How To Prepare Your IRA In Your 20s And Have An Annual Return Of 46%

How to achieve financial freedom with minimal effort and without complex financial knowledge.

The majority of the world’s population has its pension plans in very low-risk assets such as TIPS, Treasury Bills, Short-Term Bonds… Sadly, when these people are about to withdraw the money from their pension plan, they realize how much purchasing power they have lost during this period. Many of those who do not invest in these assets have their accounts linked to actively managed pension plans with management fees of around 2%, unacceptable fees when they do not provide that extra return compared to the benchmark indexes.

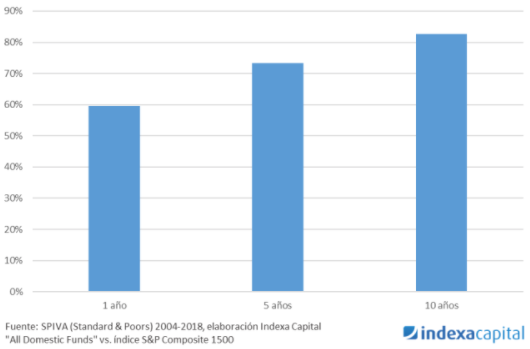

Historically, the inability of most active managers to beat their benchmarks over the long term has been demonstrated. Below, I show the percentage of active funds that fail to beat their benchmark over 1, 5 and 10 year periods.

As you can see, over 10 years 82.7% of active managers have been unable to beat the S&P Composite 1500 index. This figure is even higher when we extrapolate it to 30 years since it is around 99% in that period.

That is why in my own pension plan portfolio I only invest in the ACWI world index, an index that includes not only the developed countries but also the emerging ones. Who can assure me that in 30 years China or India will not be the world’s leading power?

The main reasons that have made me choose this type of fund are the following:

- Low fees

- Global diversification

- No financial knowledge is required

- Allow automation

On the other hand, it is important to know the risk that this type of asset has had in the past, as well as what has been their profitability, a good measure that encompasses risk and profitability could be the Sharpe Ratio, and we should try to maximize it.

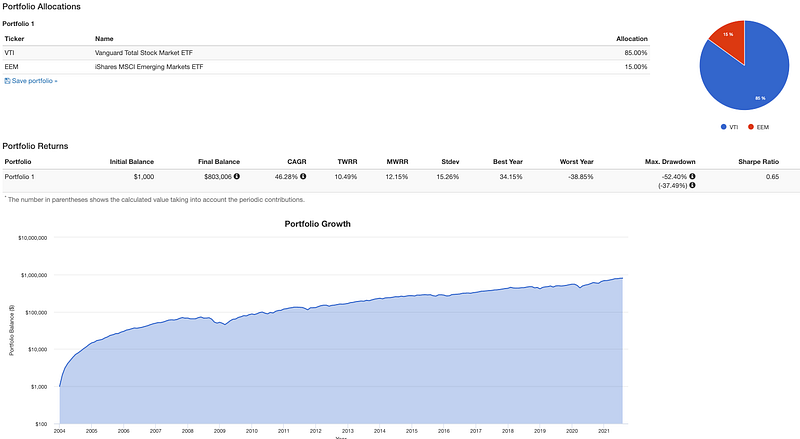

To do this, we are going to perform a backtest from 2004–2021 and check what results we would have obtained by investing in this index. This backtest will have as premises an initial capital of $1,000 and monthly contributions of $1,000. The ACWI index has its origins in 2008, but its distribution between developed and emerging is 85/15, approximately. Obtaining the following result:

As you can see the CAGR is 46.28% (MWR). We know that the TWR is lower but this is one of the advantages of compound interest and periodic contributions.

Final Consideration

If you are at the end of your working life, I would not consider having this asset allocation, since in the event of a sharp fall in the markets you could be several years before they recover. Therefore, it would be necessary to have a greater weight in fixed income and less in equities as retirement age approaches. In addition, if you want to avoid paying a high amount of taxes, it would be convenient to make partial withdrawals distributed over time.

Our purpose is to convey to the individual investor, through our newsletter, simple strategies to have a covered, uncorrelated and asymmetric portfolio as possible so that any investor can implement this strategy for himself. One of the main strengths of this strategy is to be able to sleep peacefully every night and for this, we have between 40–60% of the portfolio invested in fixed income (other currencies, bonds, gold …) and the rest is invested in options or ETFs that make us benefit from any market situation

This article is for informational purposes only and it contains affiliates links, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.