What Do U.S. Housing Price Predictions for 2023–2024 Look Like and Why?

The average U.S. family can no longer afford to buy the average house. That already happened in 2022 — done deal. But wait…it gets much worse.

Related and recent articles

• Would We Be Smart to Ask These 3 Questions About the Housing Market? • What Are 4 Things Smart Homebuyers Do If Their Mortgage Rate Is Over 5%? • (Part 1) The 5 Most Important U.S. Economic Events Over the Last 50 Years • Did This Happen by Accident to 89% of America’s Stock Market Wealth? • Pressing Where It Hurts: How to Win Fights That Matter • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles.)

Three important things happened in U.S. housing over the past 2.5 years since March 2020:

- Housing prices rocketed upward. • 30% increase in the 21 months from April 2020 through the end of December 2021. • 37% increase in average prices from Q2 2020 to Q2 2022. • Such a rapid and substantial housing price increase at the national level is pretty much unheard of.

- Mortgage rates stayed fairly constant from April 2020 through end of December 2021, right around 3.00%, plus or minus about 0.3%.

- Starting in early 2022, mortgage rates began increasing rapidly. • They are now (October 2022) in the 7% range, which is a dramatic change from the 3% level at the beginning of 2022.

Roadmap for this article

Part 1. Why U.S. Housing Prices Will Go Down in 2023–2024

Background, context, and reasons — all in plain talk.

Part 2. How Much Might Housing Prices Go Down in 2023–2024

A cool — but scary — chart in this section.

Part 1. Why U.S. Housing Prices Will Go Down in 2023–2024

Normally interest rates are the major factor in driving housing prices higher or lower at a national level.

But high or rising interest rates were NOT what pushed prices up in 2020 and 2021 during the pandemic.

Interest rates basically held steady for the 21 months from April 2020 through the end of December 2021.

But housing prices? They vaulted upward — relentlessly upward — during this time.

There were 3 qualitative factors that combined to push housing prices upward from April 2020 through December 2021:

Factor #1: “Increased demand for working from home accounted for more than 60% of overall price hikes and similar increases in rent during that period.” (CNBC, 09/28/2022)

Factor #2: The massive runup in the stock market from March 2020 through the end of 2021. This made it much easier for people in the Top 10% — and especially the Top 1% — of the population to buy new homes, second homes, third homes, vacation homes, investment homes, etc. during 2020 and 2021. (…since 89% of America’s stock market wealth is owned by the Top 10% of the population.)

Factor #3: Permanent capital buying up homes to then rent to people who can now only afford to rent.

- Investors Bought a Quarter of Homes Sold Last Year, Driving Up Rents (Pew Trust, July 22, 2022)

- Warren Calls Out Private Equity-Backed Firms for Increasing Rents, Driving Up Housing Costs, and Raking in Profits Amid Housing Shortage (Jan 13, 2022)

- Real Estate Predators Tried to Cash In on the Pandemic. Then Tenants Fought Back. (Mother Jones, May•June 2022)

The upward pressure created by these 3 factors has mostly evaporated as of Q4 2022.

Indeed, a couple of the factors have actually reversed and could soon be putting negative pressure on prices . . . if they aren’t already doing so:

- It is safe to say that “stock market gains” won’t be pushing the housing market up again anytime soon. Whether or not we are in the middle of a really substantial bear market or not, the stock market is clearly in the process of correcting its massive runup.

- It’s no longer the case that increasing numbers of people are starting to work from home. To the contrary, people are now slowly but surely starting to go back to the office. The tide has turned on this factor, too (although it seems likely that it will be a long time — if ever — before we get back to pre-pandemic office occupancy levels.)

- And there are signs that private equity investors are pulling in their horns, too, and getting much less aggressive about buying large numbers of houses. Now that private equity investors are seeing/sensing that prices have turned down, they are going to start wanting to wait and let the correction in housing prices work its way through the system. Nobody likes to try to catch a falling knife.

What are the effects and implications of (1) the housing price rise of 2020–2021 followed by (2) a really large rise in mortgage interest rates in 2022 and perhaps 2023?

Regular people can no longer afford to buy a house in the U.S.

The increase in housing prices alone — all by itself — has pushed the average house out of range of the average family But as soon as interest rates started to spike, the game was over. The average person — the average family — in America REALLY can no longer afford to buy the average house. Game over.

Adjustable Rate Mortgages

Anyone who got an Adjustable Rate Mortgage (ARM) over the last few years instead of locking in a 30-year fixed-rate mortgage at historically low rates is probably going to be hurting when their mortgage resets to much higher rates. This will have the effect of dramatically increasing their monthly mortgage payment. How many families will be able to afford this? What will happen if they can’t afford the much higher monthly payment?

Geographical mobility has just plummeted.

If you’re already in a house at a relatively low mortgage interest rate and you don’t have enough equity or savings to “pay cash” to buy a new house, then you are locked into your current house. You’re not moving. If you are fortunate enough to have a 3% fixed-rate 30-year mortgage, there is just no way that you’re going to exchange that for a 7% fixed-rate 30-year mortgage. You’re not moving.

You are locked into your current home and location.

There may also be social and/or political implications. If more people than normal — perhaps many more people than normal — are unable to move away from their current home, then blue states are more likely to remain blue, and red states are more likely to remain red.

Permanent capital (private equity, etc.) is now one of the only players with enough liquid money to buy large numbers of houses.

They are the only players left standing with the capital to buy large houses in bulk.

Over the past couple years, they have become a major player. They’re not buying most of the houses in the US by any stretch, but they are buying enough to create enough marginal demand that swamps the marginal supply. And they generally pay cash . . . and sellers tend to prefer cash deals.

This HAD the effect of pushing housing prices higher by quite a bit.

But as I noted above, permanent capital is getting more defensive in the houses they purchase.

They are holding out for better deals — like getting a 20% bulk discount if they buy thousands of houses at a time from major homebuilders who are now having a tough time selling those houses directly to families or individual buyers.

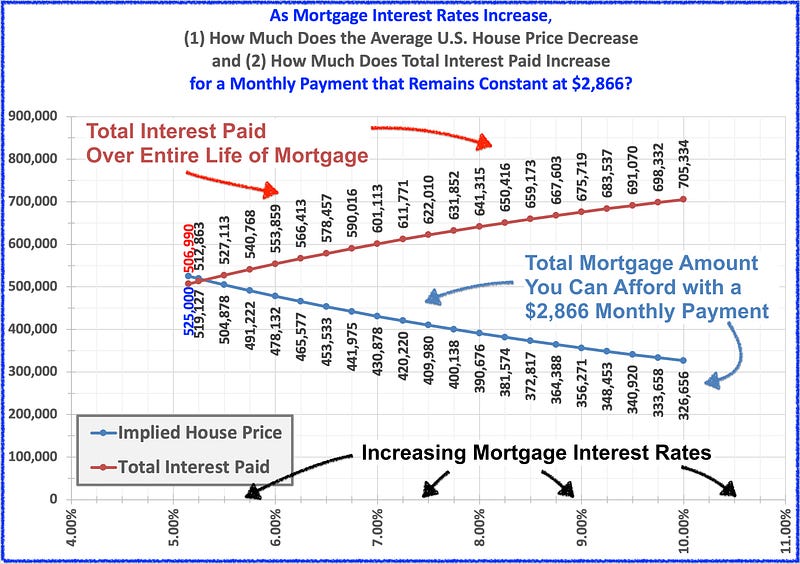

Part 2. The amount of house that a *fixed monthly payment* will buy decreases as interest rates rise

How fast, and how much might average house prices drop?

The average price for a house in the U.S. Q2 2022 is $525,000.

With the 5.15% mortgage rate back in Q2 2022, the monthly payment for someone borrowing the full $525,000 to buy the then-average house would be $2,866.64.

Remember this monthly payment number — $2,866.64. We’re going to keep using it, and we’re going to keep it constant.

Now assume that that $2,866.64 per month is the maximum that the average new homebuyer can afford. (And this assumption may not be that much of a stretch.)

Let’s look at how much house a person can buy as (1) interest rates go up AND (2) as we hold that $2,866 per month payment constant.

The question we’re asking is, “As interest rates go up, how much house will $2,866 buy?”

We know that the answer is “less” . . . but how much less?

The RED line is how much mortgage INTEREST you pay over the full life of the mortgage as interest rates go up.

The BLUE line is how much house you can buy with the $2,866 monthly payment as interest rates go up.

Here’s the really bad news:

With each quarter-percentage-point that the mortgage rate increases, (1) the purchase price of the house that you can afford with the $2,866 monthly payment keeps coming down . . .

. . . but (2) the total amount of interest KEEPS GOING UP substantially even though the purchase price keeps dropping!

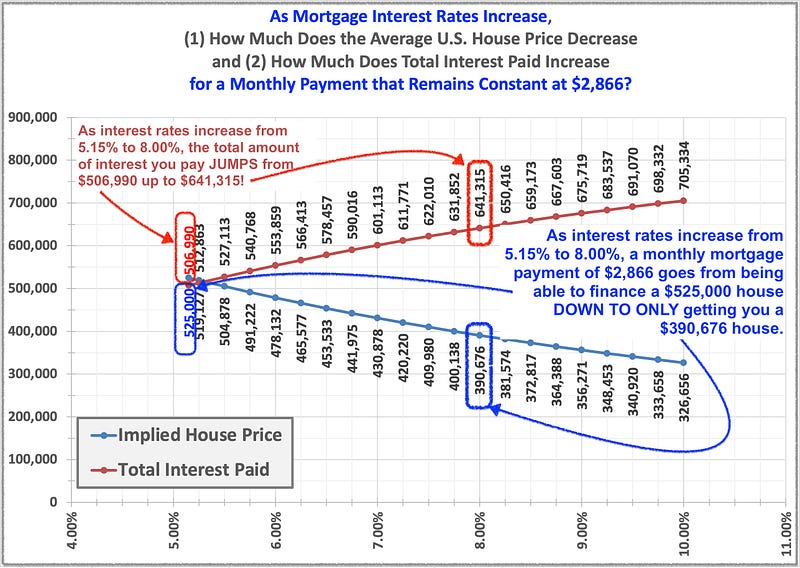

By the time interest rates have risen from 5.15% to 8.00%, your monthly $2,866 monthly payment will only buy a house costing about $390,676.

And right now, we’re only 1 percentage point away from reaching 8%.

That’s more than a 25% DECREASE in how much house you can buy with your $2,866 monthly payment as the interest for a 30-year fixed rate mortgage only rises from 5.15% up to 8.00%.

You can see in the chart above what all of this looks like as interest rates go up.

So what does this mean for housing prices in 2023 and 2024? It’s prediction time.

As interest rates either stay high or — more likely — go higher over the next year or two, housing prices seem likely to come down.

- We were in a housing market from early 2020 until late 2021 where (1) interest rates were constant at a very low level but (2) qualitative factors were driving prices higher. Those qualitative factors are now either disappearing or going into reverse.

- Now in the 2nd half of 2022, the housing market looks as though it will primarily be driven again by interest rates and by people’s ability to afford the monthly payment. Both of these will put negative / downward pressure on house prices.

Will we see the price of the average house in the U.S. go back to what it was before the pandemic?

If the average U.S. house in the U.S. early in Q4 2022 is still roughly at the same $525,000 level as back in Q2 2022, then a drop down to the $383,000 level from Q1, 2020 would be an average 37% drop nationwide.

Could housing prices drop that much?

Why not?

The factors pushing the average house price up from $383,000 to $525,000 were artificial and short-lived. And now they have either softened quite a bit or actually gone into reverse.

Matter of fact, I think there is a non-zero chance that the average price for U.S. housing could go BELOW that “starting point” of $383,000.

Remember:

1. Mortgage interest rates have gone up dramatically since early 2020. 2. The average family TODAY is far less able to afford the $2,866 monthly mortgage payment that today buys only a $430,900 house instead of the $525,000 house that the $2,866 bought just 21 months ago.

3. The economic, political, and military outlooks are now looking a lot tougher and scarier for the U.S and for potential homebuyers in terms of:

- jobs

- business growth

- high inflation

- supply chain difficulties

- trade wars

- actual wars

- the prospect of the U.S. being drawn into a nuclear war (with New York City taking this seriously enough that the city released a bizarre nuclear preparedness public service announcement video just 3 months ago.)

4. Be skeptical and suspicious when you read about economists who talk about “soft landings” or “only small decreases in housing prices.”

Look with a hard eye at who these economists work for. If they are working for the National Association of Realtors or the National Association of Homebuilders, be skeptical about what they say.

Be very skeptical.

They have a personal and professional interest in having people believe that housing prices are stable and will keep going up; that housing is always a great investment; and that housing prices never really go down much.

It may or may not be in YOUR interest to believe statements like that and to make big financial decisions based on it.

Related and recent articles

• Would We Be Smart to Ask These 3 Questions About the Housing Market? • What Are 4 Things Smart Homebuyers Do If Their Mortgage Rate Is Over 5%? • (Part 1) The 5 Most Important U.S. Economic Events Over the Last 50 Years • Did This Happen by Accident to 89% of America’s Stock Market Wealth? • Pressing Where It Hurts: How to Win Fights That Matter • Has U.S. Healthcare Really Become a Mob Protection Racket?

(Subscribe to receive email notifications when I post new articles.)

Again, thank you for reading, subscribing, clapping, and sharing — your time and attention are deeply appreciated!