The Emergence of Decentralized Finance

DeFi will replace the centralized legacy financial system

The current global financial system has created enormous amounts of wealth for the people with resources, knowledge & access to the financial centers around the world. At the same time, events like the housing crisis of 2008–09 has not only caused massive hardships for the common man & rich alike, it has eroded the confidence of the general populace in the current system.

Until the above mentioned financial crisis happened, there wasn’t an alternative to the shaky centralized financial system, but in the last decade, a new decentralized financial model has emerged — one which has been enabled by technology, driven by innovation with the immense need for inclusiveness for the less privileged.

Technological Developments

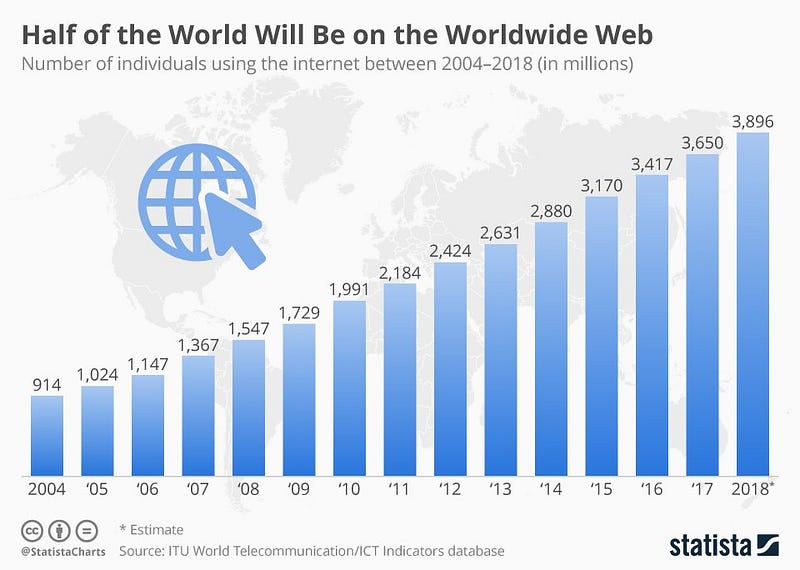

- Internet (the Early 1990s) — A research project (ARPANET) initiated in 1969 went on to become the underlying global communication tool for the masses. The World Wide Web today provides democratized access to information at your fingertips. According to the International Telecommunications Union, almost 4 billion people (or about 51%) of the global population has access to the Internet by the end of 2018, and the number is only growing.

- Smartphones (2007) — The first decade of the 21st century saw the smartphones explode on to the scene. While the cell phones had been in existence way before this, smartphones changed not only how we communicate but the way we conduct our daily lives & businesses. As reported by the World Bank, the two-thirds of the roughly 1.7 billion unbanked population of the world have smartphones, giving them the ability to be a part of the emerging financial system.

- Digital banking (1994) — With the proliferation of the Internet & ease of access and usability people have become more comfortable with handling their finances online. The traditional brick & mortar financial institutions have been offering digital banking, which has evolved over time to include a wide spectrum of services. Juniper Research states that Digital banking users have reached 2 billion in 2018.

- Digital Ledger Technology (2008) — Perhaps the single most important factor that has contributed the most towards this transition has been the rise of DLT (Digital Ledger Technology) and the associated Cryptocurrencies/Digital assets like Bitcoin. The public blockchains function on the central theme of decentralization. We will discuss the features of the public blockchain a little later.

- Fintechs (1998) — Following the convergence of DLT towards the Financial ecosystem, another innovation in the form of stand-alone financial technology companies (Fintechs) emerged on the scene and has taken the world of finance by storm in the past few years. These Fintechs are reshaping the existing ecosystem into one which serves the needs of the new tech-savvy consumer. The products & services are being catered to the needs of the growing segment of Millennials & Generation Zers.

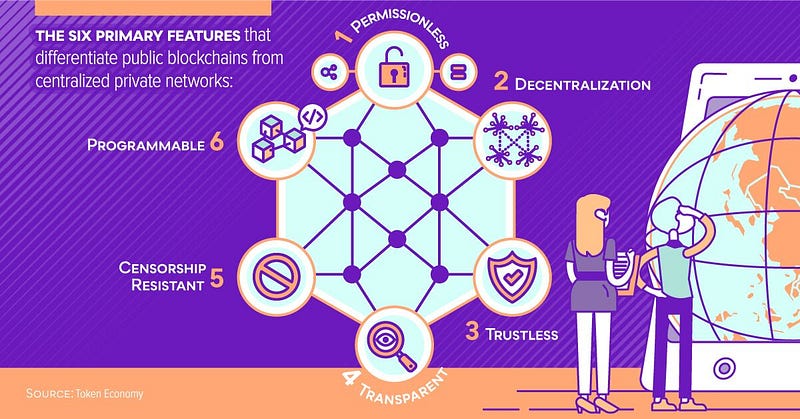

Public Blockchains VS. Centralized Networks

Let’s review some features of the decentralized networks that make it so favorable for the new model.

⇒ Decentralized — Records are kept on thousands of computers around the World called nodes instead of a central server which is much more prone to a malicious attack.

⇒ Permissionless — There is no restriction to entry in the network, anyone in the world can have access to & be a part of the blockchain. Unlike the current financial system, wealth, location & status are not the prohibiting factors.

⇒ Trustless — A central authority is not required to validate transactions on the network. All the participating nodes do this job whereas central banks, governments & certain authorized financial entities only perform these functions in the current financial system. No wonder among the different sectors of the global economy, financial services are the least trusted one by the people.

⇒ Transparent — Since the blockchain is a public network, the transactions are public and easily auditable which brings a layer of transparency to the process. In the central financial system, nothing is open to the public & the accountability process is shady at best.

⇒ Censorship Resistant — For the decentralized networks, no one party, entity or node can invalidate transactions, reverse changes or shut down the network entirely. In a centralized financial system, like the one we have currently, the governments have the power to manipulate it which can have devastating effects on the financial markets & the lives of the people.

⇒ Programmable — Developers can program business logic into low cost and interoperable financial services. Rather than implementing a whole new system, technology can be deployed in intuitive ways to solve the problems. The current systems employ tardy & cumbersome processes that are difficult to rewrite & expensive to replace.

Impacts of Decentralized Finance

- The biggest impact of the new decentralized model will be the inclusiveness it will bring to the people, by bringing wider global access to financial services. Fintechs are & will continue to play a pivotal role in this endeavor. Anyone with an internet connection and/or a smartphone can access financial services. A Hedge Fund Manager at a Top financial firm in the U.S or a farmer in a remote region of Africa will have the same level access. Barriers like wealth to invest, distance from functioning economies & lack of documentation would diminish.

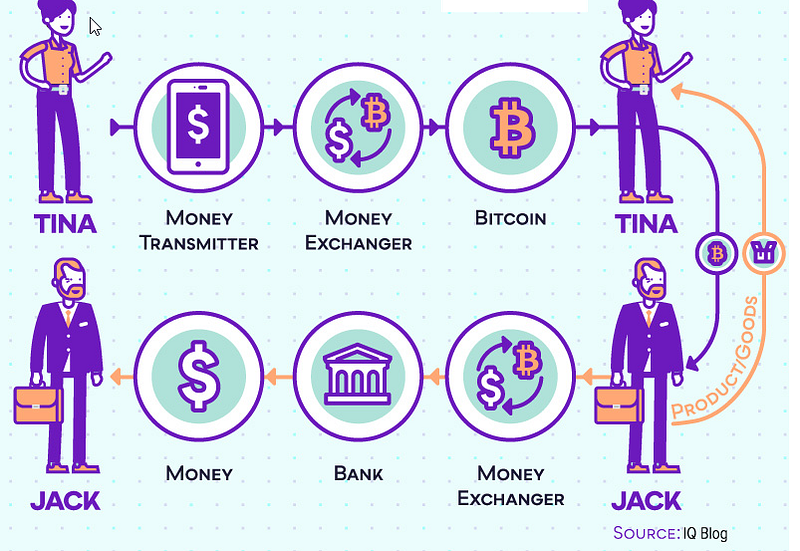

- Removal of intermediaries will be the other big advantage of the new model. The remittance services will become much cheaper for the global population especially for people living overseas and have to send money home regularly. According to the World Bank report, the global average remittance fees is around 7% significantly higher than the G-20 objective of 5% & and the UN Sustainable goal target of 3%. International money transfer Apps like Xoom, TransferWise & WorldRemit are some of the examples of the remittance services that are making cheaper & faster overseas remittances possible.

- Major improvement in the Privacy & Security of consumer data. Decentralized finance does not require the validation of a central authority to transact securely. A malicious actor won’t be able to steal anything as long as the clients have control of their private key. While in the centralized system, clients’ information resides on a central server at a single physical location which can be a target of repeated & reinforced malicious attacks.

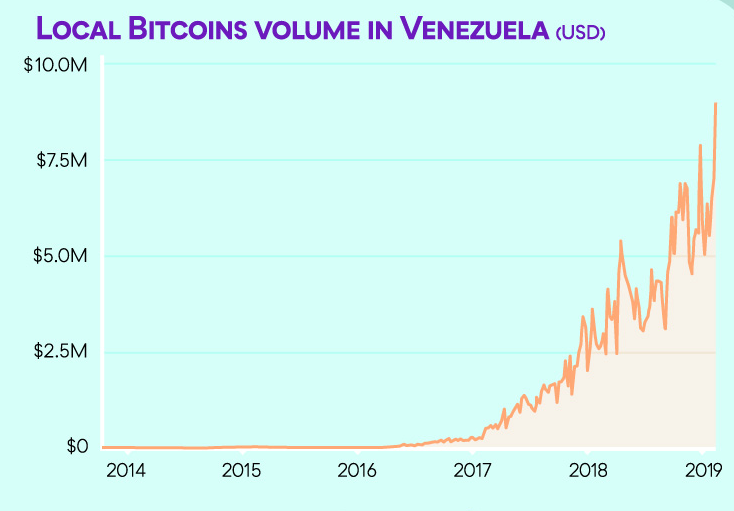

- The immutability of the decentralized networks gives it the ability to defy any shutdown attempts by anyone. In countries with poor governance & authoritarianism, the governments use the central authority to financially censor their citizens by freezing accounts, removing funds, denying access to payment systems, etc. The citizens can use the decentralized financial system to protect their wealth & lifelong savings. The most glaring example in this regard is Venezuela, where runaway hyperinflation resulted in a complete loss of trust in the country’s fiat currency, caused a recession, evaporated people’s savings & increased crime rate resulting from a sky-high unemployment rate of 39%. Venezuelans have turned to decentralized digital currencies like Bitcoin, Dash & others trading on exchanging them on peer-to-peer (P2P) market places like LocalBitcoins (chart above).

- The simplicity of use is the greatest convenience that the decentralized financial services have brought to people. The Plug & Play apps on your smartphone let you use the services intuitively without the complexity & time-consuming constraints of the centralized system. The decentralized system would allow a woman in China to receive a loan from an online lending platform in the U.S to invest in a business in India while paying off her debt at home, through All-in-one interoperable apps.

It’s still a long road ahead though. Unless the Governments & Central banks vanish overnight, the best-case scenario looks like a gradual shift from the current centralized system to a decentralized financial ecosystem. In the intermediary period, an ideal scenario would be the interactivity of the two financial systems — Public blockchains working in tandem with the centralized financial system to create a hybrid model.

Users could conduct their economic & investment activities on the public blockchains & exchange their wealth on the centralized system. This can also provide a hedging opportunity for investors who can diversify their portfolio by having holdings in both the systems, thus reducing the systematic risk. Best of both worlds?

Email📭| Twitter📜 | LinkedIn📑| StockTwits📉 | Telegram🔗

Recent Articles:

Originally published at www.datadriveninvestor.com on March 14, 2019.