A Step-by-Step Guide on How to Create your Own Budget Plan

A budgeting plan for those who have goals to chase

For unlimited access to Dare to Finance articles, you need to become a Medium member. By signing up through this link, you would be supporting Dare to Finance writers and gain access to many well-written articles across various topics on Medium.

Introduction

Having a good budgeting plan that works for you is important because it serves as the first pipeline on how you utilise your salary. It is like an instruction manual where you tell your money where to go instead of figuring out where it should be at the end of each month.

In this article, we will introduce you to a goal-based budget framework for those who aim to achieve more in life.

Limitation of 50/30/20

The 50/30/20 rule is perhaps the most popular framework that many financial gurus recommend internationally. It is simple and beginner-friendly for anyone to get started with. However, it has its own set of limitations and may not work well for anyone who aims to achieve several financial goals in their life and especially in a country like Singapore. If you wish to find out more about the limitation of the 50/30/20 budgeting rule check out our previous post here:

Goal-based budgeting

This goal-based budgeting framework that we are introducing in this article revolves around your financial goals as well as the self-love fund that we often talk about at Dare to Finance.

This budgeting framework is designed to help you stay focused on what brings you the most value in life and prevent you from getting distracted along the way.

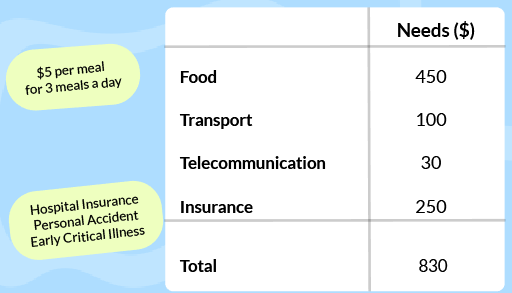

Step 1: Know your minimum monthly expenses

First and foremost, calculate what is the minimum amount of expenses you would need every month. This amount that you calculated for your needs is your non-negotiables. If you wish to cut back on your expenses at any point in time, this will serve as your lowest limit.

To do it effectively, be realistic and truthful about what is the minimum amount you would need to get by the month. (On the other hand, don’t go overboard and reduce 3 meals to 1 meal a day- being realistic is key here.)

An example of your minimum monthly expenses may look something like this:

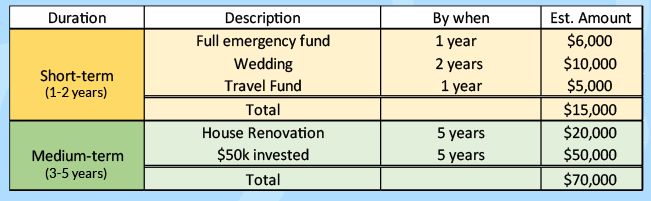

Step 2: Understanding your goals

This is where things get a little bit more exciting and is the most important step of this goal-based budgeting framework. For this step, list down all the goals you wish to achieve in life, how much is needed and when you aim to achieve them. These goals that you set for yourself will also act as a motivation to get you going and stay disciplined.

At this step, your goals should not be bounded by any financial possibility. It can be as wild as buying an island or as small as buying a house appliance that you have been eyeing for a while. Once you are done with that, categorise your goals into 3 categories — short, medium and long. This will help later when coming up with a game plan.

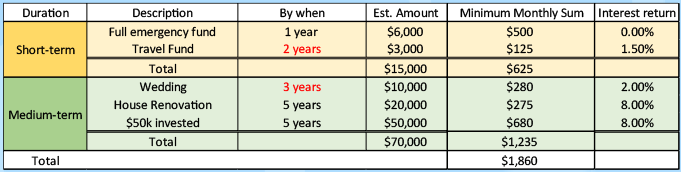

Once you are done with this step, you should have something that looks like this.

We created this with a fresh graduate in mind. If you have any long-term goals that you wish to achieve, we would suggest breaking them up into multiple medium-term goals. This will make it less daunting and your goal S.M.A.R.T (Specific, Measurable, Achievable, Realistic, and Timely).

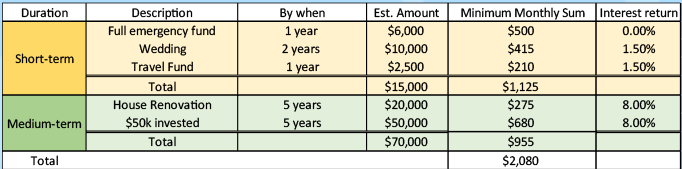

Step 3: Coming up with your game plan

Next, calculate what is the minimum amount you will need to set aside each month to achieve these goals. Funds that you need for your short-term goals should be easily accessible and stashed in a place stable enough to meet your goals when you need them. While for medium-term goals, you can consider investing them and converting them to more stable assets when the date draws nearer.

To calculate how much you need for each goal, you can use an online investment calculator that accounts for regular contributions and interest returns. Here is one that works great for me.

When determining how much interest return for each goal, look into when you need to fulfil your goal and how important achieving it is to you. This is ultimately tied to how risk-averse you are and how you plan to raise this money.

Once you have done that, you will get something like this:

Once again, we are planning this with a fresh graduate in mind. It is based on the assumption that they have $0 in their bank account. If you already have some savings on hand, add a column on how much you wish to allocate to each of these goals and recalculate the minimum monthly contribution.

Step 4: Readjust your goals

This is when you bring yourself back to reality. You may realise that the goals you’ve set for yourself may not be realistic for your income level. In this case, it’s time to readjust your goals.

You can take different approaches in adjusting your goals, it could be reducing the budget, delaying it or even completely pushing it aside to revisit it again during your next planning. We recommend maintaining the interest return as it is. It is easy to simply adjust the interest rate to match your goal but it might not be realistic for you to actually achieve it. For example, setting a 20% return on investment can make a lot of goals seem a lot more achievable in terms of the timeframe but getting a 20% return may not be realistic. The interest return you set should be realistic and achievable within your reach.

Example of goals readjustment:

Sticking to the fresh graduate example, if he earns a take-home pay of $3,000 after deducting his non-negotiables expenses in step 1, he is left with $2,170. Although $2,170 is enough for him to meet his goal of $2,080 it may not be sustainable in the long run. Remember that the expenses we calculated in step 1 only accounts for the non-negotiables expenses, and only having $90 in surplus ($2,170 -$2,080 = $90) might stretch you too thin. More on that in step 5.

After readjusting his goal, it will look something like this.

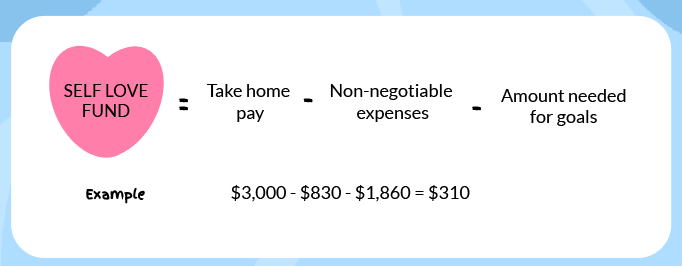

Step 5: Self-love fund

The final step of this goal-based budgeting framework is to calculate the balance in your self-love fund. This fund is where you can spend on things beyond the basic expenses you calculated in Step 1. These would include entertainment costs, that extra date night expense and many more!

This self-love fund is an important portion of the goal-based budgeting framework to re-energize yourself while you chase towards the bigger goals in life. We recommend having at least 10% of your income towards this self-love fund. While there are many goals that are important, don’t forget to live in the present. It could be as simple as treating yourself to an expensive ice cream you love but small self encouragements like this can keep you going as you move towards the bigger goals in life.

Caveat

For this budgeting framework to be beneficial for you, you will need to be aware of your financial goals, especially those of long term. For example, it could be “ I want to have accumulated $800,000 by the age of 50 so that I can withdraw $3,000 monthly for 30 years thereafter”. This is to account for the asset you need when you retire. While it is not everyone’s goal to achieve financial freedom, it is still our individual responsibility to be financially sustainable when we retire.

Additional Information

If you choose to adopt this framework, it would be recommended to revisit time to time when you have new goals or when your income increases.

Summary

To sum this article, here are the 5 steps in this framework:

Step 1: Calculate your minimum expenses

Step 2: Understand your financial goals

Step 3: Determine the monthly amount needed to set aside for fulfilling your goals

Step 4: Readjusting goals to be achievable within earning capability

Step 5: Calculate your self-love fund

Conclusion

Like all the other budgeting frameworks out there, there are pros and cons. There is no one best budgeting framework but rather the best one for you. This goal-based budgeting framework that we introduce in this article is just a guideline that you may need to adjust to fit your needs.

If you have adopted this framework in your life, join the community of like-minded individuals who are working towards their goals here.

For unlimited access to Dare to Finance articles, you need to become a Medium member. By signing up through this link, you would be supporting Dare to Finance writers and gain access to many well-written articles across various topics on Medium

About Dare to Finance

We are a platform based in Singapore that creates content ranging from Personal Finance, Adulting to Beginner Friendly investment.

If you have something to share that is relevant to our focus topics, write to us here and earn through the Medium Partners Program.