Nassim Taleb Trading Strategy in Practice: How to Profit from Black Swans.

Whenever I drop the name of Nassim Nicholas Taleb on a conversation with my colleagues who work on Artificial Intelligence I get weird gazes, and I can understand it, Taleb has dedicated many lines to make fun of guys who -like me and my colleagues- use mathematical models to make money in the stock market.

However, if you can put up with his cocky writing style, you will find that he raises some interesting points in his books. Actually, the most frequent complain that I hear about him is that people like his ideas but they don’t see how to put them in practice.

In this article, I will lay out the basics of Taleb’s strategy and explain how you can implement it in real life.

The Origin of the Barbell Strategy

The first thing we need to understand is the core of Taleb’s thinking. Basically, Taleb all his theories are based on the inability of models to predict rare events that he calls black swans.

He advocates a barbell strategy in which most of your money (about 80 –90%) goes to “safe investments like bonds” and the remaining 10–20% is allocated for very risky assets with huge upside potential. Now, the problem for a beginner is: how do you find these very risky assets and invest in them?

Well, I will use the opportunity of answering this question to actually show you some interesting and crucial concepts that will change the way you look at the stock market.

If you read Taleb’s books you probably had to watch him spend lots of ink talking about “mediocristan” and “extremistan”, and if you didn’t read them don’t panic, I will summarize in 2 lines what it is all about:

The variance of stock prices does not follow a Normal or Gaussian distribution, however most models used by traders assume they do, this causes them to underestimate the probability of very big movements called black swans or fat tails

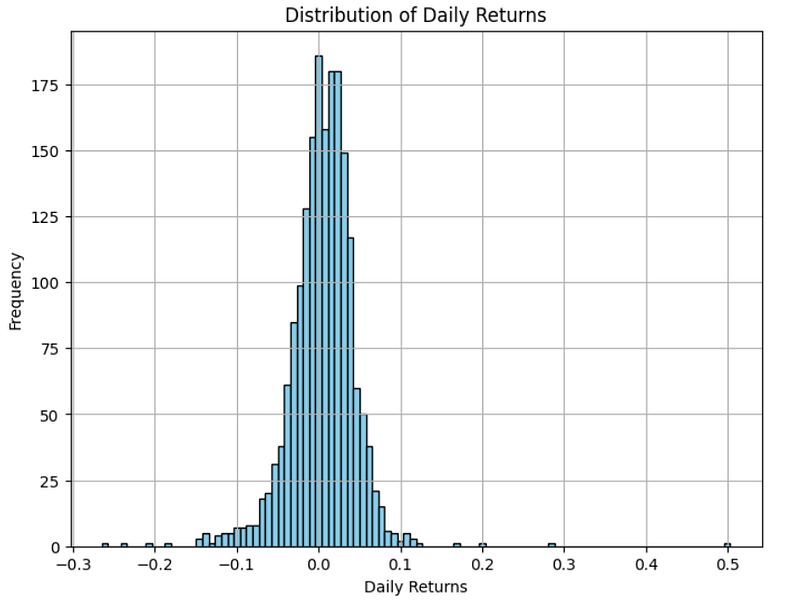

But an image is better than a thousand words, so just look at the following graph, it is the distribution of daily returns for the S&P500 from 1982 to 2021:

As you can see, the distribution is not Gaussian, in fact, there are some very good and bad days that happen more often than expected, and it is precisely during these rare days where the market falls or raises 10–20% that most of the money is made or lost.

This what Taleb calls “Fat tails” and their probability is much larger than expected in Normal distributions. The same is true if you look at monthly or yearly data.

Now, think of it, a model can be right 99% of the time and still miss the biggest movements in the market, which happen during the remaining 1% of the time.

That’s why Taleb complains of models using normal distributions and here comes the funny point that made Taleb rich: normal distributions are everywhere in the trading world.

In fact, the most popular formula used by traders to price stocks is the Black-Scholes formula, which relies on the assumption that volatility is constant across stock markets. Sounds like joke? It isn’t. You might find it hard to believe, but the truth is that 50 years after the creation of this formula, computers are still running models that assume that the markets have constant volatility.

Making Money From Mispriced Options

Option trading is by far the best way to make money out of failed normal distributions. People like Taleb have been trading options for fun and (huge) profit since the 80s. They realized that models using gaussian volatility to price option ended up mispricing the option very often.

Let’s see an example of how to price an option with Black-Scholes formula using Python, this very simple code will do:

import numpy as np

from scipy.stats import norm

def black_scholes_call(S, X, T, r, sigma):

d1 = (np.log(S / X) + (r + 0.5 * sigma**2) * T) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

call_price = S * norm.cdf(d1) - X * np.exp(-r * T) * norm.cdf(d2)

return call_price

# Example usage:

current_stock_price = 140.13

option_strike_price = 145

time_to_expiration = 28/365 # 6 months

risk_free_rate = 0.0068

volatility = 0.23

call_option_price = black_scholes_call(current_stock_price, option_strike_price, time_to_expiration, risk_free_rate, volatility)

print(f"Theoretical Call Option Price: {call_option_price}")If we run that snippet we will get this result: Theoretical Call Option Price: 1.7177. Now, let’s compare this with another method which doesn’t assume constant volatility.

Non-Constant Volatility Methods

Cool, now if you go to your online broker and check the price of that option, most probably this is the formula that they are going to be using. So your task is to try and spot mispriced options by using other methos that do not assume constant volatility.

There are many ways to do this, but one popular method is the Heston method, so let’s go ahead and calculate the price for this same option using it in Python:

import QuantLib as ql

def heston_call_price(S, X, T, r, kappa, theta, sigma, rho, v0):

# Set the evaluation date to today

evaluation_date = ql.Date.todaysDate()

ql.Settings.instance().evaluationDate = evaluation_date

# Define QuantLib objects

spot_handle = ql.QuoteHandle(ql.SimpleQuote(S))

rate_handle = ql.YieldTermStructureHandle(ql.FlatForward(0, ql.NullCalendar(), ql.QuoteHandle(ql.SimpleQuote(r)), ql.Actual360()))

dividend_yield = ql.YieldTermStructureHandle(ql.FlatForward(0, ql.NullCalendar(), ql.QuoteHandle(ql.SimpleQuote(0.0)), ql.Actual360()))

# Create the Heston process

heston_process = ql.HestonProcess(rate_handle, dividend_yield, spot_handle, v0, kappa, theta, sigma, rho)

# Create the option

payoff = ql.PlainVanillaPayoff(ql.Option.Call, X)

exercise = ql.EuropeanExercise(evaluation_date + ql.Period(int(T * 365), ql.Days)) # T is in years

option = ql.VanillaOption(payoff, exercise)

# Calculate the option price using the Heston model

engine = ql.AnalyticHestonEngine(ql.HestonModel(heston_process))

option.setPricingEngine(engine)

heston_option_price = option.NPV()

return heston_option_price

# Example usage:

current_stock_price = 140.13

option_strike_price = 145

time_to_expiration = 28/365 # 6 months

risk_free_rate = 0.0068

volatility = 0.23

heston_option_price = heston_call_price(current_stock_price, option_strike_price, time_to_expiration, risk_free_rate, kappa=2.0, theta=0.05, sigma=0.3, rho=-0.5, v0=0.04)

print(f"Theoretical Heston Call Option Price: {heston_option_price}")Now, if you run that code you will see that it returns this price: Theoretical Heston Call Option Price: 1.2626.

So, as you can see, for the very same option, the price difference between Gaussian and non-Gaussian methods is huge, in this case it went from 1.7177 to 1.2626, this means the price should be 26% cheaper and therefore you can exploit this price discrepancy.

There are many strategies for profiting from mispriced options, in this case, we saw that the call price is too expensive, so the most obvious way is to sell (write the option contract) this option. In the opposite case, if the call price was cheaper, then you could buy the option.

Of course, this code was just a prelimimary approach, and there are many details that you could adjust in those formulas and many others that you could try. But the main point is that mispriced options offer a great opportunity for great profits, and this was how Taleb made his killing in wall street.

To be precise, during the period leading to the 2007–2008 financial crisis looked at the option prices assets in the real estate and financial and came to the conclusion that they didn’t make sense.

It was too cheap to buy options betting on real estate stocks going down, the models were underestimating the risks, and offered very low prices. Taleb saw this opportunity and bought heavily into it, making a huge profit when the market crashed.

The Problems with Taleb’s Strategy

Now, even though his strategy is of course a valid approach, in my opinion there are two huge problems that make it unsuitable for retail investors.

- Long periods of losses: this strategy involves a lot of waiting until a black swan happens, in the meantime you are underperforming or even losing money.

- Cost of opportunity: this strategy requires you have the bulk of our portfolio sitting on low profitability assets like bonds, preventing you to invest in more profitable ones.

These problems together with the deeply sophisticated knowledge of options trading required, make me not recommend this strategy for retail investors.

In my opinion, there are much better ways to make money in the stock market, specially if we are talking about quantitative strategies.

After trying many approaches I deeply believe what works best is a Bayesian Strategy in which you manage your risk exposure based on probabilities, this combined with the use of leverage is what has allowed me to create a model that beats the S&P500 by 549% during the last 24 years.

Bayesian Risk Balancer

Thanks for reading until the end. Before you go:

- If you enjoyed this article, visit bayesianriskbalancer.com to gain access to the bayesian model that I use for my personal investments.

- Visit my YouTube Channel: https://youtube.com/@ModernaiTrading for more detailed video contents.

- Follow me on Medium to stay tuned for more related content.