How to Measure the Expected Shortfall of a Stock Investment In Python

You should know how to calculate the downside risk of your stock.

Everyone has to make decisions in the face of uncertainty.

The same goes on with stock trading. Some of the best investors in the world are constantly facing questions like: “Should I sell or buy more?”, “Should I sell everything and invest somewhere else?”, “Should I get rid of this stock altogether?”.

When we think about this we will define the trade-off between risk and return. The first question we have to ask is:

“How do I measure risk?”

There are a lot of ways to measure risk in the world of financial markets.

Let’s see one interesting measure: the Conditional Value at Risk.

Disclaimer: The purpose of this blog post is only to show how to calculate the value at risk of a stock. There is no investment advice or promotion for any stock.

Content

1. What is the Conditional Value at Risk (CVaR)?

Conditional Value at Risk is a metric for estimating expected losses in the worst-case scenarios.

In my previous blog post, I introduced the Value at Risk (VaR) of a stock. The VaR quantifies the risk of potential losses for a firm or an investment over a time period. It calculates a maximum loss within a defined probability range.

CVaR is a conditional measure of VaR and it calculates the standardized maximum loss in every future period given a specific terminal loss.

2. CVaR Calculation

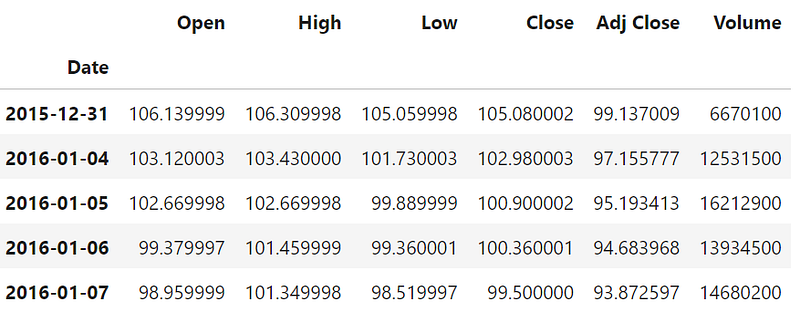

A. Retrieve Stock Data

We import the needed libraries.

We use the yahoo finance library (yfinance) to get the stock data for Disney with its ticker and choose the periods we want.

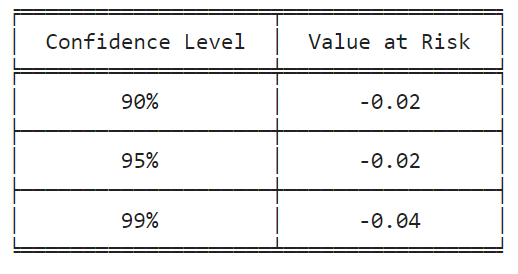

B. Calculate the VaR

Let’s calculate the VaR: we first calculate the daily returns and then use the quantile method.

Let’s present the different measures in a table with the Tabulate library.

How to read it for 99%: Disney’s stock loss will not exceed -4% on a single day with a confidence level of 99% based on its historical values over the last 6 years.

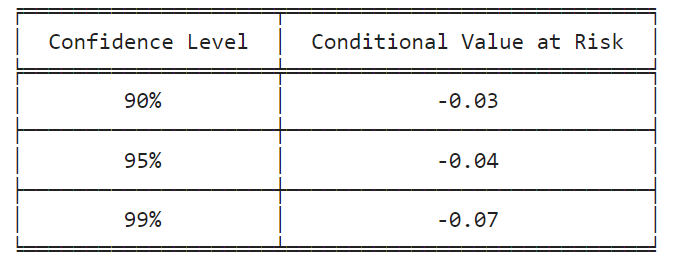

C. Calculate the CVAR

CVaR is also expressed as a percentage. To get it, we filter only the daily returns that are less than the three VaRs we just calculated, and then take the average of these values.

How to read it for 99%: Based on historical values over the last 6 years, Disney stock losses can reach -7% in the worst 1% of cases.

3. CVaR in real life

CVaR must always be greater than VaR because CVaR is based on the worst-case scenarios of returns, which is reflected in the results shown.

Safer investments (large-cap US stocks or bonds) rarely exceed VaR significantly.

More volatile asset classes, such as small-cap US stocks, emerging market stocks, or derivatives, can have CVaRs that are many times greater than VaRs.

Investors prefer low CVaRs. However, investments with the most upside potential frequently have high CVaRs.

Even the best-designed system for risk assessment has its limitations. In fact, there is no such thing as a perfect risk measure.

I hope you enjoyed reading this post! Follow me on Medium to get notified when I publish new posts. It motivates me to continue.

You can also find me on LinkedIn.

References:

Conditional Value at Risk (CVaR) (investopedia.com)

Value at Risk (VaR) Definition (investopedia.com)

Downside Risk Definition (investopedia.com)

Subscribe to DDIntel Here.

Join our network here: https://datadriveninvestor.com/collaborate