How I Cut My Spending By $1,600

A look inside my bank account

I’m actually embarrassed.

I ran the numbers comparing my pre-pandemic spending to my monthly outlays in quarantine. The results shocked me more than I expected.

That’s my friend, Nicholas.

His reaction looks a lot like mine when I saw my spending data.

I was like, “um, wow” and I promptly needed a shot. Though I didn’t take one.

Enough delaying the inevitable. Here we go.

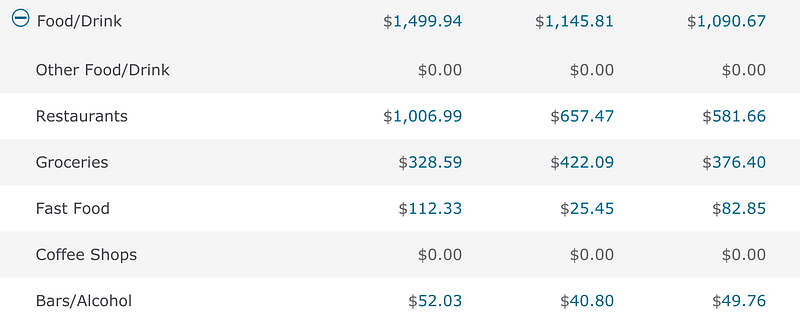

From January through March 2020 (which includes two weeks of lockdown in Los Angeles), I spent $3,736.42 on what Wells Fargo categories “food and drink.”

From April 2020 through June 2020 (all under quarantine), I spent $2,125.65 on food and drink.

That’s a decrease of 43.1 percent, or $1,610.77.

As you might expect, I spent the majority of my pre-pandemic food and drink money in restaurants:

- January through March restaurant spending: $2,246.12

- April through June restaurant spending: $349.90

During quarantine, my restaurant spending plummeted 84.4 percent.

Quick note — I don’t eat fast food. Wells Fargo appears to have categorized the coffee shop I frequent as “fast food.” But this actually brings up a good point.

I’m not willing to give up my coffee runs

I’m all about cost of living and how a low cost of living gives you the ability to save/invest more and the flexibility to live and retire how and where you want. How we control our cost of living comes down to the choices we make.

I choose to continue to spend on coffee. I think (maybe rationalize) that the social experience of acquiring coffee and chatting with my favorite baristas makes me more productive. It’s a trade-off I’m willing to make.

Money in exchange for what I feel like I’m getting out of it.

However, when things return to “normal” (as in, it’s safe to eat at a restaurant), I know I’m not going back to my old food and drink habits.

I absolutely get something out of drinking beers, doing shots of soju, and eating Korean food with Nicholas. It’s a social experience. We need these things. But I will go about getting them differently post-pandemic.

Because $1,600 is a lot of money.

Investing $1,600 more a month can put you ahead by years, if not decades, as an investor.

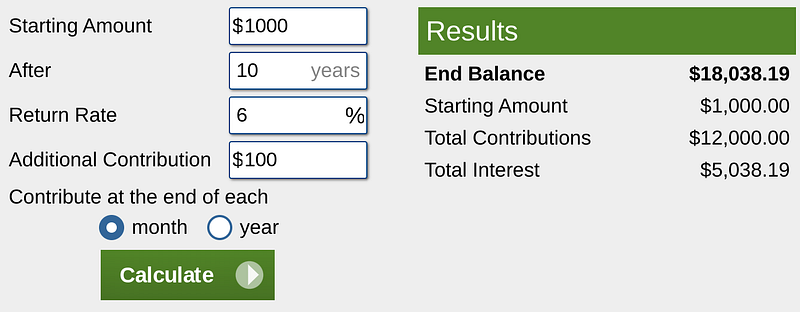

Consider the basic math.

That’s you starting with $1,000 and adding $100 a month to it, at a six percent rate of return, over ten years. You end up with $18,038.19.

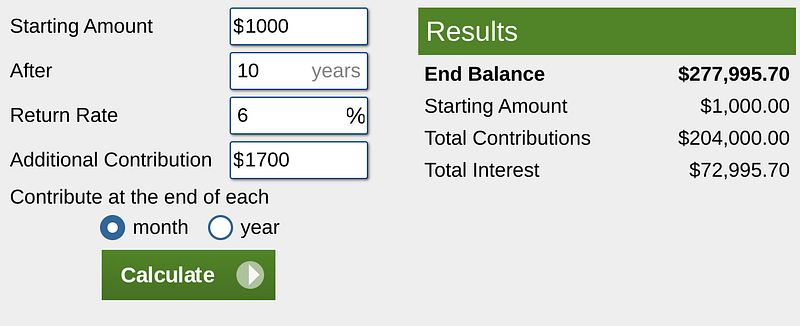

Here’s what that math looks like if you change just one thing. You invest $1,700 a month instead of $100.

In this scenario, you end up with $277,995.70.

That’s nothing short of stunning. And it makes me want to do what we’re doing during quarantine life — meet Nicholas in the park with a $10 burrito.

It’s common sense.

If I have $277,995 ten years from now I give myself infinitely more options than if I have $18,038.

You can also look at it from a single stock perspective.

Think about Apple.

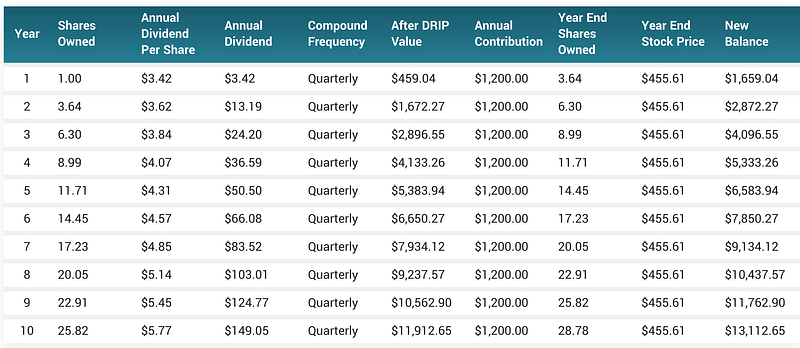

As I write this, the stock costs $455.61 per share. It pays an annual dividend of $3.28 per share. Last year, Apple raised its dividend by six percent.

If you opt to reinvest those dividends (and you absolutely should), you will buy more Apple stock with that money in addition to any incremental buys you make along the way. These actions will increase your position size and continually increase how much you collect in dividend income.

At the moment, one share of Apple generates $3.28 in annual dividend income. Two shares brings in $6.56. One hundred shares produces $328. And so on.

Let’s look at the magic of dividend reinvestment and consistent, monthly buys in a stock like Apple. We’ll assume that Apple’s stock price remains static, never moving from $455.61 during a ten-year time frame.

While this is imperfect (because you will be able to buy less Apple as the stock price moves higher and more as it moves lower), we’re doing this for broad and still powerful illustration purposes.

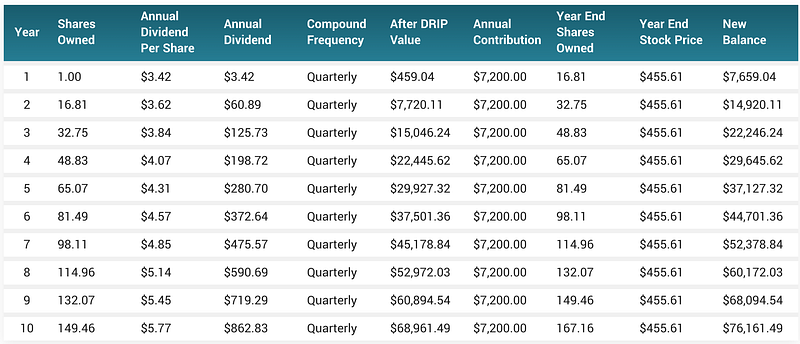

So you start with one share of Apple, reinvest all dividends, assume dividend growth of six percent, a static stock price, and $100 monthly additions to your position over ten years. Here are the results.

In year ten, you’re sitting on $13,112.65.

Now, we’ll up our monthly investment to $600. Essentially, we take part of that $1,600 we’re not spending on food and drink and invest it in Apple.

In this scenario, you’re sitting on $76,161.49 in year ten.

Imagine what we could do if we invest that remaining $1,100 in food and drink savings in a slew of other stocks, creating a diversified income-focused portfolio.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.