest $1,000 a month.

- Have a sick, all-out, and I’m going all-in $500 dinner once a month.

- Put $2,658 a month into a savings or investment account until you have enough to buy a rental property that yields 8%.

$4,658 — scenario three:

- Create your own scenario.

If deciding how to allocate an extra $4,658 every month isn’t financial flexibility in and of itself, you’re definitely on the right freeway to get there. What an incredibly great and encouraging problem to have.

I don’t know what the number is. And it’ll be different for everyone on the basis of personal preference and cost of living in their chosen city/environment. But there’s a number we all have at which we would consider ourselves cash secure and headed toward financial flexibility. An amount of cash we can do whatever we want with every month.

In a situation where you make $10,000 a month, a number like $4,658 matters quite a lot. At least it does to me. You might be like:

I don’t want a cushion. I don’t care about cash security. I’ll save money when I’m dead. I’m buying a Tesla and spending whatever I have left on whatever I want.

If you’re making $50,000 a month, things change. You could literally burn $5,000 a month (in an actual flame), save enough to achieve cash security, and still have loads of money left over to allocate however you’d like.

Or you could increase your cost of living — lifestyle inflation — and be in the same boat as the person making $10,000 a month. There are probably people who make $5,000 a month but live so frugally they’re better off than their $10,000 or even $50,000 a month counterparts. Maybe you’re one of these people.

Clearly, it comes back to personal preference. But only to a certain extent.

I go through exercises like this not to prescribe my beliefs to you (though I do try to gently persuade!), but to get the wheels turning. Because, as much as personal preference plays a key role in how people budget and determine what their “number” is, it doesn’t explain all of the variations. I’m confident we can explain some of the differences between people through what I’ll call going through the motions.

In other words, some people don’t have a preference in the matter. They haven’t thought about it. They haven’t done the intellectual and psycho-emotional work. They stand for nothing from a personal finance perspective.

They take in money every month. Maybe a lot of it. From there, they have no plan. You might be able to relate. Your personal finance plan is literally garbage in, garbage out — every thirty days.

I know so many people like this. For fuck sake, I used to be like this. I’d be like:

Okay, I make $3,878.43 after taxes every month so I can spend $1,800 a rent, $500 a car, let the credit card minimums total another $500 a month, and use the leftover $1,078.43 on whatever my monthly spending spree ends ups looking like.

The spending sprees end up not feeling like actual spending sprees because they span thirty days, and you go through the same patterns every month. Isn’t this the definition of going through the motions? You engage in something so thoughtlessly that it becomes the uncritical, barely productive, and potentially destructive norm.

Not a good way to live. Take it from someone who has been there, done that.

Fitting a lifestyle into an amount of cash as opposed to letting your cash dictate your lifestyle.

When you practice the former style of personal finance, you take what you make and cram a bunch of expenses — some fixed, some discretionary — into your monthly cash flow, to the dollar.

When you practice the latter style of personal finance, you begin with the bare minimum. Relatively low housing payment. Modest monthly transportation costs (i.e., you don’t have a car or you drive one that’s less expensive than you can afford). The flavor of frugality we often talk about together. From there, you see how much money you have left each month and spend/allocate it accordingly.

Maybe you need a getaway. So one month, you decide to go big and drop $2,000 on a nice trip up the coast. In another month, you’re busy but perfectly content, so you literally put every dollar you have left into savings and investments. At some other juncture, you fall somewhere in between. You save and invest a little less and spend a little more, though not quite the $2,000 you dropped for your coastal respite.

You have given yourself the financial flexibility to make these choices every thirty days because you’re not tied to out-sized monthly obligations or running on very little breathing room between income and expenses.

While one size absolutely does not fit all, and we need every possible case to comprise a sample we can all learn and draw conclusions from, I gotta say there’s something to be said about making your budget base case as low as humanly possible. You can always go up from there. It’s easier than coming down when your expenses outpace your income.

Think about it. This strategy allows you to go on a living spree most months, if not every month. It beats the hell out of spending sprees and ultimately stressing over how you’re going to pay for them. The latter often leads to credit card debt and attendant financial impotence, and cash insecurity.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Consult a financial professional before making any major financial decisions.