Stop Eating at Restaurants

They’re stealing your financial freedom

No. Actually, pizza is not essential.

Nice slogan, though.

Like so much consumer marketing it’s designed to do one thing — take money out of your checking account and put it in somebody else’s.

Support Local Business? Support Yourself First.

The push to support local businesses, particularly restaurants and bars, became an unfortunate element of life dominated by a global pandemic.

Please allow me some safe space to explain.

I took a four-year hiatus from writing to work in hospitality. When the pandemic shut things down in mid-March, I was running an iconic craft cocktail bar on Melrose Avenue in Los Angeles.

I worked with incredible people, learned a ton, and most of all, fell in love with providing hospitality. I even wrote about it a bit, blending it with another one of my passions — Bruce Springsteen and his legendary live performances:

As bartenders, we can treat each shift as nothing more than the task of making a bunch of drinks. We have large enough menus and compendiums to draw from. Or we can treat each shift the way Springsteen treats each show. With a determined intensity and an unbridled enthusiasm to give his guests more than they came for, to deliver an experience they’ll remember and want to have again. To make them feel alive, connected, and socially valuable. To make them feel like they did something much more meaningful than merely walk into a bar.

So I more than appreciate restaurants and bars as social spaces. I understand the role they play and the value they provide in cities and communities.

I also know firsthand these establishments run on razor-thin margins. The worst thing about running a bar, after having been an hourly bartender myself, was the need to mercilessly control labor costs. It’s a tough business.

Many restaurants and bars will not reopen. Quite a few have already called it quits.

The pandemic should be — and hopefully has been — a wake-up call to restaurant and bar owners.

Consider this blurb from an Eater LA article about Osteria la Buca, a popular Italian restaurant in Los Angeles:

Osteria la Buca had not yet begun to offer dine-in services to its customers, relying instead on a limited menu of Italian staples for takeout and delivery, as well as pantry goods, grocery items, and online alcohol sales. (Owner Stephen) Sakulsky says the restaurant has done well financially in its 15 years, and reopening more fully isn’t a top priority right now. “We’ve had the luxury of building a rainy day fund,” he says, “That’s why we do these things, so we can be prepared for this.” (bold emphasis added)

You don’t hear that too often. A restaurant with a rainy day fund.

Every restaurant or bar that survives this mess should make establishing a “rainy day fund” priority number one. Nobody — proprietor or investor — should enter a new venture without enough cash in reserve to weather, at the very least, a year-long storm.

The pandemic made it clear — the restaurant and bar industry needs to better situate itself financially.

Being in a tough business with slim margins isn’t an excuse to not do so.

It is reason to do so.

From an individual standpoint, the pandemic provided many of us an opportunity to spend less, increase savings, and practice more sound personal finance. Some people had no choice due to reduced income or job loss. Others discovered they prefer spending less money on ephemeral things.

In April, the savings rate in the US hit an all-time high. Of course, fewer places existed for us to spend our money. Hopefully, the forced frugality will lead to new, financially healthier habits and routines that endure.

If you were operating under the equivalent of slim margins — living paycheck to paycheck and financing life with credit cards— staying at home gift-wrapped a chance to pay down debt, stock an emergency fund, and maybe even start investing.

I’m spending $1,600 per month less on food and drink than I was before the pandemic.

I’m not going back.

I’m ashamed of how much money I threw away in restaurants and bars.

That level of spending in just one budget area was literally taking decades off of my quest for financial freedom. I can’t overstate the wealth-building effects of an additional $1,600 (or thereabouts) saved and invested each month.

Let’s say you have $20,000 to start, you add $500 a month to that nest egg, and see, on average, a 5% annual rate of return. In ten years, you’ll have accumulated $109,759.47.

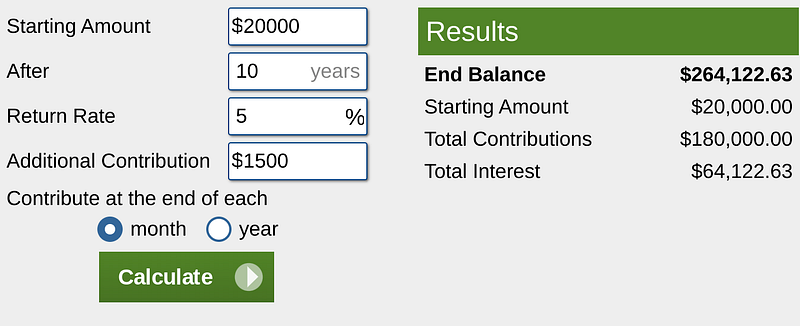

If you take just $1,000 of that $1,600 and add it to your $500 monthly contribution, you more than double your money:

And that’s with the conservative assumption of 5% growth and no dividend reinvestment.

Up the return to 8% and your nest egg grows to $313,364.91 over ten years.

Plug the same numbers into a portfolio of dividend-paying stocks with a modest yield (4%), super conservative dividend growth (1%), and dividend reinvestment and you’re sitting on $384,304.96 come year ten.

You get the picture.

The power of saving and investing at this level —irrespective of strategy —should astound you. The earlier you start and the more cash you have free to save and invest, the more dynamic the numbers.

Heck, if you didn’t even invest that extra money. If you just put $1,000 in a box every month for ten years, you wind up with $120,000.

Don’t Feel Guilty Over Putting Yourself First

We’re socialized to believe that “going out” must be the center of our social universe. But why does excessive spending on food and drink have to be the cornerstone of this lifestyle?

Other ways to “go out” exist.

It’s not uncool to be frugal.

In fact, it’s the smartest choice you can make. And you absolutely can have a fun life alongside frugality and financial responsibility.

Just as the pandemic helped some of us improve our financial situations, it presented a new way of, as the sociologists say, doing life.

A $4 coffee and urban walk or hike over a $40 brunch. A couple of beers with a friend in the park over $15 cocktails. An evening at the beach with snacks over expensive oceanfront dining.

I’m having a ton of fun making these choices. And I’m wealthier in the process.

We experience all kinds of social pressure.

In an indirect way, spending too much money on food and drink is one. But it has a direct impact on your financial well-being and future.

During the pandemic, we’re almost made to feel guilty if we don’t support restaurants and bars. It will probably get worse once they fully reopen.

But know this — there’s always going to be someone who (over)supports local business. It doesn’t have to be you. You don’t have to be a regular. You don’t have to be out every single day and night of the week. You don’t have to order takeout at abnormal rates — something that has become akin to civic duty.

People who achieve financial freedom tend to not follow the crowd. The crowd overspends. The crowd follows the crowd thus creating the crowd.

You choose your lifestyle.

Straightforward Steps To Making It Happen

You don’t have to go all-in all at once.

Start small. Log in to your checking account. Determine how much you’re spending on food and drink. Most banking apps categorize your spending for you.

Redirect a portion of your restaurant and bar outlays to groceries (you still have to eat) and your personal finance.

Pay off credit card debt first. Doing so alongside reduced food and drink expenses amplifies the effects.

Fill an emergency fund. Set aside enough money to cover a few months without income due to unforeseen events, such as those caused by, say, a global pandemic.

Invest the rest. Buy stocks in established companies that, preferably, pay dividends. Do so with as much vigor and conviction as you have when you say “this round’s on me.”

Making the choice to spend less and save and invest more represents a seismic lifestyle change for the better. You should feel pride, not guilt or shame.

It’s cool to care about building wealth and your financial future.

Find people who share your ideals. Stick with them. And stick to your ideals.

You’re useless in other aspects of life if you’re stressed about money.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions