The Two Levers of Financial Independence

Simplifying Personal Finance

Personal finance can feel complicated and intimidating. There are thousands of articles published every day, tackling different personal finance topics. From side-hustles to real estate, to investing the list seems endless. How is the average person supposed to keep track of it all?

Luckily when it comes to personal finance and reaching financial independence, all these discussions can be classified into one of two categories: the two levers of Financial Independence.

What are the two Levers of financial independence?

- Making more money

- Saving/Investing more money

Why these are the two Levers of Financial Independence

You have reached “Financial Independence” when your passive income you earn from investments is enough to cover your living expenses. This is the point where you are no longer dependent upon your job to finance your lifestyle.

Thanks to Mr. Money Mustache, we can predict when we might reach financial independence. We only need to know two things.

- How much money we are making

- How much money we are saving & Investing

If we know how much we make and how much we save & invest, we can calculate our savings rate, which tells us what percentage of our take-home pay we save and invest.

For example, if you cleared $5,000 per month after taxes and deductions and you were investing $500 per month, you would have a 10% savings rate.

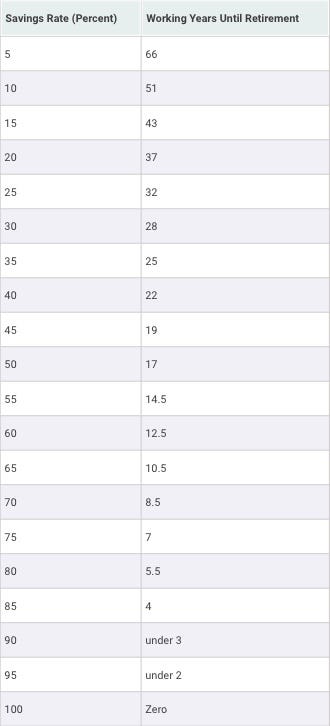

Mr. Money Mustache developed this simple chart that will tell you how many years it will take to reach financial independence, given your current savings rate.

If you have a 10% savings rate, you will reach financial independence in 51 years. If you have an 85% savings rate, you will achieve Financial Independence in four years.

(Note: The math in this chart assumes you are starting from scratch, and you can earn 5% above inflation on your investments.)

How the two Levers fit In

There are only two ways to increase your savings rate and reach financial independence sooner.

- Make more money (and maintain your current lifestyle).

- Save/invest more of the money you are currently making.

If you want to reach financial independence quicker, you will need to pull one or both levers.

Pulling the Income Lever

The more money you make, the easier it will be to reach financial independence. The higher your income, the more money you will have leftover after paying for the “big-3” living expenses: housing, transportation, and food.

Let’s say you rent an apartment that costs $1,500 per month, have a $300 per month car loan, and spend $400 per month on groceries. That’s a total of $2,200 per month spent on housing, transportation, and food.

- If you make $50,000 per year, your monthly take-home pay will be around $3,400. You would be spending 65% of your take-home pay on the big-3 life expenses.

- If you make $100,000 per year, your monthly take-home pay will be around $6,200. You would be spending 35% of your take-home pay on the big-3 life expenses.

In this example, you could reach financial independence 18 years sooner by increasing your income from $50,000 to $100,000 per year.

Ideas to make more money

- Pick up a side-hustle

- Ask your boss for a raise or earn a promotion

- Upgrade your skills and look for a higher paying job

- Start a business

The 10% Rule

How to achieve financial freedom in less than 10 years starting from scratch

medium.com

Pulling the Saving/Investing Lever

While it is easier to reach financial independence making a lot of money, it is not a requirement. What I love most about the concept of financial independence is that it focuses on saving. This means that if someone is smart and willing to sacrifice, they can achieve a high savings rate and reach financial independence, even if they don’t have a high income.

Let’s return to our example where the person making $50,000 per year spent 65% of their take-home pay on the big-3 life expenses. With a frugal mindset and a willingness to make a few sacrifices, these numbers can look a lot better.

- Rather than living alone in that $1,500 per month apartment, getting a roommate could cut housing costs in half to $750 per month.

- Trading in the car and it’s $300 per month payment for a $50 per month transit would reduce transportation costs to $50 per month.

- Being a little more frugal on food choices could shave off $100 from the monthly grocery budget, bringing the cost of food down to $300.

That’s a total of $1,100 per month spent on housing, transportation, and food.

The non-frugal person making $50,000 per year spends 65% of their income on the big-3 life expenses, while the frugal person making the same amount of money is only spending 32% of their take-home pay on the same costs.

In this example, you could reach financial independence 18 years sooner by cutting your expenses in half. Note that this has nearly the same impact as doubling your income does.

Ideas to Reduce your Living Expenses

- Be smart with your housing

- Cook your own food

- Be efficient with your groceries

- Don’t spend too much on a car

Putting it all Together

Personal finance and financial independence can be a pretty simple concept if we let it be. Every action you take on your finances can be boiled down into one of two actions.

- Making more money.

- Saving more of the money you currently have.

Achieving Financial Independence is all about increasing your savings rate. Being more efficient with the money you already have and increasing your take-home pay are both excellent ways to improve your savings rate and move closer to financial freedom.

Learn How the 2-Levers Of Financial Independence Fit Into Your Budget

If you want to go more in-depth on the concept of the two levers of financial independence and how pulling each lever can help you balance a budget that focuses on your savings goals, you may want to enroll in my personal finance masterclass on Skillshare, where you will learn the 6-steps to creating a budget that locks in your financial goals.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.

In the interest of full disclosure: If you use the link in this article to enroll in my personal finance masterclass and end up signing up for Skillshare, I receive a referral fee from Skillshare. It does not cost you anything and, in fact, gives you two free months to the platform, but I thought you should know.