How To Get Wealthy In Two Simple, Fast Steps! Expanded.

(Most) everyone knows you should probably save some money. I say “most” because if you have ever listened to or watched Dave Ramsey or Caleb Hammer, you know too many Americans lack basic financial education.

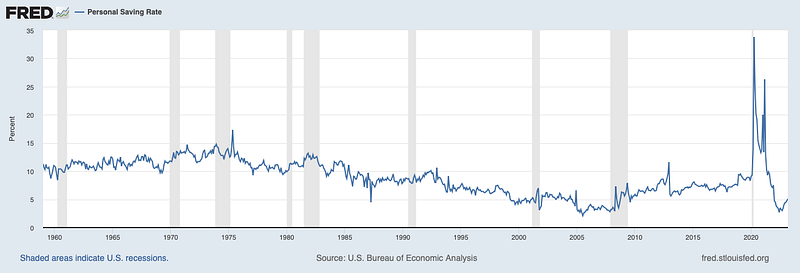

But, if that’s true (knowing you should save), how do we explain charts like this?

So, when I first wrote about the two simple steps to get wealthy, 1) Spend LESS than you bring home in Income sources, and 2) Save and invest the difference in things you know and understand…

I did so in a rather glib manner, failing to take into account that for many Americans, it just isn’t so easy.

As I have highlighted before on this blog, for a majority of Americans, life is just getting too expensive.

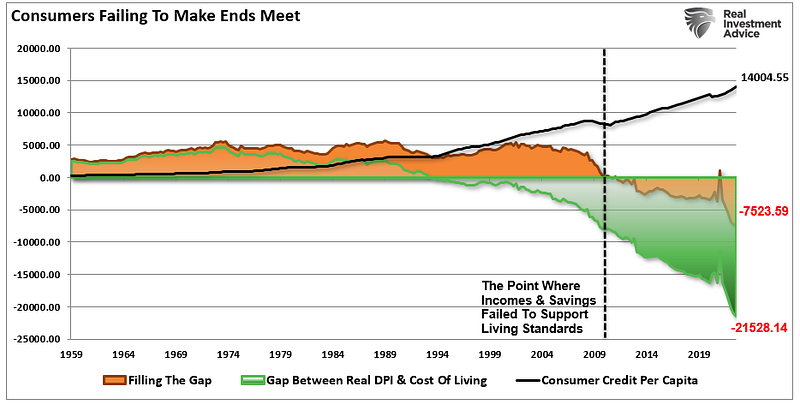

As you can see, in 2022 the gap between COL (Cost of Living) and (DPI) Disposable Personal Income reached about $20,000 annually.

It has been this way since about 2010.

All the while, as inflation rages, Real DPI has taken a hit.

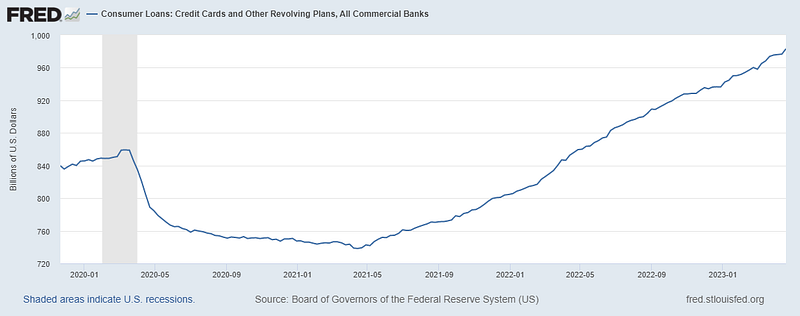

This reality is apparent when examining credit balances.

BLS data shows why the math doesn’t work. For the 45 to 54 age Demographic (America’s highest earners) the 2022 Median Annual Income was $61,412.

Even people in the top 10% of earners in America are often struggling to make ends meet.

So how exactly is anyone supposed to save money?

Ok, Matadore, we get it! So where are you going?

As Morgan Housel highlights in his must-read The Psychology of Money, success with money involves both personal experience and behavior.

The aforementioned money celebrities (Ramsey and Hammer) are all about breeding behavior changes in their broke subjects. Dave likes to regularly remind us that “personal finance is 80% behavior, 20% knowledge”. (I agree, but behavior is learned and is thus a form of knowledge.)

America’s problem is Consumerism.

I will not regurgitate this excellent article from the APA but suffice it to say, Americans are repeatedly barraged with societal, credit, and psychological assaults that make the valuation of stuff more important than anything else.

Again, watch an episode of Ramsey and Hammer and tell me the reason people are in debt is for any good reason. Useless degrees, restaurants, cars on credit, you name it.

What many of these people fail to understand or practice is that saving even small amounts of money, weekly, monthly, etc., can yield tremendous results over the decades.

I know this sounds elementary, and if you are reading personal finance blogs on Medium, you likely already understood my initial post, “How To Get Wealthy In Two Simple, Fast Steps!”

But, clearly, many Americans do not get it.

What if people traded Consumerism for Compounding?

Back to Morgan Housel’s book, the human mind is not great at conceptualizing compounding. The math gets too hard and the numbers become both abstract and unbelievable.

Housel presents the experiment of calculating of 8+8+8+8+8+8+8+8+8 in your head being rather simple (it equals 72).

He then asks the reader to calculate 8x8x8x8x8x8x8x8x8.

Yeah, you need a calculator. That equals 134,217,728. A massive and inconceivable number using the same series of 8s.

Here in lies the power of compounding.

We have covered on this blog before the average car payment in America is a staggering $648.

$648 a month for a depreciating asset so you can look cool at the stop light for people you don’t know that don’t know you.

Again, what if Americans traded Consumerism for Compounding?

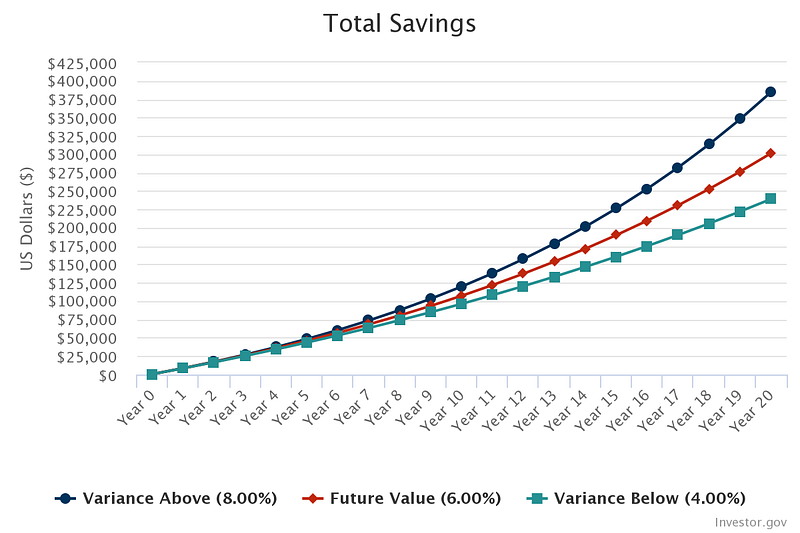

Here is what $648 a month invested every month for 20 years, with an interest rate return variance of 4% to 8%.

From $250,000 on the low end to $375,000 on the high end.

$375,000 vs. a car* that will likely be worth nearly $0 in 20 years.

I am not a “budgeter”. I prefer getting after it on the income side and practicing mindful spending while avoiding debt. But, I would wager most Americans, especially the top 10% of earners, can easily find room in their budget and divert “wants” to saving and investing. Even lower-income Americans can leverage small amounts of regular savings for a powerful return.

Consider how long it’s taken Warren Buffet to amass his fortune! Americans think too short term. Nothing good happens overnight.

Time is the key, combined with good behavior.

Our needs cover shelter, food, and utilities. Most everything else is a want. Americans love wants.

Once we understand the power and concept of Compounding, we can make a choice to better our tomorrow and improve our financial well-being.

Thanks for reading. Be good stewards of your earnings.

*There are exceptions to the rule.