No One Should Pay Assets Under Management Fees. Ever.

Like being robbed? Find an Advisor that charges Assets Under Management Fees!

I have covered on this blog the aspect of fees, specifically how mutual funds tend to be magnitudes more expensive to own than a simple ETF that tracks the S&P 500.

Keep in mind, most of the holdings will be identical to, or very similar, so paying more for managed funds (which is what mutual funds are on average) makes zero sense unless you don’t have the option, say in a 401(k).

Most financial advisors will happily push you into managed funds, that surprise, they make money on. But for this article, I want to focus on fees applied to Assets Under Management (or AUM).

Most investment advisors, be they a CFP, CPWA, CWS, or WMCP, will ask you for compensation in the form of a percentage-based charge, on an annual basis, against the total amount of dollars in the investment account or accounts being “managed”.

Let’s set aside the fact that in 2023, it really is inexcusable to not understand what your investment options are, or what historically has been the best place to put your money.

My fellow writer and thinker Denis Gorbunov does a very nice job of laying out this fact.

Given easy access to sites like Medium, podcasts, and even some YouTube channels, seeking an investment advisor strictly to settle the question of allocation seems silly to me. Just do some homework!

But let’s look at the real crime of the fees associated with most investment advisors.

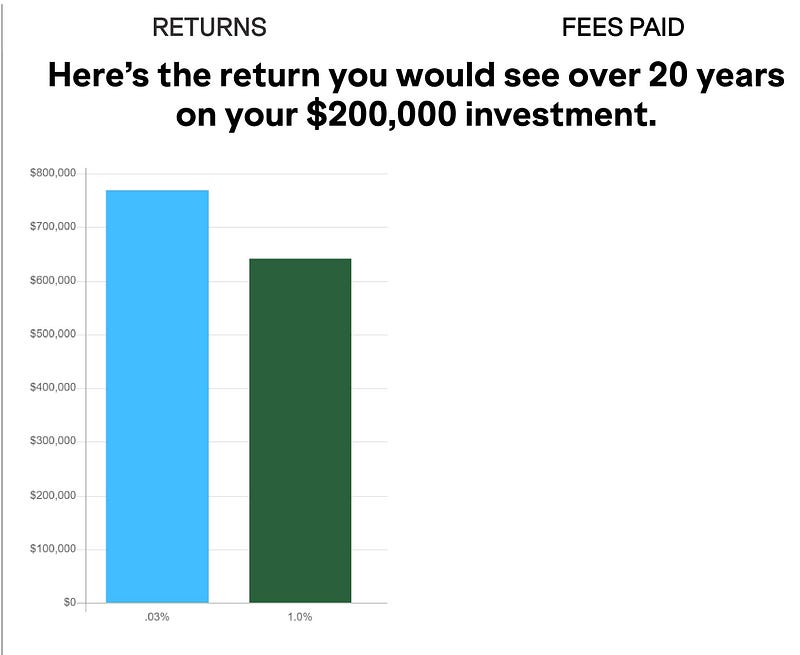

For a simple example, I am going to look at a portfolio worth $200,000 invested over 20 years, with no additional contributions, with both a 1% AUM fee taken, and comparing that with the money being self-managed in the Vanguard S&P 500 Fund, VOO, which charges a .03% fee.

I ran a 7% return rate for both portfolios.

Again, many financial advisors will not keep it simple by investing your money in ETFs that track an index (S&P 500, NASDAQ, etc.), and instead chase more expensive mutual funds, or more exotic ETFs that actually put fat commissions in their pockets. Remember, the financial industry is full of sharks and vampires.

Here is the total return comparison.

That is $769,611 with funds in the VOO, vs $641,427 paying a 1% AUM fee at the same rate of return!

A difference of $128,184!

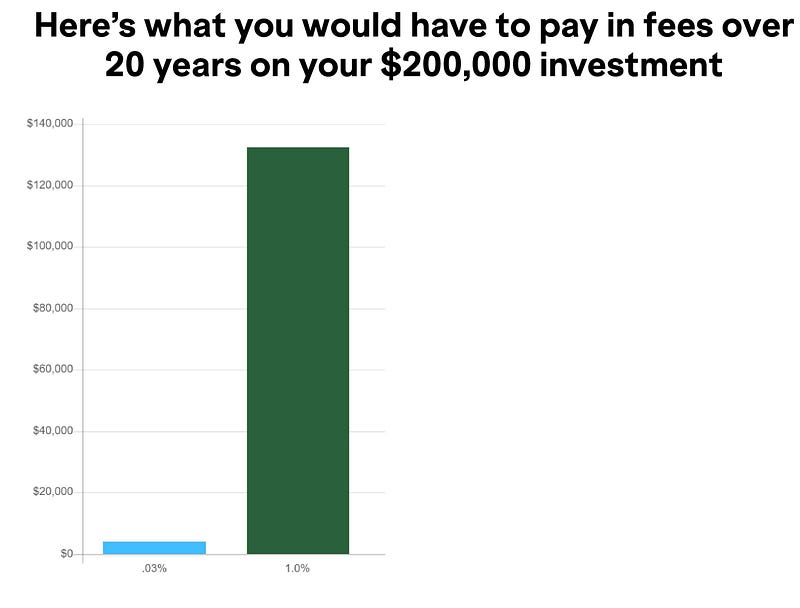

Of course, the reason for that is the staggering amount that a “small” 1% fee amounts to.

No less than $132,515 in fees! That’s great for the investment advisor's pocket! What about yours?

With $VOO, you’d pay just $4,331.

To me this difference is inexcusable. AUM fees are the equivalent of a timeshare for wealthy people.

Now Matadore, you say, some people are busy with life, kids, and careers! They don’t have time to research stock and ETF investments and manage it all!

I entirely reject a notion like the one regularly peddled on The Ramsey Show that everyone needs to go out and hire a “SmartVestorPro” to do it for them because you need an expert to invest.

I say bullshit, but I fully acknowledge some people manage to amass quite a portfolio of assets and might need more insights on taxes, estate matters, etc.

In that case, they would be much better off finding a “flat fee” advisor, one that will agree to help on an hourly or one-time basis, or a retainer, often on an annual basis. Similar to how an estate attorney will build an estate plan for a fee, there are fiduciary advisors out there who will as well.

You can google this and find local groups that work on these models. Make sure they also advertise themselves as “fiduciaries”. I would limit the choice to someone who is a registered CFP.

They should approach the conversation from what you are looking to solve for, your goals, and work from the perspective of showing you options that are in your best interest, not telling you where to put your money.

Facet is one such model that is available to anyone and was specifically designed to buck the system of opaqueness, high fees, misaligned incentives, and low accessibility.

I make nothing by mentioning Facet, I simply believe it is a service that does things the right way.

What do you think about AUM fees? What is your opinion about managing your investments yourself?

Thanks for reading.

If you are looking for more help getting out of debt and building wealth, you can get my newly published Zero To Wealth Workbook here! This is the exact method I used to pay off debt and build wealth and will help guide you along.

Some of my other, recent popular stories.

Female Hypergamy Is Real. And It’s A Bitch.

I Gave Up Drinking For The Month Of October. Here Is What Happened.

Dave Ramsey’s Investing Advice Is Both Bad and Wrong.

The information provided here is for informational and educational purposes only. It is not intended to be, and should not be considered as, financial advice. We do not provide personalized financial, investment, or legal advice. The Matadore is not a registered CFP.