Are We Heading Into an Uninsurable Future?

In times when climate change and global insurance markets collide, is there a place where we can truly find refuge?

Something happened today — as things do, in synchronicity — which put flesh on the bones of a post I’d been meaning to write.

A very good friend of mine was in town, so I invited him home for some mates (the shared Argentinian version of coffee).

“How are you?” I asked as we embraced.

“I’m going to be a dad,” he instantly said, euphoria and also despair evident in his eyes.

We talked for hours about the old days — we went to school together, grew up playing sports, and traveled the world, and I always admired him. We exchanged stories, traded memories, and reassured one another. Things would be OK. But I knew there were some pressing questions he had.

Recently, I’ve noticed a recurring trend among those who know and read my work. I can anticipate the difficult questions they will ask. And my friend was no exception.

One question that weighs heavily on people’s minds is, “Is it morally acceptable to bring a child into a world plagued by uncertainty?” Climate change, democracy, economy, uncertain peace, and even overpopulation -can we ignore the potential challenges our future generations may face?

The other question that arises, albeit with less emotional intensity, is, “Where should I live to ensure a habitable future?” Global warming is gradually shrinking the areas where human life can thrive, making this decision all the more critical.

When he left, I felt a wave of nostalgia wash over me. The old days. The world was different back then when we enjoyed absolute freedom, felt safer, and embraced an optimistic outlook.

And now — that feeling. What shall I call it?

The feeling of an uninsurable future.

The Cost-of-Living Crisis

We’re stuck in a vicious cycle of stagflation and inflation. On the one hand, prices are soaring, mainly driven by climate change. Sure, Covid and war in Ukraine played a role — but that’s in the past tense. On the other hand, our economies are stagnant.

“Growth” is mostly an illusion: the rich get richer, the rest of us struggle to survive, and incomes fall. Do you see any average person with too much money? Anyone not sending rockets to the stratosphere? I didn’t think so.

So, what’s behind this global cost of living crisis? Our old systems are failing. Growth rates have been dropping for years. Wealth is being sucked up by the elite, leaving the rest of us in a state of crisis. If there’s no real growth, it means wealth is being extracted — a concept often highlighted by Thomas Piketty known as “looting.”

The root of this issue? A lack of civilizational surplus. Surplus created civilization, leading to significant developments: from farmers to specialization to modern society as we know it — sciences, technology, art, literature. But now, we’re running low.

As we hurtle through the 21st century, it’s increasingly evident that the machinery of our global economy is careening off the tracks due to an unexpected obstacle: the climate crisis. Our relentless pursuit of growth has propelled us forward with unyielding force for decades, smashing through barriers (see: wars, pandemics, etc) like a speeding tractor-trailer barreling down a hill. But now, a formidable force threatens to slam on the brakes, sending shockwaves through our capitalist systems and societal structures.

The world’s wealthiest organizations can’t bear the risks and costs of catastrophe now. That’s what a lack of surplus means in complex terms. Systems begin to fail and crash. That’s what happens when you hit rock bottom, isn’t it?

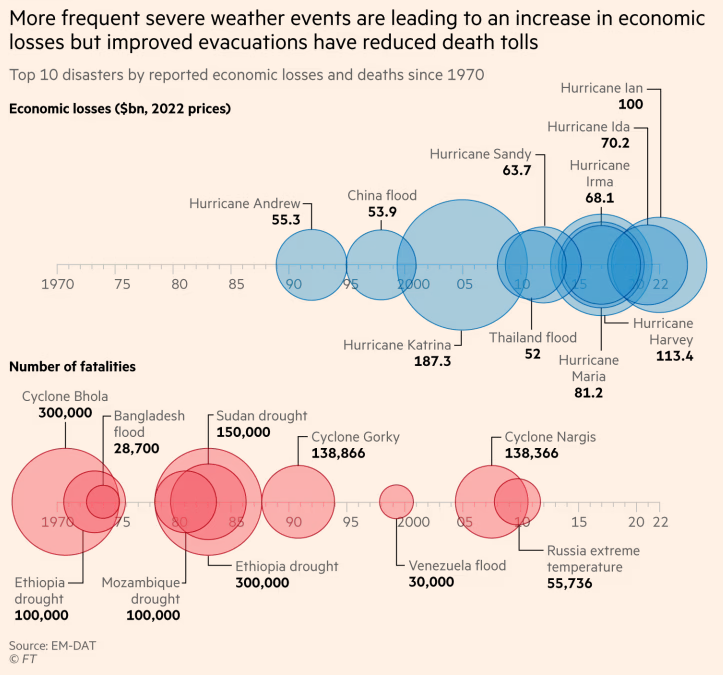

According to recent ground breaking research, half of our economies could be wiped out by 2070. This isn’t just a financial loss — it’s our future torched, drowned, incinerated, droughted, and flooded.

This research doesn’t come from mere “alarmists” or advocacy groups; it stems from the British Institute and Faculty of Actuaries, a credible and conservative source. They calculate risk, the backbone of the insurance industry. And they’re making it clear: climate change is a risk too big to bear.

“So, Where Should I Live?”

There’s a certain self-centeredness to this question— how do I avoid this collective disaster? There’s also a certain privilege as many people, particularly those most in need of relocation, lack the resources or legal means to move. Nonetheless, the question remains pressing: where can I find refuge in a world increasingly defined by uncertainty and environmental instability?

The Wall Street Journal recently highlighted the urgency of the situation, revealing that “Buying Home and Auto Insurance Is Becoming Impossible.” The reasons are unambiguous: has seen an onslaught of natural disasters fueled by warmer temperatures that intensify storms and worsen droughts.

The Journal was entirely clear about the likely consequences:

“Climate change will destabilize the global insurance industry,” research firm Forrester Research predicted in a fall report. Increasingly extreme weather will make it harder for insurance companies to model and predict exposures, accurately calculate reserves, offer coverage, and pay claims, the report said.

Millions of homeowners worldwide are on the front line of an insurance affordability crisis. As climate-related catastrophes become more frequent and powerful, they strain even the adaptive capabilities of developed nations, rendering vast territories uninsurable, overturning major investments, and crashing markets.

Actuarial tables, once the bedrock of risk assessment, falter in the face of uncertainty. Climate change, responsible for claiming millions of lives since 2000 and destabilizing our planet, is upending the reliability of our predictive models as we hurtle into uncharted territories. Not even the timely emergence of AI as a powerful forecasting tool can give a clear outlook.

The availability of affordable home insurance, often a crucial annual expense and frequently a condition of mortgage debt, is dwindling as firms exit some areas and demand higher premiums in others.

Why is this happening? The global picture explains why

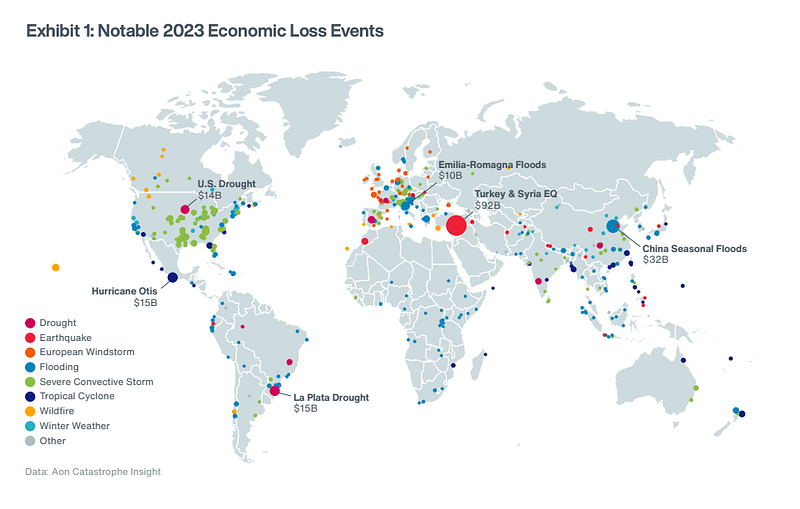

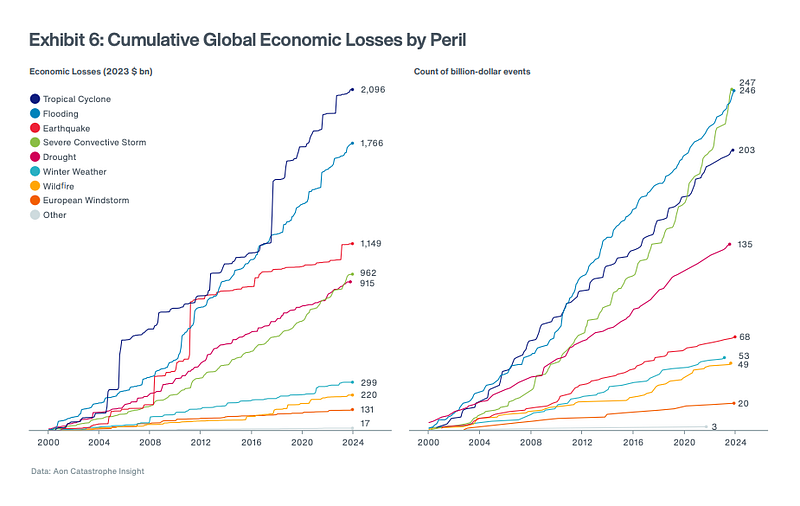

AON, a leading global professional services firm, published its 2024 Climate and Catastrophe Insight report, which identifies global natural disasters and climate trends to inform decision-making.

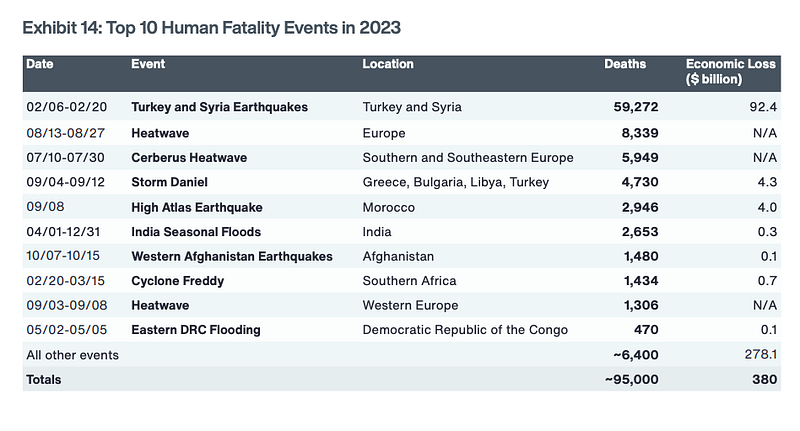

At least 95,000 people lost their lives due to global natural catastrophe events in 2023, which was well below the 21st-century average (71,430) and median (38,840).

The report reveals that 398 global natural disasters caused a $380 billion economic loss in the past year — against $355 billion in 2022 — a 22% increase from the 21st-century average. The main drivers were earthquakes in the Middle East, devastating wildfires, and relentless severe convective storms in North America and Europe.

Global insurance losses during the year were 31% above the 21st-century average, exceeding $100 billion for the fourth consecutive year, previously the mark of a remarkably bad year. Last year saw a record-breaking number of natural catastrophes causing at least $1bn in insurance losses: 37 separate events. Insurance only covered $118 billion (2022: $151 billion), or 31% of total losses, underscoring the need to expand insurance coverage.

The growing weight of catastrophes and the broadening of the areas that are exposed to them are raising anxiety in the sector and changing how risk is perceived.

It’s Easier to Figure Out Where NOT to Live

In the US, insurers have jacked up the rates to cover their risks. Big names like State Farm and The Hartford have even stopped issuing new home policies in California.

Phoenix might be the fastest-growing city, but anyone moving there after last summer's “month of hell” is not paying attention: 31 consecutive days of temperatures over 43°C / 110 Fahrenheit (!). People were burning themselves just by falling on the sidewalk.

But it’s not just obvious desert cities. In Europe, insurance prices are set to climb after a slew of extreme weather events.

In Australia, insurance has gotten so expensive that over 1.24 million households now face “home insurance affordability stress,” up from 1 million the prior year, according to the country’s Actuaries Institute. And according to the Climate Council, only 1 in 25 homes will be effectively uninsured by 2030. The country is on the fast track to becoming “uninsurable.”

In the Andes, at four thousand feet, temperatures exceeded 95 degrees (35°C) in…winter (described as “one of the extreme events the world has ever seen”). Athens, a city we often call the cradle of civilization, might soon be uninhabitable. During July 2023 and through the longest heatwave on record, authorities closed the Acropolis to afternoon tourists.

“You are seeing increasing numbers of people globally not insured because they cannot afford the premium,” says Mia Mottley, prime minister of Barbados. “And it’s not just people. You’re seeing it with businesses, and at some point, it’s going to become an issue with respect to access to and quality of their loans.” In her island nation, 95% of those affected by 2021’s Hurricane Elsa weren’t insured.

Life in India, used to dealing with extremes, is also getting more challenging, with the monsoon becoming increasingly more violent and unpredictable, causing over 100 lives lost each year.

There are examples all over the world. This recent study might sum it up: for every temperature rise of 0.1 degrees Celsius, another 140 million people live outside the “human climate niche,” the zone where humans thrive. 2023 was the hottest year on record, almost 1.5°C above pre-industrial levels.

Christian Mumenthaler, CEO of Swiss Re, one of the world’s largest reinsurers, said:

“This is the first time we actually bring a climate change bill back to the consumer, if you think about it. Rising insurance premiums were a kind of carbon price on consumers” with the higher costs resulting from “us living the way we’ve been living.”

The reinsurance market is also pulling back after years of underperformance, adding to the pressure on insurers to reprice. The cost of property catastrophe reinsurance cover is at its highest in a generation. Reinsurers have sharply raised their so-called attachment points — the level of losses that need to be reached for the reinsurance to kick in. If yearly losses stick above the $100bn level, and firms are forced into further price rises and pullbacks to protect their balance sheets, it could harm the whole proposition of the insurance sector to society. Swiss Re has predicted that there will be growing “patches” where buying insurance is uneconomical.

The private insurance sector alone can’t handle the cost of extreme weather. In the US, the UK, and other countries, a mix of state-backed insurers and national reinsurance schemes means taxpayers already share the cost of these risks.

The number of homeowners relying on California’s stripped-down Fair Plan has more than doubled from 2018 to 2022 due to escalating wildfires and traditional insurers backing out. In the UK, the Flood Re reinsurance scheme has stepped in, covering over 260,000 home insurance policies last year, from 150,000 in 2018.

Global regulators and policymakers are preparing for a scarier future. Uninsurable properties could cause other problems, like making mortgages harder to secure and increasing banks’ credit risks if homes are no longer eligible collateral.

The question now isn’t if governments will have to step in but how much they will compensate.

Amidst this turmoil, insurance companies are far from deserving of any sympathy. They not only find ways to charge higher premiums but have also played a significant role in creating this crisis. With their massive pool of investment capital, they have continuously funded the expansion of fossil fuels.

These same companies continue to support pipeline projects and LNG export terminals that contribute to their own downfall. A privileged few grapple with insurance woes, but the vast majority of the world’s population — predominantly in poorer nations — bears the brunt of climate-induced disasters without reprieve.

“Droughts operate in silence, often going unnoticed and failing to provoke an immediate public and political response,” wrote Ibrahim Thiaw, head of the United Nations agency that issued the estimates late last year, in his foreword to the report.

The affordability crisis has wide-ranging impacts.

I live in Bariloche, in the mountains of the Argentinan lake District in northwest Patagonia, a supposed “climate haven” because of its high latitude and altitude to avoid the worst heatwaves, isolated from a stormy ocean coast, and with for distinctive seasons. But last winter, we were flooded with five months of record rainfall, followed by severe droughts and destructive wildfires.

There’s no such thing as a safe place anymore.

And yet I remain glad I live where I do, close to my friends, the mountains, and the lakes that still protect us from…us.

As we grapple with this reality, we’re also battling rising “climate anxiety,” with Google searches on the term skyrocketing by 4,590% from 2018–2023. And this comes hand in hand with the insurmountable cost-of-living crisis. This is a new feeling, a new human experience. And a shared one.

It’s not a pleasant one, for sure. So it’s only fair to ask: what’s the point of a system like this?

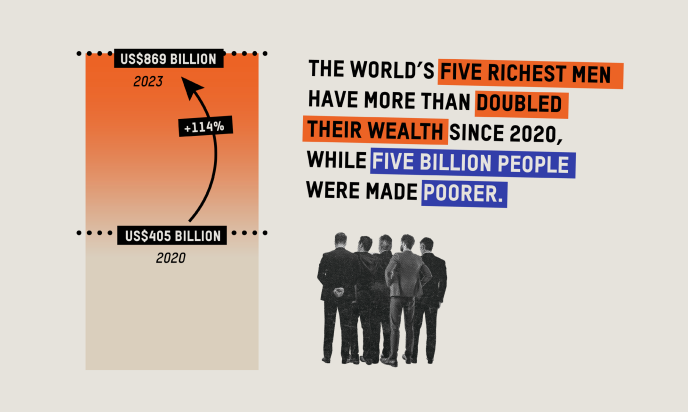

Just take a look at the data from the annual inequality report by Oxfam. The world’s richest five men have doubled their fortunes since 2020, while almost five billion people globally have become poorer. If each of the five wealthiest men spent a million dollars daily, they would still take 476 years to exhaust their combined wealth. At current rates, it will take 230 years to end poverty, but we could have our first trillionaire in 10 years.

What’s the logic or reason for more than half the world getting poorer? In contrast, just a tiny handful of people get so rich they could make every single person in the world (!) $417.72 better off, more than the GDP per capita of the poorest three countries in 2023.

This level of inequality is damaging to civilization every single, leading to what economists call a “deadweight loss.” The vast sums of wealth the uber-rich hold are not invested productively into what we desperately need as a civilization. Without relying on fossil fuels, we are clueless about producing food or manufacturing basic materials like concrete, steel, glass, and plastic. These carbon-emitting resources power the stuff and energy that thrusts our daily lives. So all that money in the hands of a few, who’d take hundreds of years to spend it — at the precise moment humanity’s at its greatest turning point? Not exactly a great idea.

As we grapple with those tough questions, we must remember: everything we think of as civilization comes from surplus, invested back into the common good. Insurance is based on the premise of continuing in perpetuity; we can always take a bet on the future, and if one person defaults, ten more can happily meet their premiums. But without that, who would bet on our future now?

So, the answer to my friend was clear. It is indeed acceptable and even needed for you to have a child, to invest your surplus as a parent, your opportunity to invest in the future. The world desperately needs fresh perspectives and innovative minds for a brighter future.

But when it comes to choosing a place to live, well, that’s a whole different story.

Be loud.

Thank you for your thorough reading and support! And once again, much deserved credit and gratitude to @TimSmedley for his invaluable feedback. Subscribe for immediate insights and join the 400+ Antarctic Sapiens community for weekly thought-provoking content.