What Happens When You Trade Stocks Based on News?

The outcome of backtesting a trading strategy based purely on financial news

We all know that one of the most impactful catalysts for stock price movement is financial news. A lot of negative press can drive a stock price through the floor. Conversely, positive financial news can skyrocket a former penny stock to the moon. Now, what would happen if we were to trade stocks purely on the sentiment from the press. Is it possible to ride the positive news wave to large financial gains? Or will it have been too late?

Seeing news headlines’ effect on stock price movement has been done before but I wanted to observe what would happen if you were to actually implement the financial news trading strategy. To do so, I used Python to code a backtesting process that would determine trade positions based on the sentiment from the previous day’s financial news.

I’ve attempted something similar to this before but with Tweets instead of headlines:

However, I wanted to see the outcome from backtesting news headlines instead.

With all this in mind, let’s begin and I’ll show you how I conducted this quick experiment…

Import Libraries

To start, I imported many different libraries necessary for this backtest to run:

# Libraries

from eod import EodHistoricalData

import pandas as pd

from datetime import datetime, timedelta

from tqdm import tqdm

import nltk

from textblob import TextBlob

import numpy as np

import random

import plotly.express as px# Importing and assigning the api key

with open("../../eodHistoricalData-API.txt", "r") as f:

api_key = f.read()

# EOD Historical Data client

client = EodHistoricalData(api_key)Getting News and Price Data

If you noticed above, I used a Python library called eod. This library allows me to retrieve not only price data but financial news data as well. If you want to follow along you’ll need to use your own API key from EOD HD. It’s free to sign up and you’ll have an API key in no time. Disclosure: I earn a small commission from any purchases made through the link above.

To retrieve the news and price data from a select stock ticker, I created a function to streamline the process:

Time Period Retrieval

Within this function, I am able to retrieve the financial news for any available stock ticker in 10 day windows. This is done to spread out the retrieval of financial news over the given time period. If I were to have done it over a period of say 1 year instead of 10 days, then I potentially risk only retrieving the most recent news instead of news from a year ago. This was the problem I had initially with the function.

Filtering Out Irrelevant News

After retrieving the bulk of the financial news, I had to filter out any irrelevant news. Many times, some of the news content retrieved may just have a passing reference to the selected stock, which is unnecessary for this experiment. In order to make sure that the news article is mainly about our given stock, I filtered out any news headlines that don’t mention our stock at all. The headline would need at least one mention of the stock symbol in order to pass my custom filter.

Price Data

With the relevant news data prepped and ready to go, I finally retrieved the price history for the selected stock from the same period of time as the financial news. I then separated the news and price data into separate Pandas DataFrames for formatting later on:

# Retrieving TSLA news and price data from the past 400 days

news, prices = getNewsAndPrices("TSLA", 400)Getting News Sentiment

With the price data and news headlines available, I can now move to the next step of extracting the sentiment from those headlines. There are many tools to use in order to analyze sentiment for these headlines such as NLTK’s Vader or Flair. But for me, I went with a library called TextBlob.

# Getting sentiment values for the news headlines/titles

news['sentiment'] = news['title'].apply(

lambda x: TextBlob(x.lower()).sentiment[0]

)# Grouping together dates and aggregating sentiment scores from the same day

df = news.groupby('date')[['sentiment']].mean()After extracting the sentiment scores for each article’s headline, I then aggregated the scores for articles released in the same day by using the average of all the scores on that day.

Calculating Trade Positions

The next step after grabbing the sentiment scores would be getting the trade positions based on the headline sentiment:

def sentimentPositions(val, thresh=0.1):

"""

Returns position as 1, -1, or 0 for Buy, Sell,

and Do Nothing respectively based on the given

sentiment value and threshold.

"""

if val > thresh:

return 1

elif val< -thresh:

return -1

else:

return 0# Applying the position function

df['sentiment_positions'] = df['sentiment'].apply(

lambda x: sentimentPositions(x, thresh=0)

)With this function, I can determine what the trade position can be based on the given sentiment score and threshold. Since given sentiment scores are based on a range of -1 to 1, I can determine the trade position by looking at the score and threshold. For example, with a given threshold of 0.1, the function will only return a Buy position if the sentiment score is greater than 0.1 and vice-versa for Sell/Short positions.

Combining News Sentiment and Price History

Now that I have the trade positions based on sentiment scores and price history, I can combine both DataFrames in order to start the backtest:

# Merging price history and sentiment positions

df = df.merge(

prices,

right_index=True,

left_index=True,

how='outer'

)# Filling in empty values with their most recent value for positions

df['sentiment_positions'] = df['sentiment_positions'].fillna(

method='ffill'

)When the positions have been merged with daily price history, NaN values will be present when there are no news headlines for that day. In this case, I used the most recent sentiment position to determine the position for that day, which is why I fill in the NaNs with the forward fill method.

Performing the Backtest

To begin this backtest, I first needed to establish a few other trade positions which would act as baseline performance measurements. I added Buy & Hold and random choice strategies to compare to my news headline based strategy. The Buy & Hold strategy will buy the stock right at the beginning of the backtest and will never exit out of its position. The random choice strategy will randomly choose between Buy, Sell, or Do Nothing everyday. In the end, we shall see which strategy performs best.

# Positions shifted ahead by one to compensate for lookahead bias

position_df = df[['sentiment_positions']].shift(1)# Buy and hold strategy

position_df['buy&hold'] = 1# Random strategy

position_df['random_positions'] = random.choices(

[1,0,-1], k=len(position_df)

)# Dropping the last Nans

position_df = position_df.dropna()Now I can perform the backtest on the different strategies laid out above.

# Log returns

log_returns = df['adjusted_close'].apply(

np.log

).diff()# Performing the backtest

returns = position_df.multiply(

log_returns,

axis=0

)# Inversing the log returns to get daily portfolio balance

performance = returns.cumsum().apply(

np.exp

).dropna().fillna(

method='ffill'

)The backtest has been performed and if you want to look at the raw numbers you can observe the DataFrame saved within the performance variable. However in the next section, you can see the performance results visualized.

Backtest Visualized

The first stock I attempted the backtest on was AMD. As you can see from the graph above, the overall performance was better than random choices but still not enough to beat a Buy & Hold strategy. Throughout the backtest, there were instances where the news sentiment strategy beat B&H (Sept. to Nov.) but also instances where it performed worse (first 6–8 months).

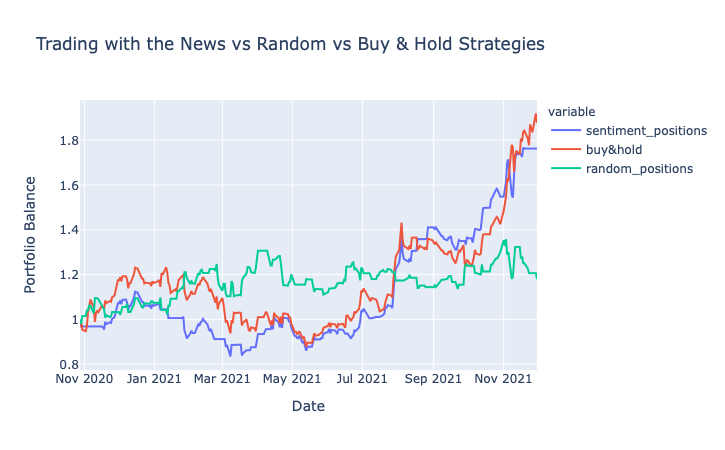

To see if these results were common with other stocks, I also performed the backtest again on TSLA:

With TSLA, the performance between B&H and news sentiment initially was identical. Afterwards, the performances diverged. The news strategy also had an instance of outperforming B&H but in the end it did not beat out B&H. However, throughout all this, the sentiment strategy was still miles better than random choices.

Closing

While using news sentiment to trade stocks is not a new strategy, I still wanted to see its performance in action. The outcome was a bit better than expected but not enough to officially use news sentiment as a primary trading strategy. More testing with different scenarios may be required to know the full extent of this strategy.

However, I believe that if you were to combine this strategy along with some Machine Learning Time Series forecasting, then you might have something that can possibly beat the simple Buy & Hold strategy.