Dave Ramsey’s Home Buying Equation Is Impossible For (Most) Americans.

The math doesn’t lie.

If you have listened to Dave Ramsey at all, you know he has repeatedly told listeners to follow the 25% rule when buying a house. More specifically, never buy a home with a monthly payment that’s more than 25% of your monthly take-home pay on a 15-year fixed-rate conventional mortgage.

I heard it again of late and like before, cocked my head, especially considering the numbers the caller in question relayed, but more broadly given my general understanding of incomes in America.

Let’s really examine this home-buying equation from Dave Ramsey.

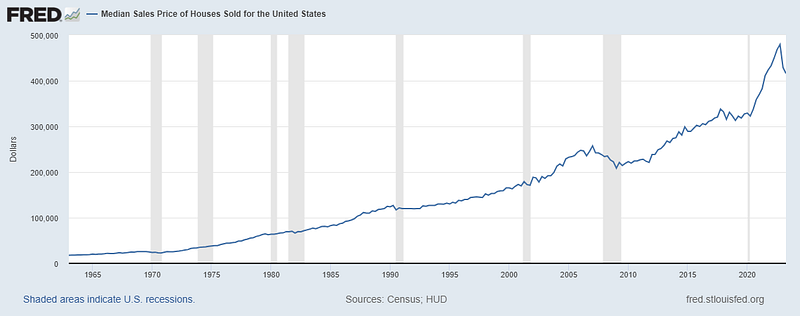

According to data from the National Association of Realtors, the median price for an existing home was $410,200 in June 2023.

So let’s figure out what that means for buying a home on a 15-year mortgage.

A $410,200 purchase price, minus a down payment of 20% of about $80,000 (which is a financial feat for the average American), means financing $328,000 or so on a 15-year fixed-rate mortgage.

Rates as of the date of this writing for a 15-year fixed are about 7%, even with an 800+ credit score.

(I am being liberal here for illustrative purposes. In all reality, most Americans do not have $80,000+ saved and don’t have 800+ credit scores.)

Are you ready for it?

$3,719 a month, just in principal and interest.

Realistically, property taxes, insurance, and maybe an HOA would make this even higher.

But let’s just go with $3,719 for this exercise.

What would you need to be making annually to fit a $3,719 mortgage payment into the 15%/25% guideline?

Again, under Dave’s guidance, we would be shooting for $3,719 being 25% of take-home pay, so you would need about $12,000 monthly take-home!

Running that backwards through a tax calculator we get the following.

For a take-home of $12,000, we need…

Gross Earnings of about $16,500.00, monthly! Here is the math:

- Total Taxes: $4,408.92

- Federal Income Tax: $3,146.67

- Medicare Tax: $239.25

- Social Security Tax: $1,023.00

Take Home: $12,091.08

Mind you, this does not take into account deductions for health benefits, or the 15% of retirement savings off the top Dave Ramsey advises you save.

But stay with me and let’s put a $16,000 gross monthly income into perspective.

$16,000 monthly equates to about $192,000 gross. And, just 12% of U.S. households earn $200,000 or more annually, according to Census Bureau data.

What is the average household income (to match the average cost of a home in the USA) you ask?

Again, according to the U.S. Census Bureau, that number is $74,580. Of note, that is a 2.3% decline from 2021 estimates of $76,330.

A little short of the $200,000 needed, I would say.

Again, these are all averages, which of course means we can find cheaper homes that might get closer to the 15%/25% rule. We can also find even higher costs for homes where even $200,000 a year won’t get near the 15%/25% equation.

Further, just as the lower cost of living areas will show lower average household incomes, the opposite is true for the higher cost of living areas.

This is to say, “affordability” evens out, and a 15-year fixed-rate mortgage payment that is 25% or less of your take-home pay, is a pipe dream at best for 80% or more of Americans.

What do you think?

Is Dave Ramsey’s home-buying recommendation indeed unrealistic for most people?

What about people who can afford to take on a 15-year fixed-rate mortgage within the 25% of income ratio; does it even make sense?

Thanks for reading. Be good stewards of your earnings.

Subscribe to get my posts via email and get my E-book “Zero To Wealth” for Free!