MONEY MANAGEMENT | BUDGET

Monthly Budget Update — June 2023

Buckets of Money

Big decision time (for me): I moved my budget off spreadsheets and onto YNAB (You Need a Budget).

Why?? A couple of reasons: First, while I LOVE and value spreadsheets, I have maxed out my knowledge and skills. Yes, I could take a class or whatever to learn more but my time and mental energy are better spent on activities that are homeschool related or that generate income. Second, I chose YNAB because it is a “buckets of money” app that operates smoother than my spreadsheets and I can access it across all devices. #simpleliving

Specifically, I can check the balance in my clothing bucket when I am at the store and come across a royal blue Merino wool dress I want to buy.

YNAB is a zero-based budgeting app, a modern tech-friendly version of the cash-stuffing envelope system. Money comes in, I allocate it into my buckets, and deduct it as it is spent.

YNAB is compatible with most banking systems in the USA which allows accounts to be directly linked to it, but not so many in Australia and other countries. I have a simple workaround system I use that I will share in a future article.

What YNAB doesn’t do well is generate reports showing me the results I am looking for so at the beginning of each month after all transactions from the previous month are entered in YNAB, I copy the totals over to my end-of-the-month spreadsheets.

One of my spreadsheets shows the total income and allocations. The other spreadsheet shows actual spending from each bucket. And yes, they are quite different.

Allocating into the buckets happens in every category every month (unless a bucket is fully funded) but I don’t spend money from every bucket every month.

Cat registration is due in March. Dentist appointments happen in January and July.

My actual spending may be less, the same, or more than my income and that is ok. It is how the bucket system works. I’m not spending from my income but from my buckets.

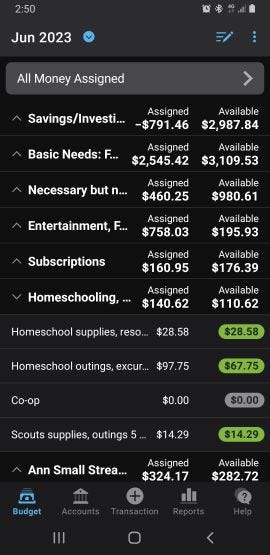

Let’s take a look at my buckets in YNAB. The categories are all the same that I had in my spreadsheets with 1 that is new: Subscriptions.

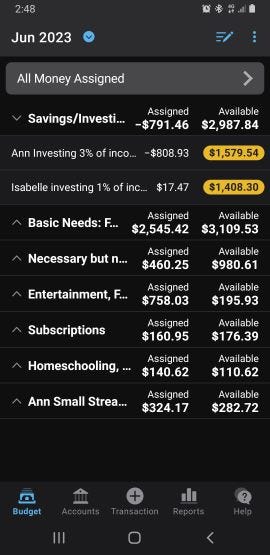

Savings/Investing

This small category shows the 2 accounts I have set up, 1 for me and 1 for my daughter where I capture the money I am setting aside for us to invest. In a perfect world, the balances would match our bank savings account balances which at this time they don’t. I’m working on it while we are researching how to get started investing. These are Savings Builder accounts that get a set amount each month with no limit set. I will always be adding to these accounts from my income.

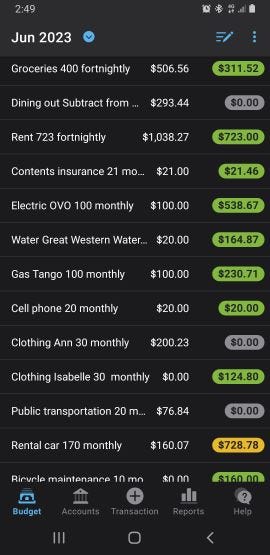

Basic Needs: Food, Shelter, Clothing, and Transportation

My categories are based on needs vs wants with the needs buckets prioritised to be filled with money before wants. No other buckets in my budget get money allocated to them until all of these in Basic Needs are filled for the entire month.

Some of these buckets (groceries, cell phone, and a couple of others) are spending buckets where money just flows through them. Others such as clothing are Savings Balance buckets which have a specific target amount that I save up to, spend from, and then replenish.

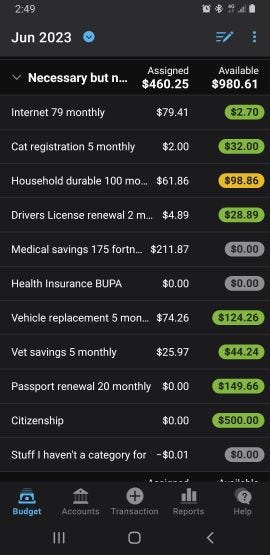

Necessary but not Basic Needs

These buckets are periodic expenses that may or may not have a specific due date. For some people, they might qualify as emergency expenses but I treat them as expenses I can plan for even if I don’t know exactly when they will happen.

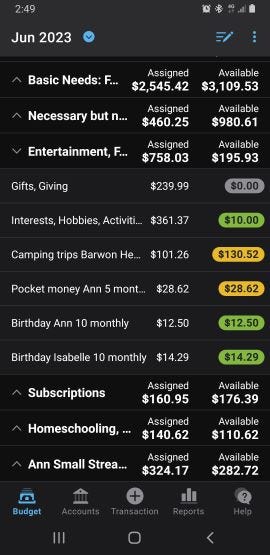

Entertainment, Fun, and Convenient Privileges

These buckets are all about the quality of life. None of them have to be funded but they do make life more enjoyable. I used to have a bucket in here called Subscriptions which is where I captured all of my monthly and annual subscriptions. Now they are in a separate category.

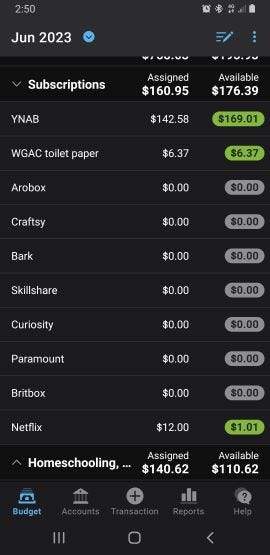

Subscriptions

I decided to pull Subscriptions out of the “Fun” category and list all the subscriptions individually: Netflix, WGAC toilet paper, and more. I’m not subscribed to all of these at this time. Paramount is new and I’ll Netflix is cancelled. Arobox and Bark and apps for encouraging and limiting time off screens (specifically phones).

Most of the subscriptions can be paid monthly but cost less over the year if paid annually so I need/want to look at them individually.

Plus, how easy is it to pay for a subscription that actually isn’t being used?! I know it’s happened to me. Recently, I discovered a AU$15 charge coming out monthly that I wasn’t using at all. So I cancelled it.

Homeschooling and Scouts

Technically, these buckets are needs not wants, but they also will disappear from my budget once my daughter is launched and paying for her education herself. But for now, as a homeschooling parent, I pick up these costs. And yes, we treat Scouts as a resource for her education.

Except for co-op, all of these buckets are Savings Balance buckets. They each have a target that I save up to, spend down, and build back up again.

That target amount has changed over the years. When she was young, we spent very little on resources taking advantage of the offerings through the public library, community centres, and parks departments. Now though her needs and interests have changed and expenses have grown. But that’s not to say we do everything.

When there is no money in the bucket and even when it is fully funded, it is a finite amount and choices have to be made. We have a lot of conversations about which experiences offer the highest value per dollar spent. And once we commit to an activity, we rarely back out because we know that others are relying on us to be there — to spend time with us and/or to meet the number attending requirement for a group discount.

Wrap Up

The changeover from spreadsheets to YNAB went smoothly with only 1 false start. I’m still learning some of the ins and outs of YNAB and am prepared for another reset if need be. Unless I can get the balances to match on my savings accounts I’ll have to start over, but that’s ok. I’ll get it figured out.

I’m pleased to report the totals of all my buckets equal the total of my bank account and I am on track to building my financial security after starting over just a year ago.

Rather than putting all of my income eggs in one basket of employment, I am building multiple small streams of income that I will share with you in future articles.

Thank you for reading to the end. To receive future articles I write in your email inbox, click SUBSCRIBE. I write about lifestyle choices including simple living, homeschooling, Stoicism, walking as transportation, sewing, family budgeting, and more.

Next article: Why Not Walk?

Previous article: Solve Problems Early