The rise of P2P Finance model

An Overview of the Peer-to-Peer Finance Model

The Global Financial crisis of 2007–08 in the U.S changed the global financial landscape dramatically resulting in the disruption of the conventional models of finance. The rapid devaluation of financial instruments like mortgage-backed securities (MBS) & credit default swaps either precipitated the collapse of many financial institutions or they needed to be bailed out by their respective governments.

As lending dried out from the traditional financial channels caused by the extreme credit crunch, governments encouraged the emergence of new players & business models to provide alternative finance solutions to retail & institutional lenders. In the U.S the Jumpstart Our Business Startups (JOBS) Act legitimized the concept of Equity crowdfunding to a law — marking the birth of the era of distributed Peer-to-Peer finance model.

Many other countries followed in the footsteps of U.S. passing crowdfunding laws to stimulate innovation by allowing direct investments into early stage startups thus helping to bypass the sole reliance on Venture capital (VC) firms & high net worth individuals. According to a 2013 World bank report crowdfunding investments will reach $96 billion by 2025 in developing countries alone.

In essence, financial analysts have predicted Crowdfunding to be the most disruptive of all new models of finance. This new model of Equity Crowdfunding led to the so-called democratization of finance where middlemen like stockbrokers, dealers or even the banks had no role anymore. Equity Crowdfunding, however, was just the first of the many financial instruments to follow that would utilize this new distributed P2P finance model.

The market for Debt Crowdfunding or P2P lending was considered an even bigger market for the new finance model since it included the personal finance sector as well apart from the unsecured business & SME (Small & Medium Enterprise) loans. This form of lending gained a lot of popularity among the public after the loss of trust in mainstream banks due to the preceding financial crisis. The governments also became supportive of this alternative form of finance.

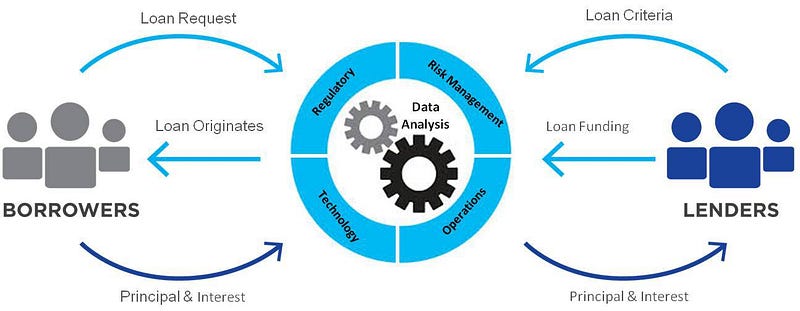

The concept behind P2P lending is simple. In a low-interest environment, especially the one that existed after the financial crisis of 2007–08 savers sought alternative forms of investment when the banks had reduced their lending. An online platform would provide a matching place for prospective borrowers & lenders. The lenders would benefit from a higher rate of return due to low overhead costs and the lenders would benefit from quick & easy access to the funds thus a win-win situation for both parties.

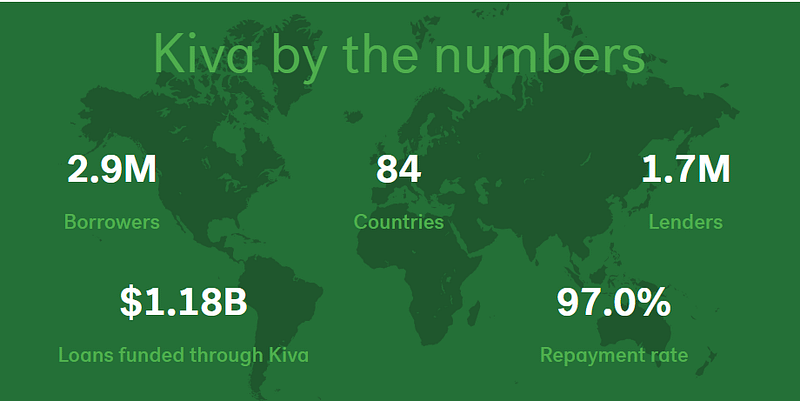

This concept is similar to a micro-lending platform Kiva which helps individuals in the rural communities of the developing countries. Kiva is a U.S. based crowdfunding platform that has been successfully helping people like low-income entrepreneurs, small-scale farmers & students among others in developing countries since 2005.

In the United Kingdom, platforms like Zopa & Funding Circle while in U.S startups like Prosper & Lending Club grew exponentially giving a huge boost to P2P lending. Lending Club also became the first leading P2P company to IPO in 2014.

Of course, there were challenges associated with this business model like any other emerging technology-driven solution. Since there were no government regulations or guarantees the question arose — How do you know if the individual/s or the business will repay the loan? Initially, it was addressed by shortening the tenure of the loans & some platforms even introduced secured loans and trust accounts.

However, things finally started to change in 2008 in the U.S when the SEC (Securities & Exchange Commission) extended its jurisdiction to such P2P lending platforms. This regulatory enforcement gave way to two trends — First, different categories of loans emerged (student loans, payday loans, business loans, etc.) on specialized platforms & secondly, individual lenders were dwarfed by institutional lenders which transformed this sector from Peer-to-Peer lending to be called Marketplace lending.

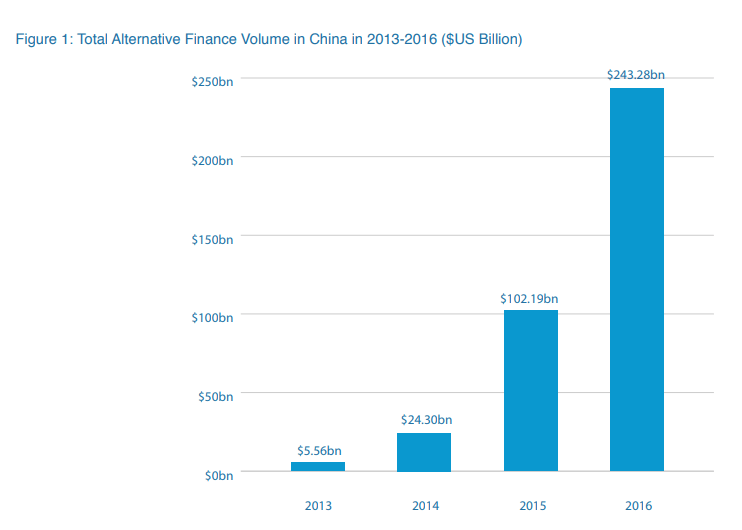

Meanwhile on the other side of the spectrum — with little to no regulatory enforcement, a growing middle class & a lack of investment alternatives the P2P market in China exploded as per the chart above. It was not until 2015 when the West realized that the size of loans originated and the number of borrowers in China dwarfed even the largest U.S. based P2P platforms.

However, this unchecked exponential growth of P2P lending platforms in China came with its own set of problems when 2016 Blue Book of Internet Finance found 1263 (almost 1/3 rd) of China’s platforms as problematic. Since then China has been tightening the noose around these P2P companies with rules & regulations, requiring custodian banks to be appointed & imposing borrowing and interest caps.

The new generation of P2P lending companies is moving away from being lending only platforms to provide more innovative solutions like credit analysis & the social media usage analysis and online purchase patterns studies of customers that can be used by traditional banks & related financial companies.

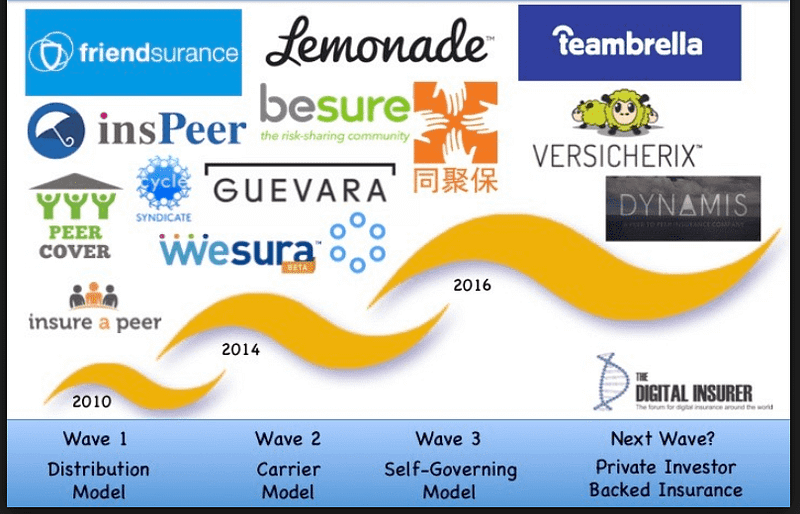

P2P Finance model has spread its wings to all sectors of the Economic spectrum with P2P insurance undergoing a major transformation within the last few years going from a distribution model to a self-governing model as depicted in the figure below.

Here are a few other examples of developing P2P marketplaces:

LocalBitCoins — A decentralized P2P digital exchange which provides a platform to millions of its users in more than 200 countries to buy & sell bitcoins absolutely free of charge — their tag line reads — Instant. Secure. Private.

Openbazaar — Also a peer-to-peer based online marketplace where people can exchange goods & services without charging or being charged any fees or the involvement of any intermediary.

VoltTech — An upcoming P2P based delivery service that I had a chance to study. It aims to disrupt the existing Hub & Spoke based delivery services like UBER & DHL. It claims it’s efficient, secure & transparent peer-to-peer model is the answer to meeting the growing needs of the same day delivery service.

Apart from paving the way for a fair & competitive market place & challenging the monopoly of the finance giants, the evolution of P2P lending platforms has provided useful lessons for the development of the current darlings of the distributed P2P models of finance — Cryptocurrencies.

Related Articles: Blockchain, Cryptocurrencies & the shifting Paradigm, Cryptocurrencies reviving Agorism, Bitcoin is still the Crypto kingpin, Mainnets… the new Revolution in Cryptos

Email📭| Twitter📜 | LinkedIn📑| StockTwits📉 | Telegram🔗

Originally published at www.datadriveninvestor.com on July 31, 2018.