Making Ends Meet on $250k A Year!

The struggle is real, folks.

A Bloomberg article by Alexandre Tanzi tells us “More than a third of Americans earning at least $250,000 annually say they are living paycheck to paycheck…”

A separate survey released by the Federal Reserve last week found an overall improvement in the financial well-being of households since the pandemic, bolstered by stimulus aid and surging prices in assets like houses and stocks.

“About 78% of Americans said they were doing okay financially or living comfortably — the highest share since the Fed began running the annual survey in 2013.”

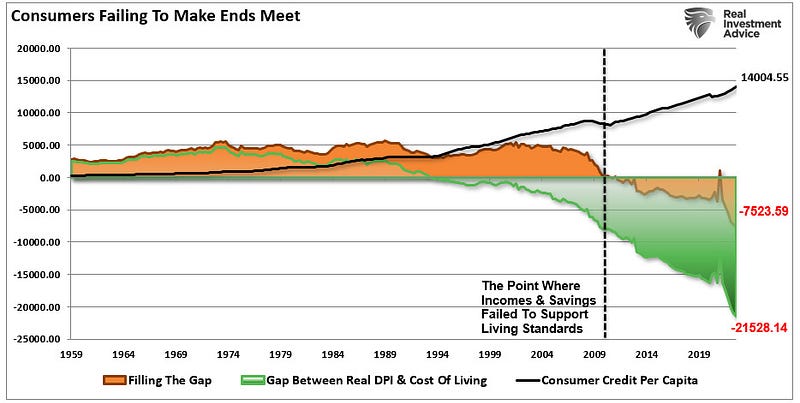

Still, one in nine respondents said that they wouldn’t be able to cover a $400 emergency expense by any means, including credit cards, borrowing from family and friends, or selling an asset.

Now, you might be thinking, “Matadore, $250,000 is a lot of money! If I made that kind of money, it would solve all my problems!”

Well, that all depends on where and how you live.

I can speak from personal experience. More money always makes things easier, and when the average home price in America is $542,900 (at the time of this writing) and inflation remains at historically painful levels, money just doesn’t go as far as you’d think it would.

Let’s dig into some real-world costs….

We will consider a $250,000 household with two children and an average mortgage payment of $3,048. I am not clear if that includes property taxes, which is a major variable, and cost.

Using a rough tax calculator this $250,000 salary brings home about $13,774 a month, net.

This US News report found a family of four eating (real) food is likely spending $1,410.80 to $1,528.10 a month

I can attest to similar costs in order to eat well. I am not talking about dining out often, even. I am talking about eating home-cooked meals consisting of meat, fruits, vegetables, etc., not boxed, processed, or fast food.

Using some of my own, 4-person household costs, Utilities ($450), Gas & Fuel ($300), Insurance (Life, Auto $216), Internet and Phone ($220) and we can aim for about $5,762 in “running the house expenses”.

This doesn’t include eating out, saving for a vacation, clothing, home supplies (toilet paper, toiletries, etc.), entertainment, or children’s activities (sports, dance, etc.).

But let’s just say this household now has $8,012 in surplus.

What about 401(k), HSA, or ROTH contributions? Anyone making $250,000 a year should be saving money, right?

Let’s peel off $1,875 per month for the 401(k), and $541 for the ROTH.

Now we have $5,596 per month left.

About those Kid’s Activities ($450), School Fees ($150 monthly(annualized)), Vacations ($9500, annually, $791 monthly), and Entertainment ($150). You see where this is going.

Down to $4055.

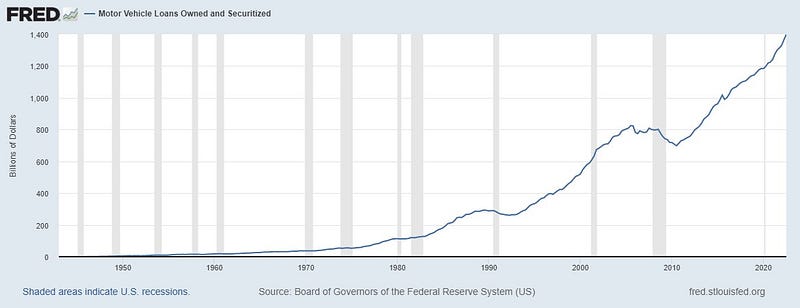

Now, most people, around 31% of American adults, have a car loan payment. In fact, a car loan ranks high on the debt stress level. I would imagine looking at this chart.

But what can we assume a car loan costs? What about two? Family of four, two jobs, two cars? According to Bankrate, on average, drivers are spending over $700 and $500 each month for new and used vehicles, respectively.

Let’s meet in the middle and knock off $1,200 for two cars.

$2,855.

Now sure, $2,855 is a decent chunk of change at the end of every month, but how many Americans, based on what we know about the number of people that cannot meet a $1,000 emergency, are saving and not spending it (dinners out, booze, general consumerism)?

Yes, in the scenario I run thru, this family of four making $250,000 isn't struggling, but any inference that they would be called “rich” or be living a lavish lifestyle simply isn’t reality.

In fact, what we can take from this thought experiment is that if you aren’t making at least $250,000 a year, and have children, you aren’t likely able to save significantly, take reasonable vacations, or feel like you are “getting ahead”.

It's no wonder so many people are falling behind.

Although again, back to and depending on where you live, perhaps not making any money at all can be a lottery ticket of another kind.

Thanks for reading. Be good stewards of your earnings.