Budgeting 101

Why the 50/30/20 Rule Won’t Work

Deconstructing the ever famous budgeting framework

The 50/30/20 budget is a popular budgeting framework that gives guidance as to how one should allocate their income. According to this framework, your income should be split into 3 different portions —your needs, wants and saving/investing.

It’s the framework that is mentioned by numerous financial gurus but when actually applied to my Singaporean lifestyle, it just doesn’t seem to sit well with me. In this article, we would be covering its limitations and why it may cause more harm than good.

What is the 50/30/20 Rule?

50% needs

Based on this framework, it is recommended for 50% of your income be allocated towards the necessity. This includes essential costs such as rent, food, utilities, insurance, transport etc.

30% wants

This category includes everything else that isn’t considered an essential cost. To put it bluntly, it refers to things that you can live without. It can range from anything between luxury brands to a dessert after a meal.

20% Savings/Investing

The final category is what you should be setting aside each month for your emergency fund, retirement and other investment goals.

Why it won’t work for you

1. Encourages wasteful spending

While allocating 50% of your income to your “essential needs” may be restrictive for some, it’s heavily dependent on what your monthly commitments are.

To many who don’t own a car because they stay in the city (i.e New York, Singapore etc) or simply don’t pay rent, allocating 50% of your income to this segment of expenditure is far too much. In such cases, you may feel compelled to spend more because it feels validated.

For a typical Singaporean, that is exactly the case. Firstly for most of us, our flat is paid through our CPF and for the next biggest expense, a car — it is usually not seen as an essential expense thanks to our very well-connected transport system.

Similarly, this applies to the 30% allocation of “wants” where you may form a habit of spending more than planned.

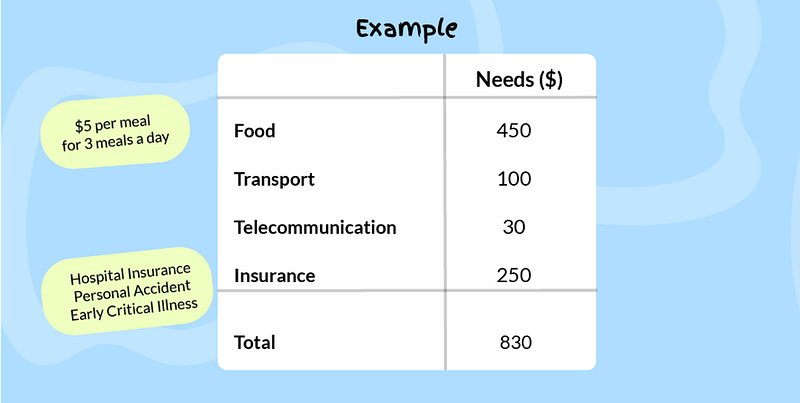

Let’s try to visualise this in a case study:

John is a fresh graduate who earns an annual salary of $36,000. As such, making his monthly budget breakdown of $3,000 look something like this:

50% (Needs) : $1,500

30% (Wants): $900

20% (Saving/Investing): $600

As a fresh graduate, the following may be what you are spending on at the minimum. (We understand that for some of our readers you’ll have to account for parental allowance, but more on that next time. )

If you follow the 50/30/20 framework blindly, you will have a surplus of $670 after spending on your actual “needs”. This may in turn “encourage” you to start increasing your expenditure on food or other unnecessary wants.

Certainly having a total expenditure of 80% (includes both needs and wants) of your income is overstated.

2. Restricts amount saved for future goals

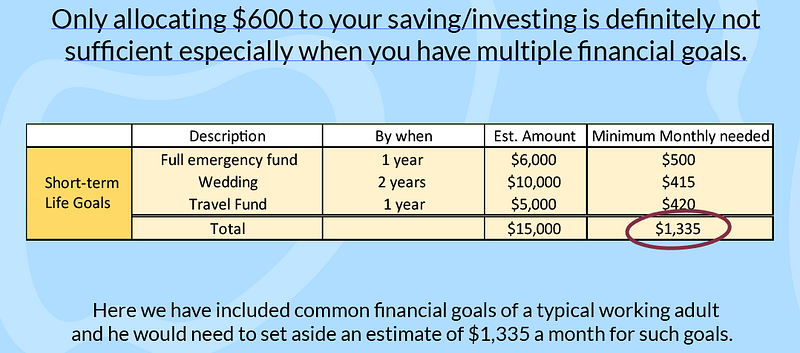

An exciting part about starting in the workforce and getting a monthly income is planning towards your life goals. Whether that is purchasing your own home, having that beautiful wedding of your dreams or perhaps simply travelling abroad without much to worry- they all cost money.

Let’s not forget about accumulating our full emergency fund as well.

Moreover, with the rising desire of achieving financial freedom early, only allocating 20% (equivalent to $600 in the previous example) to savings and investment is definitely too little.

Upon calculating an average working adult's short term life goals, someone like John would require at least $1,335 allocated to “savings and investing” to fulfil his short-term life goals. To top it off, he also has to plan for his mid to long term goals that are not yet accounted for.

3. Vulnerable to lifestyle inflation

It’s only natural for our income to increase as years go by. However, when that happens, due to this framework being one that ties your expenses as a ratio of your income, your expense budget will grow together with it making you more susceptible to lifestyle inflation.

Lifestyle inflation refers to an increase in spending when an individual’s income goes up.

When your expenditure increases together with your income, it's easy to form unhealthy spending habits. This is further accelerated as lifestyle inflation tend to increase with each pay raise. It can eventually make it difficult for one to save for retirement, other financial goals and even leading to taking loans they can’t afford. To top it off, it can be very difficult to lower your standard of living when changes have to be made.

Conclusion

Personal finance is personal for a reason and while the 50/30/20 budgeting rule may give a very rough structure and starting point to many who are starting their journey, it does not apply to all and throughout their life.

There are elements that we have to change and question whether it applies to us. After all, these budgeting frameworks are here to help us achieve our financial goals and not stilt them.

For unlimited access to Dare to Finance articles, you need to become a Medium member. By signing up through this link, you would be supporting Dare to Finance writers and gain access to many well-written articles across various topics on Medium

About Dare to Finance

We are a platform based in Singapore that creates content ranging from Personal Finance, Adulting to Beginner Friendly investment.

If you have something to share that is relevant to our focus topics, write in to us here and earn through the Medium Partners Program.