How to get a 32,000% return during Covid-19

The market is full of inefficiencies and ‘black swans’ from which you can get stratospheric returns

During 1950 several economists laid the foundations of the Modern Portfolio Theory, one of the most important was Black-Scholes (BS), whose formula served as a reference for the valuation of options for a long period of time, in fact, today it continues to study and use in academia. This formula tried to include the price of financial options under a normal distribution. What Black-Scholes did not take into account is that in the world of finance there are extreme situations that go beyond said distribution, as was the case of Covid-19.

This strange event is found within the tails of the distribution (> 5 sigmas), which means that following the BS assessment, the probability that an event of this type will happen is 0.0014 events every 10 years when it has been proven that in the world of finance 7 occur every 10 years. As I describe in my first article, I think we should be covered in these types of situations.

For this specific case, we are going to see what would happen if a person had covered their portfolio in these types of situations. The SP500 volatility index (VIX) will be taken as a reference for the study.

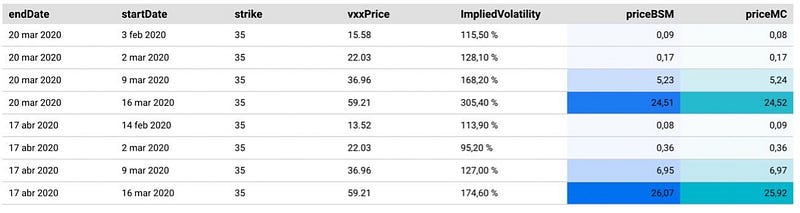

On the one hand, very OTM options are bought on February 3 and 14, 2020 and whose expiration dates are March 20 and April 17, 2020, respectively. We see that the price valued by the Black-Scholes method (PriceBSM), causes the price of the options at the beginning to be only $ 0.09 per contract.

On the other hand, we see that by maintaining these contracts until March 16 (even though the worst day was the 18th, it has not been chosen to avoid overfitting), the contracts would have reached a price of $ 25 per contract, approximately. Which makes a return of 32,000%.

These returns would have offset 33 years of periodic contributions to this strategy, while these events occur much more frequently without going any further in 2000 and 2008 and will occur again, being of a much stronger magnitude if the central banks continue to carry it over with more debt.

Conclusion

I am in favor of having an asymmetric portfolio that allows, on the one hand, to have assets with very little risk (short-term bonds, gold, other currencies) and, on the other hand, assets with a very high risk, as is the case that I present in the article. This allows me to have a totally uncorrelated portfolio that benefits from market inefficiencies and with a very limited possibility of loss. These types of investments are tremendously complicated to follow and you must have a good knowledge of what you are doing since the irrationality of the market, normally, lasts much longer than the investor’s patience.

Another ‘fat tail’ useful example

In addition, we have a newsletter where we publish weekly all the movements made, where our only mission is to minimize the ‘risk/reward’ equation as much as possible. As Taleb would say: ‘I am not a risk manager, I am a risk-taker’.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.