Part 1. How saving $18,000 a year can make you a millionaire many times over.

Three common investment vehicles do the work. The magic is in the withdrawal stage.

We have covered a variety of investing tactics on this blog.

Here, I will highlight how making separate $6,000 annual contributions to a 401(k) (or similar 403(b), 457B, etc.), a ROTH account, and a taxable brokerage account can be an incredible combination for wealth.

Let’s dig in…

Here is the simple plan and resulting math.

- $6,000 into a tax deferred, qualified plan. This is where you would fill up pre tax contributions. Again, 401(k), etc.

- $6,000 into a ROTH. If you have a ROTH 401(k) option, you can use that. Most work sponsored plans nowadays have that option. Ask your HR or plan administrator if you don’t know. If not, establish an individual ROTH IRA to utilize.

- $6,0000 into a taxable brokerage account. Any reputable brokerage outfit can work. Schwab, TD Ameritrade, etc. Perhaps your 401(k) plan or HSA investment account is a good place to look so you don’t have learn a new platform. Same for your ROTH, if going the individual route.

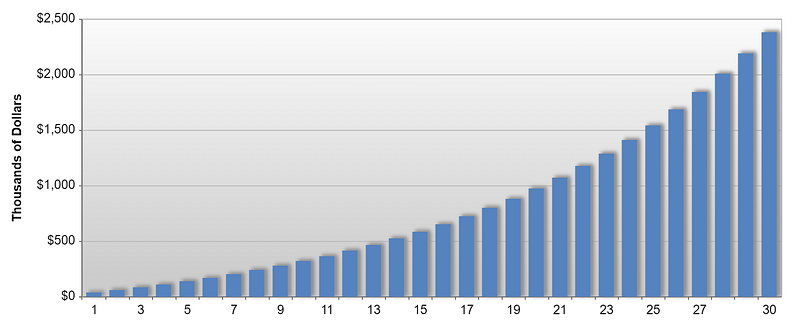

Do this starting at age 25 or earlier.

Running a simple investment calculator over 30 years, using a conservative 8% annual return estimate, with returns compounded, you would end up with $2,383,353.42.

$2.3 million dollars before age 65.

This does not account for any employer match contributions, or extended period of outsized returns and reinvestment.

What if you are the 13% of people that max out your 401(k)?

In this case, you’d split the $20,500 contribution (for year 2022) between tax-deferred and ROTH, $10,250 each. Then put $6,000 in your brokerage account.

How does $3,508,826 sound?

What if you are starting later in life and finally getting serious, like me?

I still have 17 years, minimum. Employ the same strategy above with existing savings (I will plug in $176,000; you can change this to suit your own situation), and we are looking at $1,617,135.

Again, not taking into account any match or additional savings, the returns are powerful.

What you are putting your money in is up to you to research, but low cost ETFs like VTI, VOO, VIG, etc. along with sector style vehicles like XLE, XLV, XLP work well. This is where is pays to be macro aware and manage your investments accordingly.

Even if your sponsored plan is captive to funds of the issuer, there are some options better than others. Do your homework.

In the second part of this post, I will look at the benefit of setting up your investments in these three specific investment accounts relative to withdrawal. Stay tuned.

Thanks for reading, be good stewards of your earnings.