Let’s Do The Math: Health Insurance

How to save thousands. Every. Single. Year.

Last updated: May 9, 2022

When is the last time you actually looked at your health insurance plans?

- A life-changing event? Unlikely.

- Annual open enrollment? Maybe.

- First week on the job? Probably.

If you are like most people, you spend less than 30 minutes reviewing your health insurance options, then probably just pick the one with the lowest premiums.

What if I told you that by spending just a little extra time, you could knock off hundreds or even thousands of dollars.

Not just this year.

Every. Single. Year.

Health Insurance is Hard on Purpose

Listen. Health insurance sucks.

You know it.

I know it.

We all know it.

Policies are expensive. Medical bills come months after procedures. And there’s an ever-changing list of what is (not) covered.

The national problems with healthcare mimic many of the issues with student loans.

This is by design.

Insurance companies haven’t turned record profits by offering clear, concise, low-cost plans to everyone. (Cigna, Humana, and Anthem have all posted $1 billion profits in 2019.)

So, how do we cope with the labyrinth that is health insurance? I suggest following this tried and true advice.

Hope for the best. Prepare for the worst.

Always assume the worst will happen and you will meet every payable limit in the calendar year. Then you can work backwards to find out just how much you need to save to pay off any healthcare bills you have.

Before we get to the numbers, though, we need to understand the various sources of health insurance fees, of which there are three main categories.

- The price of the policy, as priced by insurance premiums

- The cost of healthcare that is not covered by the policy (i.e., the deductible and other out-of-pocket costs).

- The taxes you pay on your earnings before paying for healthcare.

Insurance Premiums

Insurance premiums are probably the most well understood and calculated cost of health coverage.

In short, they are the annual cost of your healthcare police. It’s similar to when you pay for car insurance every month.

When you look at the total price, you begin to realize insurance policies are not cheap. Multiply your premiums by the number of annual paychecks, and you’ll see that insurance is actually quite expensive.

For 2019, my family’s insurance policy costs $129 twice monthly, or $3,096 annually. And this is one of the cheapest plans we’ve been on in the past 10 years.

Because they are easy to understand, insurance premiums are where many people stop calculating their annual costs and just choose the cheapest option.

This is what gets them into trouble when something happens later in the year.

Out-Of-Pocket Expenses

If premiums are easily understood, the out-of-pocket (OOP) expenses are probably the least understood. There are two main categories of OOP expenses; the deductible and the annual out-of-pocket maximum.

Caveat: Most insurance companies have different levels for the deductible and OOP maximum depending on whether you use in-network or out-of-network providers. For the rest of the article, I am going to assume in-network costs.

Deductible

This is the amount that you must pay before any insurance benefits kick in. Deductibles can be as low as $500 or as high as $5,000, depending on the overall plan.

If you are single, then the deductible is pretty straightforward. If you are married or have a family, you need to be aware of what type of deductible is in your plan.

An individual deductible is one where each person has to meet a certain threshold before the higher-level benefits kick in.

A true family deductible is one where all costs for the entire family apply to the deductible, regardless of who incurred the costs.

Annual Out-Of-Pocket Maximum

As mentioned above, once you meet your deductible, insurance will start to pay a percent of your medical expenses. In many cases, this is around 80%.

You still have to pay 20% of any expenses (you coinsurance), but only up to a certain point. This point is your OOP maximum.

Many people think they only need to care about the deductible. Please don’t make this mistake. OOP maximums are normally much higher than the deductible, and could cost you even more.

Other Expenses

Copays

These are a nefarious part of any health insurance plan. Most times, copays do not apply to the deductible, but rather to the OOP maximum.

This is a sneaky, underhanded way for the insurance companies to maximize their profits. You see, most patients don’t meet their full deductible every year, and almost no one goes to their OOP maximum.

So, if you are the average insured employee, the companies can charge you 100% of your deductible for medical procedures, and still collect 100% of your copays.

But, like I’ve said earlier, if you plan for the worst (which is paying your full OOP max every year), then the copays won’t eat into your other finances.

Prescriptions

Similar to copays, prescriptions may or may not apply to your deductible. They may also have a percentage of coinsurance you need to pay or a flat fee structure.

Regardless, most every plan has tiers of prescription drugs, with Tier 1 (the generics) being the cheapest, and thus preferred by the insurance companies, and Tier 4 (the specialties) being the most expensive.

If you have any regularly prescribed medicines, you need to be aware of the prescription structures and costs.

Health Supplies

Unless prescribed, health supplies apply to neither your deductible nor your OOP maximum. Many can be bought with a tax-advantaged account, but these will still be in addition to your insurance.

Examples of covered health supplies might include a cane (prescribed after a fall) or a blood pressure cuff (prescribed after starting on new medication).

Tax Burden

Taxes are part of any financial conversation, and health insurance is no different.

Fortunately, just about every employer-sponsored health insurance plan can be paid for with pre-tax dollars. This means that every gross dollar you earn to pay for insurance is used towards that payment.

Unfortunately, everything else is paid for with post-tax dollars. That means that you have to earn more than the cost of your deductible and OOP maximum in order to afford them.

For instance, say you have a $2,000 deductible. At a 20% tax bracket, you will need to earn $2,500 to cover those costs. That brings us to our next topic.

Mitigation Strategies

Over the years, there have been several mechanisms developed that help people save money on their health insurance. Most of these use a special savings account that can be funded with pre-tax money but only used for health expenses.

Flexible Spending Account (FSA)

This is probably the most common way to save money on health insurance and other healthcare costs. The FSA can be funded with pre-tax dollars, which can then be used for a wide variety of healthcare costs. This includes deductibles, OOP costs, prescriptions, and even over-the-counter items. The list goes on. The FSA cannot, however, be used to pay for your insurance premiums.

There are some drawbacks to the FSA, though. The limit for 2020 is only $2,750, so it probably won’t cover all of your expenses.

Additionally, the FSA is a use-it-or-lose-it deal, with only $500 allowed for rollover to the next year. You need to accurately plan on what your health costs will be over the course of the year if you want to use the FSA option.

Health Savings Account (HSA)

The HSA is similar to the FSA, in that it is funded with pre-tax dollars and only used for healthcare costs. And also like the FSA, it cannot be used to pay for your policy premiums.

The similarities end there, as the HSA is a much more powerful option than the FSA.

The main difference is that the HSA can roll over into the next year, regardless of the amount left on it. With a 2020 limit of $3,550 for an individual ($7,100 for a family), you can literally save thousands of dollars to cover next year’s expenses.

The reason for the much higher HSA limit is that it can only be used in high-deductible health plans (HDHP). As you might have guessed, these plans have much higher deductibles than the standard Preferred Provider Organization (PPO) or Health Maintenance Organization (HMO) plans.

As a reward for taking on this risk, the health insurance companies offer a much lower premium. We’ll go through the math at the end of this article.

The other big draw of the HSA is it has a triple-tax-advantage.

- Funds are added pre-tax.

- Funds can be invested and grow tax-free.

- Funds used for healthcare costs are distributed tax-free.

This last one is huge for those close to retirement, as healthcare costs increase exponentially as you age.

Employer Contributions

Your employer offers multiple benefits that can increase your take home pay and/or decrease your expenses. Here are a few examples related to health insurance.

Health Account Contributions

Many employers will contribute money towards your health spending account if you choose a high-deductible plan. This can from $250 for a single plan up to $1,000 for a family plan.

Depending on the plan, the contribution can go toward either a Health Reimbursement Account (HRA) or a standard HSA.

Companies provide these incentives because their costs of the high-deductible plans are much cheaper than the low-deductible plans. While the contribution may feel like you’re being bribed, you just need to do the math to see if that’s the case.

Wellness Programs

Many companies have instituted wellness programs for their employees, with participation resulting in a reduced premium. These can range from a simple annual checkup to a year-long health monitoring program. I have been part of both, and the more complex the program, the bigger the discount.

Spousal Insurance Penalty/Incentive

If your spouse is offered insurance, it is common for employers to add a surcharge to your health insurance. The logic is that you should take someone else’s insurance, thereby lowering the cost of your company’s insurance costs. They disincentive you from using the program you are offered.

Some companies go even further. Not only do they charge a penalty, they will actually pay you outright not to take their insurance, which is exactly what happened to me.

In late 2018, my wife found a job with excellent insurance, but we stuck with mine through the end of the year so that we wouldn’t be exposed to a brand-new deductible. Because of that, I had a $35 bi-monthly penalty added to my insurance premiums.

In 2019, we switched to my wife’s insurance. Not only did the $35 penalty go away, I was then rewarded with a $65 bi-monthly incentive for not taking my company’s insurance. This one switch lowered our healthcare costs by $200 every month, or $2,600/year.

Granted, we have to pay taxes on the $65, but it’s not a bad income swing given our current insurance plan costs just over $3,000.

Putting It All Together

Now that we have all of the parts of health insurance laid out, let’s start adding everything up. For this example, I will use my 2020 insurance information for a family of 3.

We are offered three different plans.

- HDHP with HSA

- Standard PPO

- HDHP with HRA

There is an option for a wellness program, plus employer contributions for both HDHPs.

So, let’s do the math.

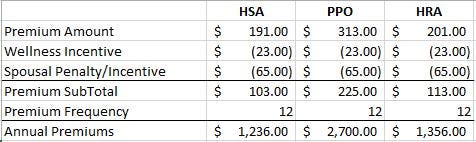

Below is the table showing the insurance premiums and any incentives or penalties incurred.

So far, the HSA plan is the cheapest, followed closely by the HRA plan. That’s to be expected, given that HDHPs have super low premiums.

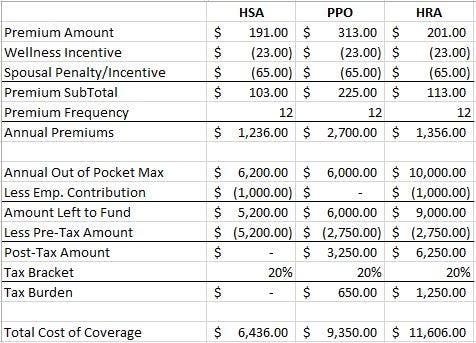

Next, let’s look at how much is not covered by the policy while subtracting any employer contributions.

The HSA is still coming out on top, but this time, the PPO is running a close second.

Now we need to see how much of that OOP maximum we can fund with a tax-advantaged account. We can use the higher HSA with the first plan, but the other two can only employ the lower, use-it-or-lose-it FSA.

Given that the HSA limit for a family is $7,100, which is well over the $5,200 required for this year, we will only put in what is necessary for 2020.

Lastly, we have the tax burden of any health cost exposure. Assuming a 20% tax bracket, the different plans pan out as follows.

Putting it all together looks like this.

The total cost of coverage is the sum of the annual premiums, OOP maximum, and tax burden, but less the employer contribution.

In this case, the HSA plan wins hands down.

Given that we are having a baby in 2020, we will definitely meet all the expenses of this plan, and then some. If we were smart, we would fund our HSA more than is necessary and have that roll over to next year, and the next, and the next, using it as a retirement vehicle for the next few decades.

I encourage you to use these calculations when figuring out which health insurance plan to choose. The monthly dollars may not seem like much, but over the course of a year, across all the categories of cost, the savings could be in the thousands.

My family is lucky that healthcare only costs 7% of our annual income, but that doesn’t mean we can’t work to save more.