Ask The Matadore: “Fuck! I Think We Are Getting Ripped Off!”

“We have done a really good job saving money with the guidance of an advisor. We have a 401(k) through my work, an Employee Stock Plan which is granted to me, a Rollover IRA, and 429s for our kids. However, a family member keeps telling me to dump our whole life policies ($95 in total monthly premiums for two, $100k benefit which we set up in 2013), and freaked out when I told him my rollover IRA is with Mass Mutual. The money is all invested in Capital Group mutual funds like RNWBX with over 1% management fees. When I recently logged in I saw over $1,200 in fees on the portfolio just for the year so far. This family member tells me to liquidate the portfolio, move it to Schwab, and dump my advisor. Are we getting ripped off?!”.

The financial services world is full of sharks, shysters, leeches, and insurance salesman pretending to be financial advisors. I think you found one of the latter! Sadly, there is no shortage of financial predators preying on ignorance and people looking to off-load decision-making.

In short, yes, you are getting ripped off. But, let’s take a look at a couple of pieces so you can see how, as it’s unfortunately in more ways than one.

Starting with the whole life. I don’t know the purported reason or “wisdom” behind spending $95 a month for just $200,000 in total death benefit, but there is no more expensive life insurance than whole life. My wife and I personally spend well under $100 a month total for over $2.5 million in total term coverage.

Whole life policies make your “financial advisor” rich with fat commissions. Often the cash value component is sold as an investment vehicle, but few people can benefit from whole life insurance, and your premiums clearly aren’t overfunding the policy.

Here is the real problem.

Since 2013, $95 a month, invested in VOO (the Vanguard S&P 500 ETF) would today be worth about $47,090 (as of today’s writing). That is based on the historical, annual return of about 11.7% with a 1.59% dividend reinvested.

I would guess that you instead have maybe $10,000 in cash value between the two policies, if you’re lucky. The $47,000 potential investment value is nearly 25% of the death benefit for the two policies combined. And you wouldn’t have to die to use it!

Whole life is how the middle class gets ripped off!

The Matadore’s recommendation: Close both policies (assuming you have term insurance already secured) immediately, and use the cash value to pay off debt or fund a ROTH IRA or brokerage account.

Now, regarding your IRA…

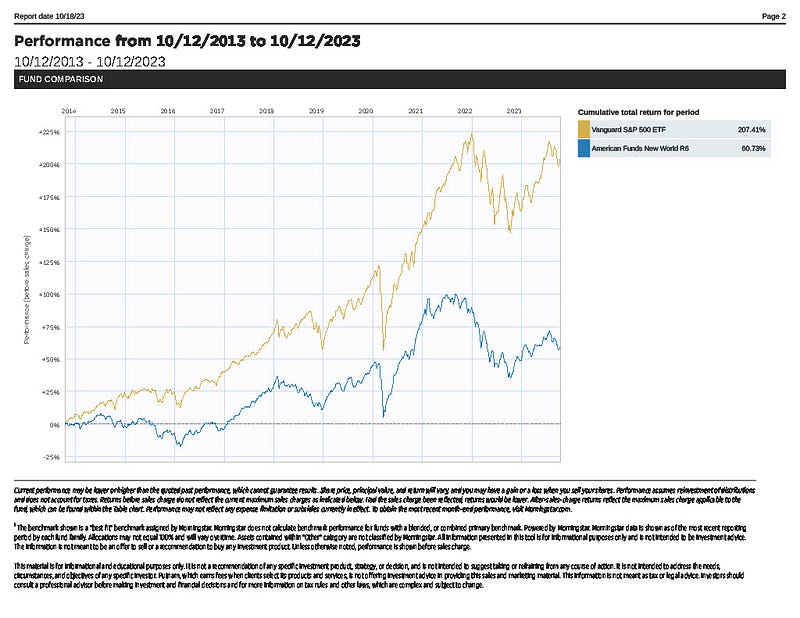

Let’s compare just your RNWBX (American Funds New World Fund) portion of your rollover IRA with Mass Mutual with the aforementioned VOO.

I will model it based on 10 years from the dates you offered on the whole life policies.

Yikes! As you can see, VOO returned over 200% in that timeframe, as opposed to 60% for RNWBX. But that’s not all.

Fees to own VOO are just .03%. Compare that with 1.70% on RNWBX.

That is over 55x more expensive for less than half the return! The fees alone make a big dent in your returns as well over long periods of time.

It’s a double whammy!

This is what you get from insurance salesman pretending to be financial advisors. Super expensive, underperforming investment options from companies like Capital Group. He gets rich on your dime.

Not all mutual funds are terrible, but on average, exchange-traded funds (ETFs) from low-cost brokers that just track the market are always your best bet. Very few actively managed funds outperform the S&P 500 over a 5 year period.

Get some basic education here and avoid all the traps the financial services industry has laid. Don’t make the mistake of thinking any of this is complicated. It just takes a bit of commitment to read a few finance books or blogs or watch some YouTube videos.

Frankly, in 2023, there is no excuse to not understand what you should do with your money, on your own.

The Matadore’s recommendation: Yes, liquidate the positions in your IRA (don’t cash it out!), and contact a discount brokerage firm like Schwab to do a rollover IRA for the total balance. Since all that money is from an old 401(k), it is pre-tax and needs to stay that way in order to avoid taxes and penalties.

It might be easy to be upset about this. Frankly, it pisses me off that there are “advisors” out there knowingly selling people things that are not in their best interest. But don’t get mad. Fire the insurance salesman and take control of your money!

If you absolutely think you need or want to be working with an advisor, find a fiduciary that is “fee-only”. Many will offer a custom plan for a one time fee, or annual fee that doesn’t change and is not based on assets under management (AUM). DO NOT pay AUM fees.

AUM fees are how wealthy people get ripped off!

Thanks for your question!

And, thanks for reading. Be good stewards of your earnings!

If you are looking for more help getting out of debt and building wealth, you can get my newly published Zero To Wealth Workbook here! This is the exact method I used to payoff debt and build wealth.

Some of my other, recent stories.

Dave Ramsey’s Home Buying Equation Is Impossible For (Most) Americans.

The “Bond King” Jeff Gundlach’s Portfolio for “7% Returns” In The Coming Economic Storm.

The information provided here is for informational and educational purposes only. It is not intended to be, and should not be considered as, financial advice. We do not provide personalized financial, investment, or legal advice. The Matadore is not a registered CFP.