Loans That Kill or Make Us Stronger

Reflections on the terror of loans, and being pursued by those to whom you owe a pound or two or three… of flesh

1. The wisdom of youthful fear…

When I was a kid, one of my unfathomable fears was living destitute under a bridge or in a Whirlpool washing machine box, scrounging for cans of cat food. I don’t know where that fear came from. I grew up in a distinctly middle-class, first-generation, immigrant, hyper-educated family with no hints of poverty that I can recall. I remember that we started out renting while my dad got his Ph.D. in nuclear engineering, and a decade later we owned a small 3-bedroom home in a suburban neighborhood. And I recall on trips as a young kid in the family car, imagining each underpass being my home. How would I get my mail, I thought (kids worry about such important things). These are the fears that (I think) evolved into my adult attitudes to loans.

Eventually, I went to college, then right on to graduate school, and came out a newly minted engineer. That’s a terrifying thought — I didn’t know which end of a screwdriver or caliper to hold, but I was a professional engineer. I started working in the Midwest for a medical device company. So, think about that next time as you lie on the gurney about to go under the knife for that artificial hip or knee or brain implant — those fresh college kids who slaved away on the designs of those critical devices, not knowing which way was up.

But, in the meantime, as I slaved away and learned new things at a crazy pace, those nightmares of homelessness faded. Instead, they left their scars embedded in a wise and useful way.

What they left in its place was a fear of loans and any form of obligation to others. I wanted my fate in my hands, not in the hands of others.

I always thought of loans simply:

- Lenders are predators with big teeth — use loans sparingly if at all

- Good loans invest in your future (paying now for school, professional certifications, and things that will enhance your future career or earnings)

- Bad loans pay for your past purchases (paying now for a buying decision you made years ago, like a car or house)

I still believe investing in your future is a smart use of loans. But borrowing for a consumer product, a car or home or vacation, is not as much. You’ll see how I navigate this rather hard dichotomous view of loans as we go along.

2. The first loans…

My dad was a super-smart guy, but not a nice guy. I’ve found often that brains and agreeability are diametrically opposing traits.

The problems were between my mom and dad, but clearly, that conflict affected us kids as collateral damage. After the divorce, I knew none of us kids could expect any help on college financing. Mom raised three kids on her own working at Sears stocking shelves for minimum-wage despite having a master’s degree in music. She is an amazing woman and mom, and everything good I have today comes from her.

I was smart enough to go to college, and to one of the best private universities at that, but not so smart as to harvest sufficient grants and scholarships to cover the bill. The majority of my undergraduate years were funded by loans, followed by work-study paychecks, and then a tiny bit by the few Pell grants and scholarships I managed to attract.

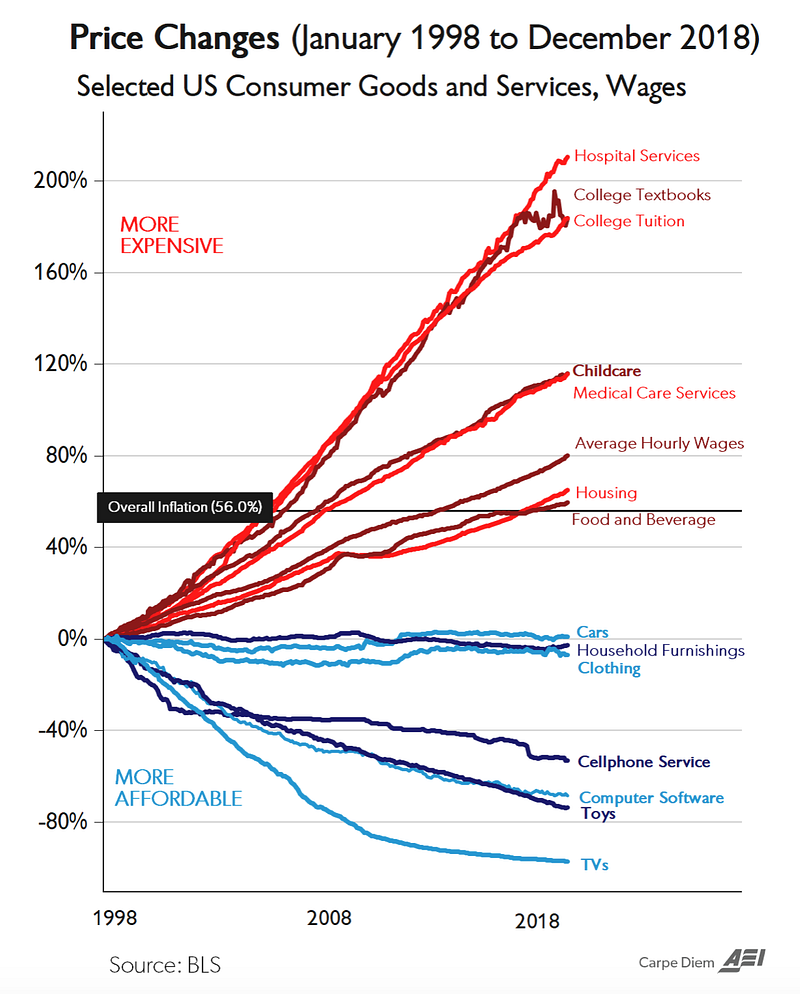

When I graduated with two bachelor’s and a master’s degree in engineering crumpled up in hand, I also had a job, but no car. I was on the east coast. My first job was half a continent away. I needed a car. That was my second loan. Seeing the inflation of college education in the graph above makes me realize how lucky I am that I got my education when I did.

So here I was, a newly minted professional engineer, working at his first job in the cornfields of the Midwest. The company paid for all my moving expenses and put me up for a couple of weeks in a hotel, and helped me find a small 1-bedroom apartment.

I had rent, utilities, food, clothes, and car — and that was about it for expenses. I lived out of my suitcases for months. I used the same milk-crates which I used as bookshelves all through college as my multi-purpose furniture. Why wasn’t I splurging all this new-found professional salary and sign-on bonus on furniture, a hot tub, snowmobiles, and motorcycles…?

Because I had loans. School loans and car loans. And these bothered me. They bothered me like residual nightmares of homelessness, stirring uneasily.

And I wanted to figure out how these things affected me and my future.

The first thing I noticed was that my school loans ranged from 4–6% annual interest for ten years. My car loan was over 12% annual interest for five years.

I noticed that inflation was at or greater than my school loan interest rates. And my car loan was twice the inflation rate. I considered the car loan as very expensive money (high-interest rates relative to inflation) and the school loans as cheap money (low-interest rates).

My first decision was to pay off the car loan as soon as possible since there was no penalty for early payment, and to hang onto the school loans for the full decade. I paid off the car in two years, and the school loans in ten.

3. The building years…

My first job was wonderful. I loved the people. I loved the work. I loved the travel. I especially enjoyed being responsible for making important medical devices that helped people. And, I got a kick out of working with surgeons, the sales-people, academic researchers, even my fellow engineers….

But it wasn’t quite what I was made to do. I could feel that in my bones. Engineering was an OK fit for me. But not a good or perfect fit. And the Midwest, though I was born there, didn’t feel like home either.

After five years I left and moved back east for a similar job, different company. Not a good move. My new boss was a jerk, the first of many encounters with smart jerks who were in positions of power they were ill-equipped for. But thanks to the courage of my mom who picked up and left a smart but abusive partner despite having no marketable skills of her own… I realized that I was not trapped with work-jerks any more than my mom was trapped with a home-jerk. I gave each boss no more than a year or two to see if they’d shape up.

During those one or two years, I worked hard and gained as much experience as possible on projects, and also took advantage of every educational opportunity. I got professional certifications, I took undergraduate and graduate-level college courses, all paid for by the company. And if the boss continued to be a jerk, I left.

I was always pleased to hear that the bosses I left had a considerable industry-chatter like a black cloud about them — people talk. Unhappy people talk a lot. And I would hear engineers and technicians confirming my poor impressions of bad bosses. The internet made this even more prevalent.

The benefits of changing jobs quickly were huge: all that experience and additional education from the old job translated into quickly accelerating salaries in the new job. I found that the old company you worked for will not value you (especially with a jerk for a boss) as much as a fresh company. So, as a young professional, I learned there were way more benefits to moving every couple of years than there were detriments. I also learned that I never once needed a recommendation from a shit boss.

So, my income increased exponentially during those years and far outpaced inflation (which is the rate most annual raises are given at).

I focused on several things during these building years:

- Controlling my expenses, making sure they did NOT increase along with my salary

- Paying off my loans according to my plan

- Saving as much as possible and investing wisely

- And NOT taking on any new loans (either credit cards or any other form of financial obligations. Note: I had credit cards to “build up my credit scores” — but I religiously paid off the full amount every month)

4. Preparing for the transition…

I married a wonderful woman and had two amazing kids. Now here’s the thing. My wife, just before I met her, had been making a big transition from a career in teaching middle school, to a technology career. When we got married, she had just made the jump and was now an engineer. She was smart — making a move from a poorly-paid career to a well-paid one. We were a two-engineer home.

But I went in the opposite direction. I had felt that engineering was exciting and fun — but not quite what I was made to do. I wanted to do science. So I started taking night classes, mostly paid for by the company. Eventually, I took graduate-level courses to see if I could handle the level of academic rigor. Then I took the Graduate Record Examination (GRE), and when my grades and test scores and recommendations all lined up — and I got accepted into a graduate program — I left my engineering career behind. I was 46 years old.

I got lucky and the Ph.D. program I entered paid all expenses, provided health insurance, and paid a stipend (a pittance, but a young person could live on it). So, while I had lost all my income as an engineer/manager, there were also no expenses associated with my tilting at windmills and going back to school as an old duuude.

I consider myself lucky on so many counts. First, being married to a smart, professional woman who, though reluctant, still agreed to my leaving a lucrative job and career for a poorly-paid one as a student and a future as a poorly-paid scientist. Second, getting accepted into a good graduate program that covered all expenses so nothing was out of pocket for me (other than the lost-opportunity income of the engineering job). Third, the savings and investments were doing well enough that they covered a significant amount of my lost income as portfolio gains (not as cash flow, though). And fourth, the wife’s engineering income was sufficient to cover the family’s operating expenses — so we did not need to tap into savings — as long as she remained employed.

So now, today, I have made the transition to academia. I did not finish the Ph.D. program but put it on pause due to Lyme disease which I contracted in year 6 of the program. Nonetheless, I am working as a staff scientist at the same graduate school, working with great people on fundamental biological research — and finally feeling like I am doing what I am supposed to do. This is the perfect fit that was missing during my engineering years.

5. The last loans…

Yet another way I was extremely lucky is that during the first couple of decades of my engineering career, I was never laid off or fired. I left each company on my terms and schedule — I often made sure to take four to six weeks off between jobs to go and travel. I went to Japan with my mom on one of these between-job jaunts, backpacked for a month by myself through Scotland and Wales on another, had our long-delayed month-long honeymoon in the south of France and Corsica on yet another… But I was otherwise fully employed during those two decades. This included the Dot Com crash of 2001 and the bursting of the Housing Bubble in 2008.

The point is I never had to tap into savings to pay for months or years of unemployment.

I left the engineering world for academia a few years after the collapse of the Housing Bubble, and my investment portfolio had not yet recovered to the pre-bubble highs. Yet I set up my portfolio for my new world as a poorly-paid academic and student and bought more conservative stocks than I normally did.

I invested aggressively during my engineering years, establishing a solid foundation using stock mutual funds (mostly S&P500 index funds), and then buying a few aggressive individual stock picks. The life changers were companies like Netflix, Amazon, Apple (and now more recently Tesla who I wrote about here).

The other important financial bit is that I resisted buying a house. I left the engineering world at 46 years old, at which time I had never owned a house. This was one area that caused considerable arguments with the wife and a very good friend who was our real estate buyer’s agent.

But finally, a few years ago, I relented. And we bought a house built in the 1990s in a good town with good schools for the kids, near my own school, and the wife’s work. This, clearly is by far the biggest loan of my life, and one that caused me considerable concern. We are all happy with the home and town. And I have no regrets for postponing buying the house.

But here’s the thing with the home loan. The interest rate on the home loan is, like my old school loans, approximately equal to the rate of inflation (~3%). Furthermore, the interest rate on the home loan is less than the returns on my investments. Typically, a diversified US stock index fund like the S&P500 might expect a 7–8% annual increase on average per year over periods of decades. Although I had investments available to pay for more of the house, I decided that I would arbitrage the investments versus the home loan, and over the 30 years of the home loan, I should be netting 4–5% by keeping the investments intact, rather than paying down the loan.

So I am doing with the home loan exactly what I did with the school loan — extending it for its full duration because of the low-interest rate relative to inflation and to my investment returns.

So although the home does not qualify in my simple dichotomous model as a “good loan”, neither is it a “bad loan”. Like many things in life, it’s a mix of good and bad. Black and white categories don’t work in the real world.

6. Post-script…

A few years ago, the wife lost her job. She had a generous severance that covered most of a year. But then she was unable to find a job for another year after her severance ended. When she did finally land a job earlier this year, the coronavirus hit, and she lost that job too. Lyme disease limited the energy I had for work, and I am now working only part-time.

These are factors that we theoretically considered but never seriously thought would happen.

Nonetheless, the decades of aggressive savings and investments, and minimizing expenses, have repaid us and covered us well. Although the savings were originally intended for later use for college (kids are still a few years away from that) and retirement, it is finding good use in keeping us going day-to-day today. We know we are lucky that way.

But it never feels good using investments originally intended to send kids to college — and for our golden years — to be paying for family operating expenses today. The old nightmares of living under highway overpasses are stirring again.

But again, we have gotten lucky. The wife has recently found a full-time technology job working from home. We don’t know how long the job will last.

Despite these issues, despite the pandemic, despite this despicable president, my blessings are numerous, and I can say that my priorities are family, health, and happiness, which come in far above careers, income, and financial issues. That said, financial problems underlie many family conflicts and reduce happiness.

Unwise use of loans is one of the main well-worn paths to financial distress.

If you are blessed and lucky, please help those who are not as fortunate during this pandemic. The ranks of the homeless have grown alarmingly. At the least, please give to charities like Habitat for Humanity or Pine Street Inn (two of our favorite charities) or many other good charities that help the homeless. Who knows, there may be a duuude there you might recognize. ;)

Thank you for reading, and please share.

Note: I also wrote about Netflix here: