My Battle Against the Soul-Crushing Costs of (Decent) Childcare

How my unborn baby’s future daycare is killing my budget.

Last updated: May 9, 2022

I’m going to say something that you already know.

Child care is expensive.

Super expensive.

Like sending your kid to college or paying a second mortgage expensive.

Now that the obvious is out of the way, I’m going to say something that you might not know.

Many parents have no idea how they’re going to pay for child care until the first day of child care. The bill comes, and they have to take it out of savings, or worse, use a high-interest credit card.

And we all know, deep down inside, that we are worse parents when we are stressed, especially about money.

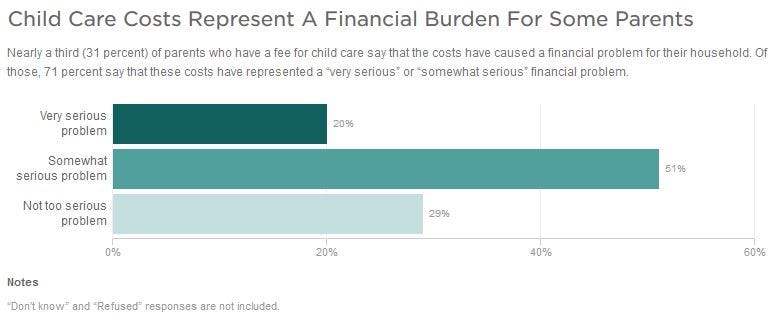

I am super guilty of this, but I am not alone. Check out the chart below from an article on the burden of child care.

So how do we head off the debt and guilt that we may think is inevitable?

The same way we attack any large financial goal: one step at a time.

Before I start, I will say that, overall, my family is pretty lucky with our current pregnancy. You’ll see why in the subsequent paragraphs.

That being said, we have also been unlucky, with my wife only having 7 days at home with our first child before heading back to work due to medical complications.

Everyone’s story is different, and I wholly realize that. This is our story, and my hope is that it might spark a few ideas to help you prepare for yours.

As with any story, there is good news and bad news. I’ll start with the happy stuff.

The Good News

Our current pregnancy is a case study in fortuitous timing.

Our new baby is due in late February. My wife’s employer allows 8 weeks off for medical recovery of birth, followed by 4 weeks of parental leave. This is 3 months of child care provided by us, which will push us to mid-May.

By sheer coincidence, my wife’s job duties end in mid-May, as she works for a local university. She won’t go back to work until August 3, which gives us another 2.5 months without daycare.

The last little bit is that I have 6 weeks of parental leave through my employer. I’ll use the first 3 weeks right after the birth and the second 3 weeks to bridge the gap between August 1 and the start of the school year for our older child.

So, we have a start date for new child care August 24. That is just over 7 months away.

The Bad News

As I said, the timing could hardly be more perfect, and we are ever so grateful for it. The downside is that any child care facility in our area worth its salt costs about $50/day.

(Check out this map for average child care costs by state.)

As I alluded to earlier, our budget is pretty much maxed out. Sure, there is a little room for savings, but not $50/day worth of room.

Before we were expecting, we were doing okay with a family of three. We were saving cash for annual expenses (e.g. car registration) and socking a little away for retirement.

Over the long term, we were working on our careers, planning on raises and promotions to provide the bulk of our retirement and college funding, as we are both in our thirties and not even in our peak earning years.

We also have a few large debt payments that will start to fall off in the coming year (two car payments and two student loan payments).

However, with the new baby, there is an immediate financial need that we currently can’t meet. We don’t have time to play the long game, and the gaping hole in our budget is looming large over our heads.

The Goal

Most goals start with a number. Ours is $50/day. That’s $250/week, $1,000/month, or $5,000 through the rest of 2020.

To put it in salary terms, we need $6.25/hour (post-tax) added to our income. Given our marginal tax bracket is 22%, this comes out to $8.00/hour extra.

Put another way, we need to have a third person in our family working full-time at above minimum wage just to cover child care. Oh, and that person can’t incur any other expenses, like, you know, food.

So where do we find this money?

Well, there are only two ways to come up with new money. We can either cut costs on things we already spend money on, or we can find additional sources of income. Let’s dive into both of those.

Reduce Expenses

This is not the “frugal living” section of the article, just a few things that we can do over the next year to help redistribute the money we have coming in.

Student Loan Payments

If you have federal student loans and are on one of the Income-Drive Repayment (IDR) plans, you can claim your unborn baby in the year it is scheduled to be born. Per studentaid.gov

Family size always includes you and your children (including unborn children who will be born during the year for which you certify your family size), if the children will receive more than half their support from you.

Our baby is due in February, so we missed out on the majority of the pre-birth benefit. But we can still update our family size in early January to get the most out it. This gives us $55/month in savings.

Medical Expenses

In Let’s Do the Math: Health Insurance, I went through the entire process of how to calculate the full cost of health insurance for the year. After running the numbers, we switched plans and will save a little over $2,000 this year, or $165/month.

Also in the article, I wrote about saving up for medical expenses that were above and beyond what the tax-advantaged accounts (FSA or HSA) could cover. After using the full pre-tax FSA amount of $2,650 in 2019, we only had about $400 in post-tax health fees this year. This allows the remaining $1,200 we had saved to roll over to next year.

We only need to save an additional $250 this year, so we save $75/month towards child care.

Savings Falling Off

There were two savings goals that we met in 2019 that will no be replaced in 2020.

The first was saving up for a professional family photoshoot. We start saving $50/month in springtime so we could get the shoot done in late fall. While we met the goal and are now putting the money toward saving for childcare, the photo shoot is postponed until the baby arrives.

The second was for a television. We sold our only TV in the summer of 2018. We found that it was becoming more of a time-suck than anything, so we pulled a page from Dave Ramsey’s book and “blew up the log jam.”

It was great not having a TV and taught us a lot about being mindful of our time together. After the first year, we decided to save up for a new TV for Christmastime. We met that goal and can now direct another $40/month towards child care.

Food

I’m not sure where your family stands, but my family and I love food.

Trying new recipes. Remembering old recipes. It’s all great. The costs, however, can start to creep higher and higher if you’re not mindful of your spending.

Partly due to using YNAB and partly due to focusing on standardizing our meal plan, we have whittled away at our monthly food budget to the tune of $150/month. We could probably add another $50/month by cutting back a bit more, and all of that can be redirect toward child care.

The only caveat is that our budget will start to creep up once the baby is weaned and starts eating real food.

Mitigate New Costs

Avoiding new expenses is a variant of cutting costs, as you aren’t currently spending any money right now. However, it’s money that you plan on spending, so the funds have to come from somewhere. If you can mitigate enough future spending, the money that would have been used can be redirected.

Baby Food

My wife is breastfeeding the baby for as long as possible, so that will cut down on formula and other associated feeding costs.

Diapers

We are reusing the cloth diapers that our first child used. Our water bill will no doubt increase due to the additional washing, but that is negligible compared to the cost of disposables.

Increase Income

While cutting expenses is all well and good, there is only so much “extra” money you can find in your budget. There is an ultimate limit to what we can save.

On the other hand, increasing our income is theoretically limitless.

Salary Increases

As I mentioned earlier, we were planning on following the standard career arc of raises and promotions to achieve our financial goals. While that plan is out the window, it doesn’t mean that raises and promotions won’t help in the near term.

My standard raise in January comes out to $1,050 post-tax. I am also getting a new professional certification in March, so that should boost my salary quite a bit more in 2021.

My wife gets her raise in August when the new school year starts. That adds an additional $850 post-tax.

A total increase in take-home pay of $1,900/year doesn’t seem like much, because it really isn’t. But it adds almost $160 every month towards our $1,000/month goal. Nothing to sneeze at.

Side Hustles

There are several great books about starting your own side hustle or creating passive income, along with quite a few good websites.

There are also way too many sources spouting way too much BS about these same subjects, so be careful whose advice you follow.

Writing

I am currently making about $10/day with my writing, or $300/month. It won’t make us millionaires, but it will contribute to our child care costs, which is my immediate need.

Selling Stuff

We are aspiring minimalists, so we don’t have much to sell. We did have some moderate success flipping Kinderpacks a few years ago, but that particular market has started to saturate, making it unprofitable.

The Takeaway

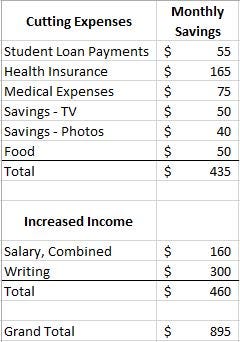

The result of cutting costs and increasing our income is that we can find $895/month to cover child care. We are still short $105/month in 2020, and who knows about 2021.

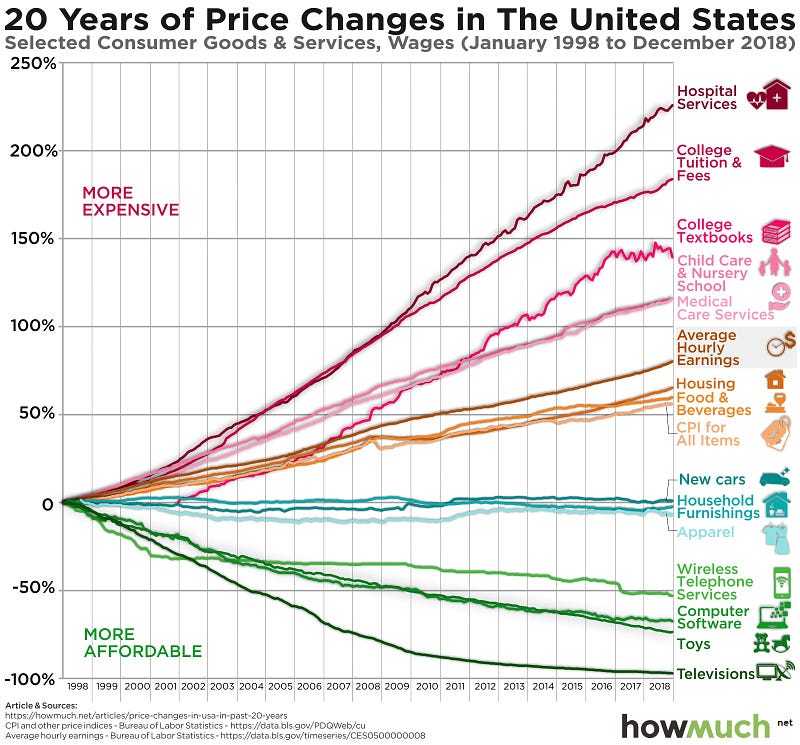

The biggest problem, aside from not even hitting our goal, is that everything keeps on getting more expensive, including the very same child care that we are working to afford. Just take a look at the chart below.

Given our current situation and the prospect of ever-increasing costs, our financial future looks dire, even with all the finagling I just described.

What strategies have you used to pay for child care (or any other living expense, really)?

Did you focus on bringing in more money or decreasing your existing expenses?