Tesla’s Stratospheric Launch Continues

A review of the historical numbers and a look ahead to the Q3 2020 earnings call

1. A historical context to Tesla’s numbers…

Tesla (ticker symbol TSLA) is scheduled to have a Q3 2020 earnings call on Wednesday, October 21. To put the numbers into context, it is always good to have a running history of your favorite data, which I’ll try to show here.

Before we look at numbers we should ask, what is Tesla? If you look at what they sell, Tesla is currently predominantly a maker/seller/servicer of plug-in battery-powered electric cars.

If, however, you look at new and future products as the harbinger of what Tesla will be, they are working on all manner of products for energy generation (solar) and storage (batteries), as well as additional battery-powered transportation modes such as trucks.

If you look at how Tesla does what they do, they are heart and soul a disruptive technology company doing to the fossilized automotive industry what Apple did to the old music industry, what Netflix did to video entertainment, Amazon did to retail, and Google and Facebook did to media and advertising.

I think the most productive way to view Tesla is as a disruptor and an evolved heir to the Silicon Valley technology ethic. I believe/hope tech companies will evolve from today’s focus on “like” buttons and programming an endorphin rush, towards Tesla’s focus on extremely hard innovation and technology work — designing and building and selling important physical/software products that transform our lives in real ways.

But at its core, the company is trying to wean us from hydrocarbon-based fuels by making us fall in love with amazing battery-powered electric cars.

The first thing any new company has to do is to move product. Often this has a multi-phased approach where a dramatically new innovation seeks the early adopters, and systematically moves through the remaining population of their increasingly more risk-averse customer demographics. Let’s look at how Tesla has done selling their products.

2. Tesla’s deliveries…

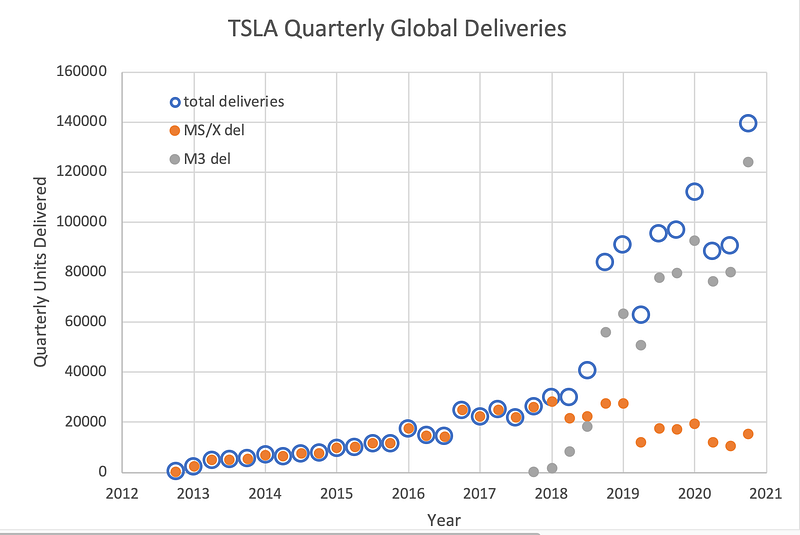

Tesla is unusual in that they define a sale (recognize revenue) as when the vehicle is delivered to its customer. So, unlike most automakers, Tesla views vehicles delivered as a critical metric. The first graph plots the total quarterly deliveries as a function of time. The open blue circles represent total vehicles delivered, and I break down the Models S and X (MS/X) in orange, and Model 3 (M3) in light gray.

Note the growth in Tesla sales occurs in the context of a large decline in US auto sales. We can see the exponential nature of Tesla’s deliveries, and the extremely steep launch curve of the M3, which only started selling in late 2017. The orange dots represent MS/X sales and appear to have peaked in 2018 and is in decline. Every time Tesla shows a downward wiggle in sales, many blame weak demand. I believe the three-year decline in MS/X sales is a temporary consequence of several factors. First, Tesla has been battery-supply limited for several years as it ramped up M3 sales and hit a cell-production limit. Second is the priority on the M3 over MS/X. Rather than reduce M3 production, Tesla, I believe, sacrificed MS/X production.

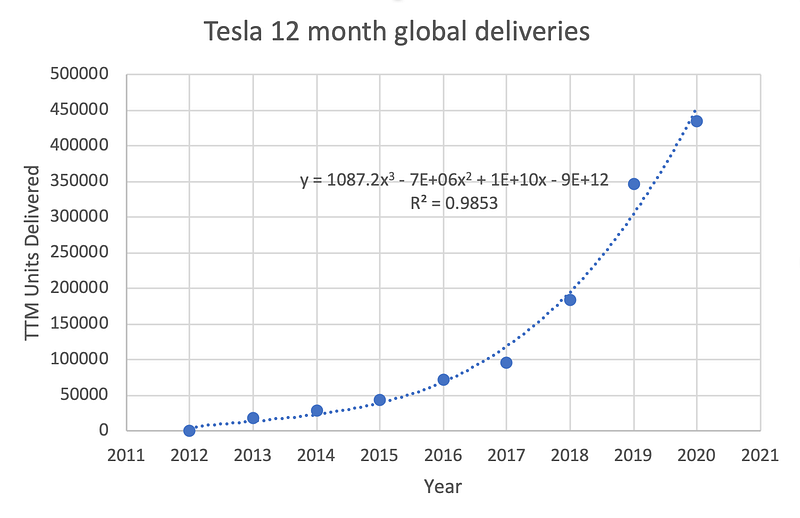

Because deliveries of vehicles are such a chunky metric, and many vehicles are in transit at any reporting period, one way to smooth out the data is to graph a longer reporting period. Here I merely change from quarterly to annual deliveries (using 12-month increments from Q2, 2020, the last reporting period). A best-fit curve shows a third-order polynomial with a very high goodness of fit measure R2. This, duuudes, is the graph of a rocket still accelerating.

3. Tesla’s revenues and gross profits…

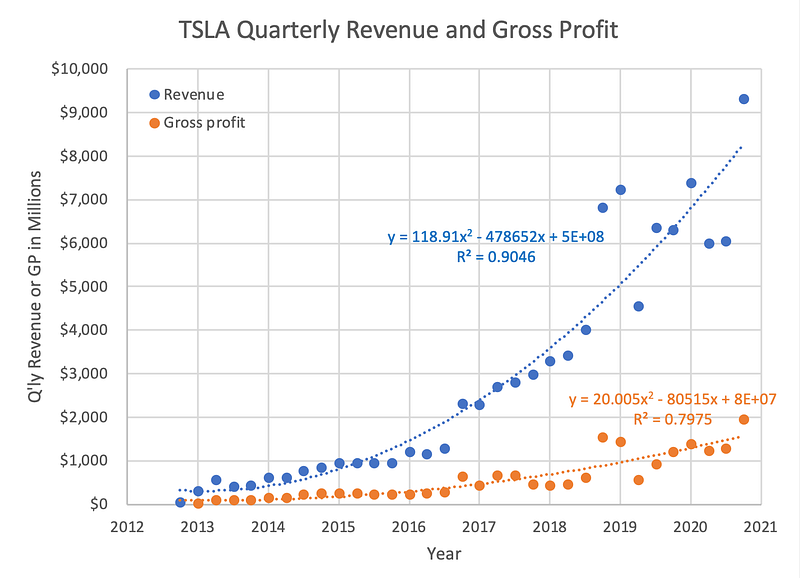

Of course, the measure of a company’s performance is not delivered products, but revenues and profits. In the next graph, I plot quarterly revenues and gross profits (Tesla has not been profitable for most of its history, so I picked a metric which at least illustrates the most basic level of profitability, which is revenues minus the cost of goods sold).

Again, we can see the exponential nature of Tesla’s performance in total sales and gross profits, both increasing rapidly over time. This increase is despite Tesla selling an increasingly large number and percent of the lower-priced M3.

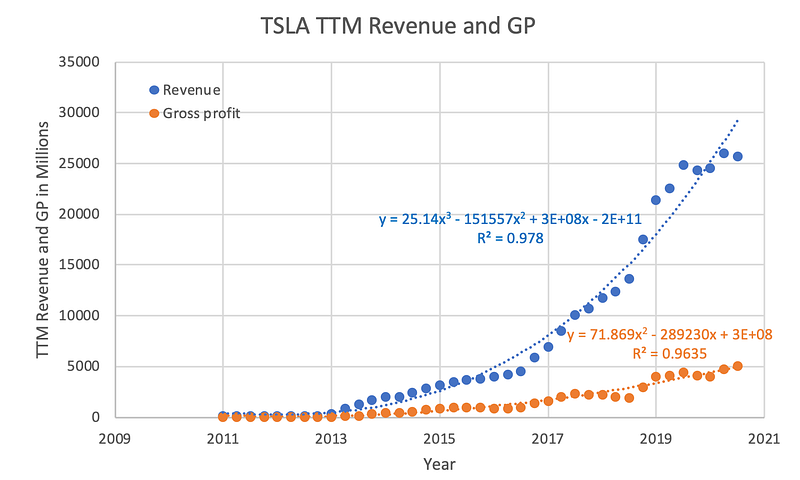

For deliveries, we smoothed the data very effectively by graphing annual rather than quarterly periods. Another common method is to use trailing 12-month (TTM) data, where for each quarter you sum the metric (revenues or GP in our case) over the 4 preceding quarters including the reporting period. We can go through the TTM smoothing for these choppy financial numbers and show similar improvements in the curve-fitting, but either way, the exponential growth rate is unmistakable.

4. Effects of selling more low-priced M3s…

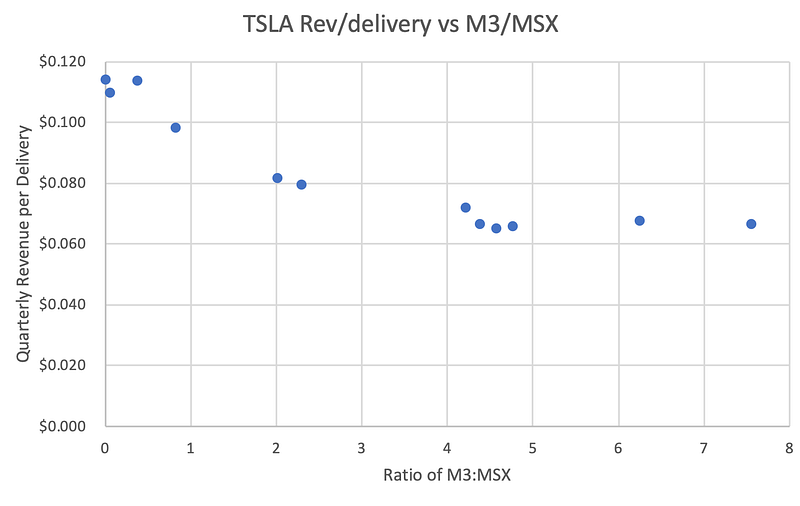

We have eluded to Tesla’s ramping up sales of the much less expensive M3, which can be priced from a half to a third of the MS or MX. The natural concern is that revenues per unit will decrease, affecting overall revenues and profits.

We can make a couple of simple calculations to see if this is a real concern.

As more and more M3s are sold, the ratio of M3 to MS/X will increase and is one variable we want to watch. The hypothesis being that revenues and profits will decline as the ratio M3:MSX increases and will put Tesla in peril.

We can similarly divide total quarterly revenue by the total deliveries made that quarter. If more M3s compose those total deliveries, we expect revenues per delivery to decrease.

If we graph these two ratios, what do we see?

Initially, we do indeed see a decrease in revenues per delivery early on in the M3 ramp. When very few M3s were delivered relative to the more expensive MS/X (the ratio is less than 1 on the x-axis), we see a high number for revenues per delivery. The y-axis is revenue in millions, and you see that the average revenue per delivery is close to the price of the MS and MX.

But we see a fascinating thing as Tesla delivers more and more M3s over time — the most recent reporting period is Q2, 2020 where the ratio of M3:MSX is about 7.5. The total revenues per delivery have flattened out. It has stopped decreasing.

What could be happening here?

One possibility is that Tesla is selling less and less of the lowest trim/lowest priced MS, and those buyers are instead buying the highest-trim/priced M3.

Indeed, we see reports that Tesla planned to stop selling the lowest-priced MS and MX vehicles as of early 2019. By July 2019, Tesla had discontinued the Standard Range versions of the MS/X.

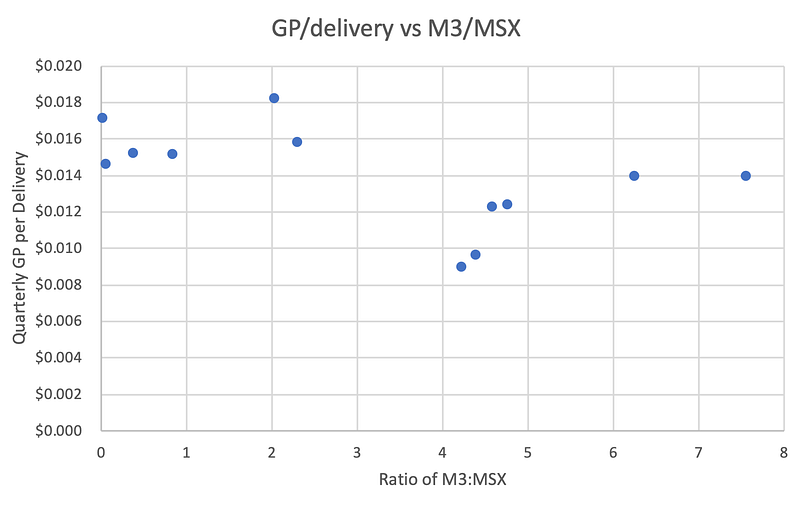

We see a similar thing with gross profits (GP), where initially there was a slight drop in profitability as more M3s were sold. But, more recently as M3s have far outsold the MS/X, the GP per delivery has plateaued, just like revenues per delivery.

Many positive and controllable factors can contribute to a plateauing of gross profit. Increasing production volume means Tesla can ask raw material suppliers to charge lower unit costs. Direct labor also contributes to COGS (cost of goods sold), so increased automation (lower labor) will increase GP.

Tesla has shown a willingness to continually invest in additional automation, as reported by Electrek in May 2020.

5. Looking ahead into the near future…

Tesla has already reported its production and delivery numbers for Q3 2020 here. Those numbers are included in the graphs above. Can we make a couple of small projections using the numbers we have calculated so far?

Tesla reports revenues only if a vehicle is delivered. We know they reported 140,000 total deliveries. And we calculated the revenue and GP per delivery for Q2 2020. Multiplying those numbers, we get possible vehicle revenues of $9.32 billion and vehicle gross profit of $1.96 billion in Q3.

Tesla is far more than a car company, though. They also design, manufacture, sell, and service energy products: solar systems and battery energy storage systems. These currently comprise a small, but rapidly-growing segment of Tesla’s business. Since the numbers for the energy segment are so small and variable, I’d rather not try to calculate Q3 numbers.

I believe that currently, Tesla’s energy business is too small for them to prioritize it, and continuing the ramp of the affordable M3 and MY sales is their main focus for now. But I also believe Tesla’s energy division will continue to grow rapidly, and someday it may be the tail that wags Tesla’s automotive dog.

6. Risks…

Any company is subject to risks. Those risks directly impact us investors. So, it makes sense to have a direct view of those risks, and to try and understand them as best we can. Companies are required to enumerate the risks they see in their financial documents such as Tesla’s most recent 10K.

But we should also use our own investing eyes, and look out at the business landscape and see if we can identify risks ourselves, and evaluate whether the company is poised to handle them. Here is my partial look at some of Tesla’s risks (which may or may not be included by Tesla in their financial disclosures).

Strategic risk: Tesla is disrupting the automotive industry as we watch. The question is whether Tesla itself is open to being disrupted in turn. The core technology for Tesla is the energy storage Li-ion cells. Tesla has hired some of the best battery experts in the world including Prof. Jeff Dahn and his group in Halifax, Canada. Tesla is actively keeping an eye on battery developments around the world, so I believe the risks of disruption are small. Another core technology is one that is not yet deployed, which is full self-driving. Tesla is in the lead for this technology, though its deployment may be delayed even longer than it has already been. Another strategic risk is a demographic change in transportation needs. The Coronavirus pandemic has changed how many of us work, with work from home becoming a norm for many. If this or similar events dramatically change how many or how often we buy a new car, this could pose a significant strategic risk to Tesla. However, this would be an industry risk, and Tesla’s automaker competitors are likely less adaptable and less likely to survive such major consumer shifts.

Compliance risk: Tesla has already been investigated by government regulators for accidents involving their Autopilot. Tesla has come away unscathed in all these investigations to date. We can expect compliance risk to initially increase with the release of full self-drive, though the quantity and quality of safety data Tesla generates may mitigate those risks.

Financial risk: The risk from large capital investments and the relative degree of exposure to loans and other obligations has decreased as Tesla’s financial health and strength increase. Tesla is no longer a startup company trying to build its first factory. The process of building Gigafactories appears now to be almost standardized. The fact that Tesla is a highly sought corporate citizen by many states and countries, mitigates those financial risks through offered grants, low-interest loans, and special tax treatments. The rapidity with which the Shanghai Gigafactory was built and brought online, mitigated much of the financial risk from the Coronavirus shutdown in California earlier this year. As Tesla expands globally, this will further mitigate local financial risks as production can be partially accommodated by other factories. Tesla is now largely self-supporting which is a major mitigation of financial risk.

Operational risk: The Coronavirus pandemic is a classic example of an operational risk as well as a black swan event. I am pretty sure that no corporate risk statement included a pandemic — and I hope that changes now. As stated for financial risk, the opening of globally distributed Gigafactories mitigates some of the local operational risks, just as Shanghai partially covered for the loss of operations in the U.S.

7. Elon Musk’s vision and goals…

We, as individual investors, do not want to breathlessly follow each quarterly call and dance to the tune of Wall Street and big institutional investors. For us small retail investors, the regular Joes, the dumb money as Wall Streeters like to call us, a calm, slow-acting, long-term buy and hold mentality is the statistically more reliable path to investing success than having a squirrely trigger-finger.

While it is fun to dig into quarterly numbers for a company you have invested in, often the short-term scrabbling among the undergrowth means you lose the forest for the trees, as the cliché goes.

Keeping a broad view of the company and its leadership, and a loose rein on the often highly variable quarterly numbers is much more productive for investing and for peace of mind.

So, how do we view Tesla and its leadership?

I think of Elon Musk as one the most divisive, disruptive, creative, and successful entrepreneurs of the 21st century — who will gift the future with either a step-change in technology or with endless cautionary tales and missed opportunities.

So I said in the introduction of my article on Starlink, here.

Tesla was founded in 2003, and Musk has been at the helm in one form or another since 2004. For Tesla, unlike Starlink, we are currently in the midst of the step-change.

Musk’s stated vision of that step-change is to “expedite the move from a mine-and-burn hydrocarbon economy towards a solar electric economy.”

Musk’s goals for Tesla were first articulated in his 2006 “Secret Master Plan” here, which he summarized as:

1. Build sports car

2. Use that money to build an affordable car

3. Use that money to build an even more affordable car

4. While doing above, also provide zero emission electric power generation options

Those have been mostly fulfilled (1. was the Roadster, 2. was the Model S and X, 3. was the Model 3 and Y, and 4. is their ongoing solar efforts).

In 2016 Musk published his “Master Plan, Part Deux” here, which he summarized as:

1. Create stunning solar roofs with seamlessly integrated battery storage

2. Expand the electric vehicle product line to address all major segments

3. Develop a self-driving capability that is 10X safer than manual via massive fleet learning

4. Enable your car to make money for you when you aren’t using it

The solar roof is having birthing pains, not unlike the schedule-stretching, years-long incubation of the Model X. Tesla’s Solar Roofs are being sold and installed, though slowly. Home and commercial energy storage is doing better and is growing rapidly and has also seen high-profile installations around the world. So, goal number one of Part Deux is very much a work in progress.

Tesla currently has four production models, S, 3, X, and Y. Yes, Musk did that intentionally (as did I). Tesla has also announced the Cybertruck, the Semi, and a revamped Roadster. The announced vehicles have apparently stalled, though the Semi is getting some visibility and high-profile buyers. The Cybertruck has the priority for resources among the three. Again, goal number two is a work in progress.

Self-driving is also undergoing a long gestation, but Tesla remains far ahead of the pack with far more relevant data (real users driving on real roads under real weather conditions) with which to train their AI. There is new news about a beta test with selected drivers. Goal number three may have the highest priority and intensity of development of all projects at Tesla, but may also have a longer unexpected gestation time than either the energy or automotive products — because it is a much harder problem.

Goal number four is highly dependent on goal number three, so as far out as self-driving is, so is the sharing economy for cars as Musk envisions it.

Nonetheless, these goals are disruptive and transformative to the industries and segments of the economy that they touch. There are no guarantees in business or investing — but if there is one place to put an investable amount (an amount where you can stomach the volatility) — I can think of no better place than Tesla.

8. Disclosure…

I am a happy owner of just about the oldest used Tesla Model S (a 2013 MS P85), and am also happily invested in Tesla the company.

You may also like the following recent articles. This one is an introduction to SpaceX’s Starlink:

And this is a follow-up article on Starlink’s recent beta test:

Finally, this article is a deep look at Netflix’s culture:

Thank you for reading, and please share!