How to Invest in Your 20s to be Wealthy in Your 30s

Excellence is exponential — 8 surefire ways to make sure you’re rich by your 30s

There’s a reason the rich get richer.

To those who have much, more will be given. To those who have nothing, more will be taken.

That’s called the Matthew Principle. It’s an economist term ripped straight from the bible. It’s sometimes summarized by the adage “the rich get richer and the poor get poorer.”

Excellence is exponential. The athletes get more athletic. The millionaires become billionaires. And the best musicians keep making the best music.

The same can be said for imperfection. The more we slack off the worse we are the next day, and the day after that. And so on. This is why the younger you start, the more opportunity you’re given to nurture your excellence. It’s also why the most important time to invest is in your 20s.

You reap what you sow, to use another biblical phrase. So, if you plant shit seeds now, you will reap a poor harvest later. I don’t want that to happen to you or me, so this is what you need to do.

Take risks and invest everything you can

Take your biggest financial risks now.

Do not think about what you stand to lose in an investment, think always of what you stand to gain. The stock market is not a casino if you do your due diligence. This means starting to invest in companies you trust and researching them on websites like Morningstar or CNBC.

Invest in stocks. Invest in exchange-traded funds. Invest in cryptocurrency.

Buy them and hold. Don’t sell if the price drops because you did your due diligence and believe in your investment long-term.

This is what $1000 would have earned you in 2020 from these investments:

- ARK Innovation ETF [Tesla, Roku, Spotify, Zillow]: $1520 (152% Growth)

- Bitcoin: $3000 (300% Growth)

- Tesla: $7430 (731% Growth)

You’re in your 20s.

You know what companies are innovative. You know what’s on the up & up. I invested in Tesla back in 2020 because I thought Elon Musk was a genius. I didn’t want to bet against him. To me, betting against him was to not invest in him.

Invest as much as you can — much more than the tiresome advice of 10% — in the companies you use every day and trust.

Live like you’re poor

Every time I spend $15 on a meal I think I actually spent $100.

Once you learn how to invest you will be able to turn every dollar into two. Sometimes three. It’s like a superpower.

This is why you save wherever and whenever you can. Spend more on groceries and less on eating out. Go through your bank statements with a scalpel and cut out any expenses you don’t need.

Moreover, do not forget that you can live broke in your 20s and no one will bat an eye. There’s nothing to be embarrassed about. When you turn 30, it’s a different story.

Surround yourself with investing-minded friends

Your 20s is the time to cut out bad friends.

A bad friend in college gets you into trouble or embarrasses you in front of your crush. A bad friend in adulthood can ruin your life.

They’ll make you spend more. They’ll tell you that your 20s is the time to wreck your life and then build it up in your 30s. They’re selfish for all the wrong reasons.

Choose your friends wisely.

The people you interact with every day have a profound impact on you. If they are all negative influences then it could be setting you up to fail your 20s and scramble around to fix it when your 30.

Save to invest. Don’t just save to save

Good investments protect our purchasing power. Think of purchasing power as the amount of goods or services that your money can buy.

Purchasing power isn’t limited to cash. Assets like gold or Bitcoin are skyrocketing in value because the U.S. is printing more cash but producing fewer goods. This is leading to inflation.

The interest rate in your savings account does not beat the current rate of inflation. Banks do not protect our purchasing power anymore.

This is why Elon Musk just moved a significant amount of Tesla’s money into Bitcoin. He wants to protect his company’s purchasing power.

I’ll ask the question again: Would you bet against Elon Musk? I’m not. And that’s why I invest in Bitcoin and other digital currencies.

Have multiple income streams (Build leverage)

“A salary is just the drug they give you when they want you to give up on your dreams.”

Kevin O’Leary said that.

Don’t become a slave to one stream of income. Not only do you lose out on new avenues of creating wealth, but more importantly, you lose leverage.

If you hate your job or your boss, you’ll have no choice but to stay because you have nothing for leverage. You’re trapped because you don’t have multiple streams of income. Don’t procrastinate and let this happen to you.

Some easy ways to make extra money are investing in stocks, taking up a new side hustle like freelance writing, or creating a product.

Here are a few more of my favorites.

Open a Roth IRA and become a millionaire when you retire

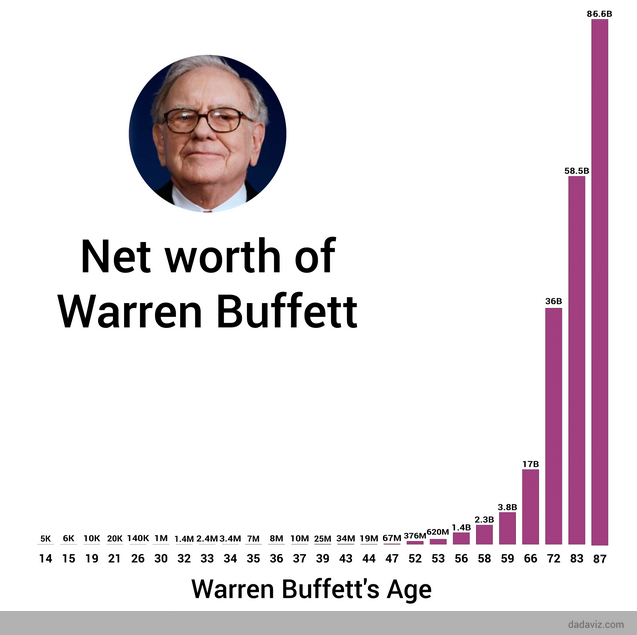

Warren Buffet played the long game to become a billionaire.

Buffett is worth about $86 billion. The majority of his wealth (99.7% of it) was created after his 52nd birthday.

A Roth IRA works in a similar way.

If you max out your annual contributions of $6,000 to the tax-free retirement account you’d become a millionaire at age 55, after 33 years and four months of contributions. Barring any global nuclear wars or mass global chaos during the next 33 years [*knocks on wood].

$6,000 a year may seem steep, but if you dollar-cost average into a Roth IRA then it becomes much easier psychologically speaking.

Reconsider College

If I had children today, I couldn’t foresee a situation where they went to college. They can travel around the world and back. Enroll in a coding or U/X bootcamp. Or they could go to a trade school.

But I’d warn them against going to college unless that’s absolutely what they wanted to do. Even then I’d ask them if they’re sure.

College does more harm than good. It saddles you with debt, equips 90% of its students with useless degrees, and indoctrinates you with one ideology. According to this study, almost the entirety of all college professors subscribe to left-wing politics.

I want my kid to know there’s more than just one way of thinking. I don’t want them to waste four years in a place that limits their mind rather than open it.

If you’re in college or thinking of going, you should reconsider. And don’t let sunk-cost fallacy be the sole reason you stay.

Learn the difference between good vs. bad debt

Philosophers say the world is made up of two things: tools and objects. Economists, however, call these assets and liabilities.

Look around your room. What’s an asset? Is your television an asset or a liability? How about your favorite books? What helps make your life better, and what makes it worse?

When you spend one dollar on a liability, that dollar is gone forever. But when you spend one dollar acquiring an asset, that asset works for you now. You’re its boss and it will work relentlessly to make you money.

It’s ok to lose money if you’re buying an asset. This is good debt.

Bad debt is spending money on liabilities. It’s signing up for a credit card to buy a newer phone or buying $300 headphones when $100 ones would have sufficed.

If you can figure out the difference between assets and liabilities, nothing will stop you from being wealthy in your 30s.

Final Thought

Gary Vaynerchuk once said your 20s is the time when you don’t blink.

Right now you need to put your head down and build the pillars of your life. You will look back on your 20s and remember it as the time you propelled your life forward or squandered your potential.

Remember: the world is much more forgiving when you’re younger. As long as you’re trying, many people will take chances on you because they don’t care that you don’t have everything figured out; they care that you’re trying your best in spite of your lack of experience.

Make prudent decisions now and you won’t regret them later.

Consider checking out my new book “Mind and Muscle” linked here.