The Ridiculously High Cost of Home Ownership in a Big City

It comes down to simple math. Most of us probably shouldn’t buy a house in Los Angeles.

I was walking to my car the other day.

From my $1,342 a month studio apartment — built in 1924 — through the 42 homes — built between 1911 and 1926 — that populate the Melrose Hill historic preservation district in Los Angeles.

There’s another house for sale. The third in the last year or so by my count. Not the norm for a neighborhood where people apparently don’t move.

I’m curious by nature, so I looked up the listing.

It’s a four-bedroom, two-bath, 2,000 square feet “2-story home, built-in 1917 just waiting to be brought back to its original beauty.” This indicates the house needs work. Relative to the other houses in the district, this appears true. While it’s not in bad visible shape, this house certainly isn’t as cosmetically well put together as most of the other classic LA homes lining the three blocks that compose Melrose Hill.

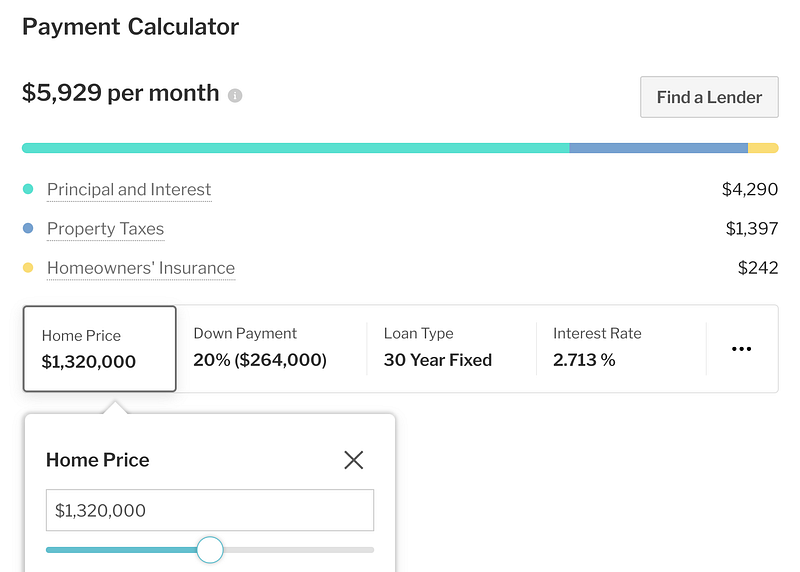

If you would like to “own” it, here’s what your mortgage might look like:

When I look at these numbers, I wonder how the rent versus own debate even exists in some contexts. It’s an almost objective fact that, even if you make fantastic money, you’d be stretching yourself to get into this mortgage, let alone afford to maintain it.

Let’s say you’re clearing $10,000 a month. You make $120,000 a year after tax. That’s good money, like around $200,000 a year before taxes. Even at that income level, it’s a financially questionable move to commit to this mortgage.

As we run the basic math, I’m purposely ignoring the personal finance tenet of you should spend 28% of your gross monthly income on your mortgage. It means absolutely nothing on the ground.

Before we even freak out over the monthly payment, we need $264,000 for a down payment.

I should end the article right here.

If somebody gave you $264,000 tomorrow, would you be ready to immediately spend it for the right to subsequently drop $5,929 a month, every month, on a mortgage?

If you scrimped and saved for years, would you trade the cash secure position $264,000 would put you in for the right to subsequently spend $5,929 a month, every month, on a mortgage?

For those of us who think $264,000 is a lot of money, these feel like questions with easy answers. As I noted in a recent Making of a Millionaire article on the subject:

The thought of saving that much money, then turning around and spending it absolutely, unequivocally terrifies me.

But let’s set the quarter of a million-dollar down payment aside for a second.

You take home $10,000 a month. You’re on the hook for 60 percent of that every month. For thirty years. This leaves you with $4,000 left over each month.

Then there’s maintenance (we won’t even get into the cosmetic and other repairs this house likely requires right away).

If you follow the 1 percent rule, you’ll need to set $1,083 aside each month for maintenance. That’s 1 percent of the value of your home. Now you’re down to $2,900 left over each month to pay for your car (presumably), food, other fixed expenses, discretionary spending, saving (for purposes other than expected and unexpected home maintenance), and investing.

This back of the envelope exercise on the cost of home ownership in a big city terrifies me. Spending $264,000 ahead of having to come up with $6,000 a month to service a mortgage should frighten anyone who believes in sound and secure personal finance.

While I’m all for individuals and couples doing what they want and what’s right for them with their money, I cringe at the thought of people without relatively endless resources taking on such a hardcore financial obligation.

Alternatives to the scenario I illustrate exist. No doubt. However, they require significant sacrifices (or compromises), all in the name of chasing home ownership.

Buy something less expensive. Get a condo (and the associated HOA fees). Move to a less desirable neighborhood — maybe in the suburbs.

This is where we get into the toxic psychology of the American dream. Countless numbers of people go from the home and neighborhood they really want to whatever they’re willing to settle for in the name of achieving homeowner status. We see it happen on every episode of House Hunters we binge. The American dream says home ownership means:

- You made it.

- You’ll receive tax benefits.

- You’re making a smart investment in your future.

It all sounds so nice on paper. Sort of like Trump making his ardent followers believe the election was rigged. They want to believe it. So they do. And they burn our society down with their ill cognitive inclinations. Nevertheless, I won’t persist. Instead, I digress.

Tax time comes once a year. Paying interest on a mortgage reduces your tax liability and maybe even gets you some money back around April. This does very little as you work to make ends meet the other 11 months of the year. Run the math. Proponents of home ownership often overstate the tax benefits and downplay day-to-day budgeting realities.

And, of course, you’re living in your “investment” because you need a place to dwell. Your home ceases to be a meaningful investment until you sell it and (presumably/hopefully) take profits. Then you run into the problem of still needing some place to live. This transition costs money, too. The extra cash you’re spending to own a home could just as well (or better) go into liquid savings and, not-as-liquid, though still more liquid than a mortgage, compounding investments.

Granted, this is merely the math around buying something that costs about a million bucks.

Here again, this might work for you. It might work for people you know and love. I could probably even figure out a way to make it work for me.

I’m not here to wholesale banish home ownership in the name of personal finance dogma.

But I am here to say we need to tip the scales away from trying to maneuver our relatively modest salaries to fit the runaway American dream. I’d rather err on the side of renting as to increase disposable income we decide we’re not going to dispose of. We’re going to use our ample cash surplus at the end of each month to fund the modern-day version of the American dream — cash security closely followed by financial flexibility or freedom.

We’re gonna go on a living spree, not a spending spree.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.