Are We In Housing Bubble 2.0?

The signs are worrisome.

The housing market in 2021 looks an awful lot like the one in 2008, except this time the market is heating up after a recession rather than causing one.

It is not uncommon to hear of double digit offers, all over asking price, submitted in just days after a house comes on the market.

What the hell is going on?

Come to find out, a hell of a lot, including the combination of

- (Still) historically low interest rates

- Pent-up, generational demand

- Rock bottom inventory levels

Let’s take a look at how these three aspects have created a roller coaster ride for home buyers.

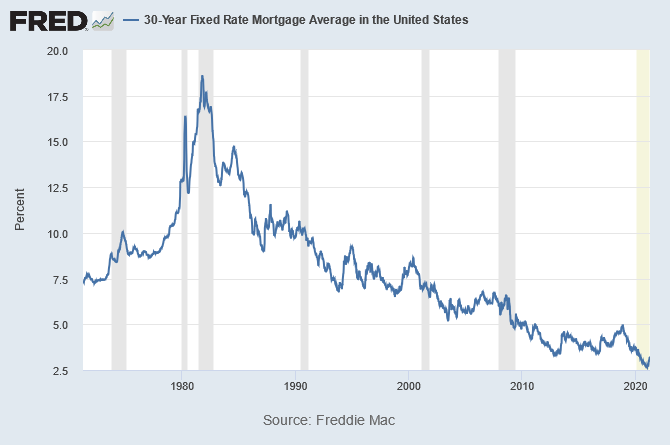

Interest Rates Our Parents Would Kill For

Mortgage interest rates in the 1980’s were close to 20%. Today they are 2–3%

What does that mean?

Mortgages are similar to bonds, in that as the interest rate on the debt goes up, prices go down, and vice versa.

I started seeing the “historically low” description applied to interest rates during the housing boom starting in 2005-ish, with a much higher frequency after the Great Recession.

We have been experiencing 15 years of a historical anomaly, so no wonder housing prices are going up.

People are beginning to think that we only have a limited amount of time before interest rates rise, and they don’t want to be stuck with a higher mortgage payment next year.

(It’s ironic, since the payment will be about the same: it’s just how much will go towards interest vs principle.)

Gen Z Are Fighting Millennials for Their First Homes

Millennials got royally screwed by the Great Recession, putting off marriage, kids, and buying a home for years while they recovered from the financial shellacking of 2008–2009.

During that time, Gen Z started entering into the workplace during a boom, and they want to do all the things earlier than their older peers.

The oldest subset of millennials graduated from college right as the economy went into a recession, which has presented career- and income-related hurdles that have delayed other life milestones.

Gen Z, on the other hand, is coming of age during an upswing in the economic cycle and benefiting from that.

Now, two generations want to buy houses at the same time.

Additionally, the pandemic-induced desire to leave populated areas is pushing up demand even further.

Inventory is Nowhere to Be Found

After the housing bust in 2008, many home builders went bankrupt, got bought out/merged with another company, or decided to just get out of the game completely.

The remaining companies decided not to repeat history with mass production of low- and middle-income houses, and instead focused on high-end, high-margin custom homes.

[The current situation] is the polar opposite of what the company faced during the subprime bust that began around 2007, when the housing market was gripped with a massive oversupply problem that took almost a decade to correct.

Construction of new homes collapsed in the aftermath of that crisis and never recovered. The supply of new homes remains very low today.

“We’ve been under-building for the last 15 years,” said Jeffrey Mezger, CEO of KB Home.

This created an inventory vacuum more than a decade in the making, and it will not be fixed anytime soon.

Additionally, many homeowners who would otherwise sell are staying put for a couple of reasons.

- They are refinancing and upgrading their current home.

- They don’t want to hold open houses and expose themselves to COVID.

- They don’t want to sell, then be forced to buy a house that eats up their profit (if they can even find a house).

“Affordability crunch resulting from strong home price growth and higher mortgage rates will discourage some potential home buyers from entering the market and take some wind out of its sails, slowing the home price growth rate by about a half by the end of 2021,” said Selma Hepp, deputy chief economist at CoreLogic.

“Potential sellers may be discouraged by their inability to find a new home and subsequently choose to not list their own home — leading to a vicious cycle of declining for-sale homes,” Hepp said. (emphasis added)

The only way to make money selling a house in this market is if you are downsizing, but that just doesn’t seem to be happening all that much.

Where Does It End?

This is the question, isn’t it?

And if I knew the answer, I’d be rich.

My guess is that a few things will gradually happen over the next 2–3 years, moving more people towards buying homes.

First, the pandemic will end, and sellers will feel comfortable holding open houses.

Second, rent will get high enough that a mortgage payment will start to look appealing.

Third, home builders will finally start building more (relatively) modestly priced homes, easing the inventory strain.

Most Recent Stories

- What’s Going On With Inflation?

- Biden’s Infrastructure Plan Is Good, But Not Great

- COVID Destroyed Women’s Finances

- Jobs, Jobs Everywhere, and Not a Soul to Work

Don’t miss my next article! Click here to get notified when I publish new material.

If you love the articles published in Money. Daily., then become a member of the Medium community and get full access to our full archives.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.