What the Money Gurus Don’t Tell You Can Kill You

Don’t stress over inflation and quality of life

If you read the wrong money writers, you might be putting your physical and mental health at risk.

This isn’t hyperbole. I ain’t into melodrama.

In fact, I’m not going to be the one to go and make things so complicated. When my peers who write about personal finance and investing muddy the waters, it gets me frustrated. So, you’re never gonna find me faking.

Thank you to the great Canadian, Avril Lavigne, for the lyrical inspiration. And thank you to Medium user, MIkeintherain, for saying what I want to say better than I could ever say it.

In a recent Making of a Millionaire article, here’s how Mike responded to a discussion about the best way to way to invest in stocks:

If I was a pretentious money type, I’d scold Mike for “ignoring inflation.” I recently riffed about the gurus who love to guru-splain inflation to the rest of us:

It’s even more difficult to talk a friend down when they’re freaked out about having enough money to pay their bills. You can help your friend better situate their finances. However, if the first thing you explain to your friend is inflation, you’re a bleeping know-it-all who is ultimately doing them a disservice.

The best advice you can give anyone looking to situate their personal finance is to determine how much cash they need on hand to meet their obligations, cover periods of reduced income, achieve additional goals, and make them feel secure enough to keep the money they eventually invest in the stock market invested…

Explaining inflation makes people feel smart. Trying to understand emotion makes them feel uncomfortable. Yet, emotion reeks far more havoc on people’s money than inflation ever will.

While I can’t put words in Mike’s mouth (we’re battling a highly contagious virus, for goodness sake), I’m confident he thinks about emotion more than inflation when personalizing his finances.

I’m not going to go on a long soliloquy. There’s no need for it because I have an absolutely straightforward point to make.

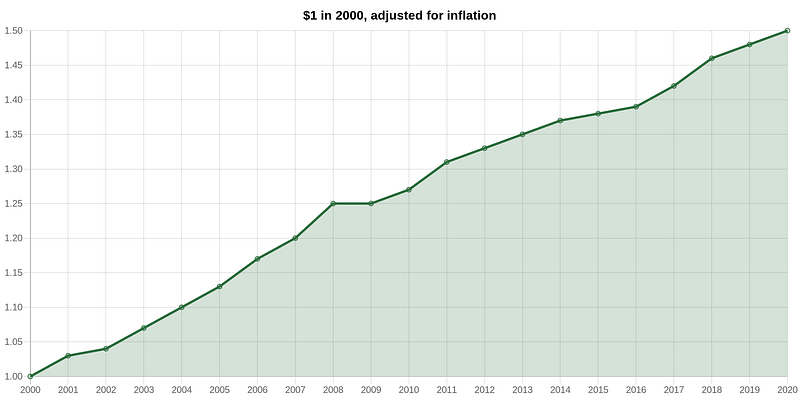

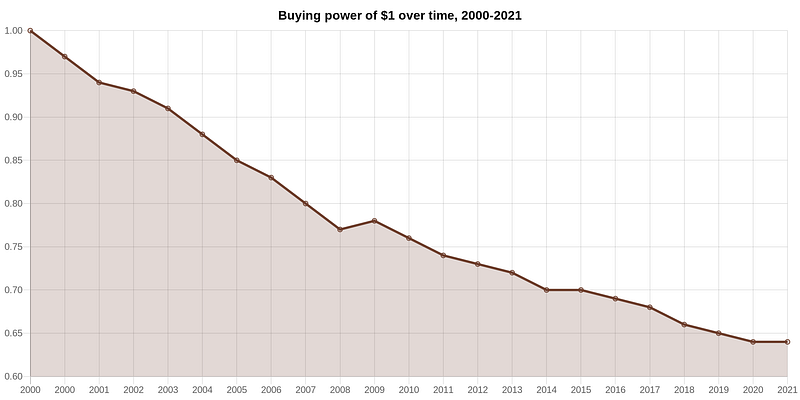

Yes, money loses value over time.

Yes, if you sit in cash, the money you hold today will provide less purchasing power going forward. The money you held yesterday (not technically “yesterday,” but you know what I mean) will secure less of what you need today.

A child can understand this.

For some of us, seeing it presented this way makes more sense.

Irrespective of how your math brain works, an adult can stress out over this to the point of poor or, at least, unsettled health. I know a few people like this. Inflation terrifies them. This is because, in part, they’re reading the wrong people. Money writers who sound the alarm for the express purpose of going on to impress you with what they know (and, to their delight, what you apparently don’t know).

When these friends talk to me about my work, they often ask about inflation. I tell them exactly what I’m writing today. I tell them I don’t generally give money advice to friends, but I care about them, so I want to save them from having a stress-induced heart attack as they needlessly worry about $1.00 only being worth $0.60 in 30 years.

I’m not saying don’t invest your money. This would be insane. However, you’re going to feel more cool, calm, and collected in your skin if you follow 65-year old Mike’s way. Mike appears to understand emotion and the power of having a handle on your cost of living and resultant quality of life.

Here’s how you deal with inflation. The same way you deal with that terrifying situation when you’re walking your dog, she poops, and you don’t have a bag. You’ll do one of two things:

- Stop. Casually look around. Slink away with no intention of picking up the poop. Sometimes, shit happens. It’s fertilizer.

- Stop. Casually look around. See if you can borrow a bag from a fellow dog walker. If you can’t find anyone, you use a leaf or maybe even walk home, get a bag, and return to the scene of the crime.

Translation: Ignore inflation sometimes. Deal with it rationally other times. But be casual about it. In fact, put your thoughts and strategies on autopilot.

You can adopt this mindset and pursuant strategy without ever using the word inflation. It’s not even part of the equation. Because it doesn’t have to be. If you have a sound personal finance and investing strategy in place, chances are it’s dealing with inflation — and a whole host of other apparently scary things — on its own.

Make being cash secure priority number one. All you need to do to figure out what this means is reread Mike’s excellent response.

Make an insanely or just a modestly low cost of living an attendant priority.

Prepare to adjust. If you’re really set up from a cash standpoint, the cost of goods and services increasing in price amounts to a rounding error in your checking account and accompanying cash cushion accounts. If things are a bit tight, adapt to your surroundings.

You’ll be much better off being more selective about what you buy and where and when you buy it than you will anticipating inflation and stressing over it. I absolutely am saying that, in this case, you’re better off being reactive than proactive, at least to some degree.

Reactive — I will respond to inflation by cutting costs in one area to offset rising costs in another area (if you even end up needing to this, which you probably won’t). Here again, it comes back to something we talk a lot about — compromise:

Compromise isn’t a bad word.

It’s just a choice you make in one area to get something you want more in another.

Proactive — this is the part where, after you’re cash secure, you invest as much of the money you have leftover into a portfolio that will beat inflation. It won’t beat inflation because you went into the process of constructing the portfolio saying, damn, I gotta make sure I beat inflation. It will beat inflation — and do dozens of other great things — because, in and of itself, it’s just a solid, well-constructed, defensive investment portfolio.

You don’t go into a conditioning program for a sport saying I need to do this because the sport’s going to get harder to play as I get older. You train because it’s an all-around good idea. It will make you stronger (or whatever). It will help you compete today. And, with any luck, it will contribute to you staying in the game for as long as you’d like.

Imagine obsessing over ageing when you’re trying to enjoy physical exertion or competition today. This is the height of insanity.

It’s not all that different from managing your money.

Solid strategies — like the ones we share on Making of a Millionaire — exist so you can live. So you don’t have to eat, sleep, drink, and stress over money. They exist in a way that a basic structure — and a basic understanding of this basic structure — takes care of all the things you don’t need to concern yourself with.

If you’re an information junkie or love following your money on a frequent basis, great, go for it. Just don’t stress over it.

If you’re a person who doesn’t want to spend their time thinking about money (at least not as much as I do), then there’s no need to do anything other than:

- Hold enough cash, so you feel cash secure and comfortable.

- Hold enough cash so you can deal with emergencies and unexpected expenses.

- Hold enough cash so you can do things you want to do — take a vacation or bring your partner to the occasional fancy dinner.

- Hold enough cash, so you don’t have to think twice about putting surplus cash into the stock market and — this is the key — leaving it there.

Inflation doesn’t hurt us as much as selling stock —

because we needed cash…

because we didn’t hold enough cash…

because we listened to some jerk talking down to us about inflation.

This article is for informational and entertainment purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.