Your financial freedom depends on the choices you make…

How to Figure Out How Soon You Can Retire

Figure Out Your Personal FIRE Point

FIRE, the acronym for Financial Independence, Retire Early, connects with many people’s dream of “firing” their boss. Do you know how long it’ll be before you reach that point?

If you don’t, there’s an easy hack to figure that out…

A Good Starting Point Tool

On his “Four Pillar Freedom” blog, “Zach” shared his Early Retirement Grid, showing how many years you’d need to reach your FIRE point. He based his grid on current after-tax annual income and annual spending. The assumptions behind his results include:

- $0 currently saved for retirement

- 5% annual return on investments

- 4% initial draw in retirement

I love the idea behind this tool, but found several significant issues:

- The grid only works for incomes of $25k-$100k and annual expenses of $20k-$95k.

- It excludes the possibility that you may want to draw more in retirement than your after-tax, after-savings income.

- It ignores a critical factor — inflation. This will gradually increase your expenses in dollar terms, even if you keep buying identical products and services.

- It ignores increases in your income.

- The 5% annual return seems too low. If you have no retirement savings you’re probably young enough to accept market fluctuations and invest 100% in equities. Equity returns have historically been much higher than 5%, even after accounting for inflation.

- According to recent research, 4% initial draw appears to be too aggressive given likely future market returns.

Addressing the Limitations of the Four Pillars Grid

To address the above shortcomings, I decided to create my own tool. This tool estimates the years until your FIRE point for a given savings rate and income replacement rate in retirement. I too assumed $0 already saved for retirement, but made a few other adjustments to help improve accuracy.

- Since I don’t assume any specific income, my grid works for all income levels.

- I include cells above the diagonal, because if you’re uber-frugal now to save aggressively, you may choose to work longer for a more comfortable retirement.

- Since I look at the replacement rate for your income in retirement rather than annual expenses in dollars, we can safely ignore inflation.

- The assumption I make is that your income will more-or-less track inflation. This isn’t perfect, since income often increases faster than inflation. However, it’s less inaccurate than assuming constant income in nominal dollars.

- My annual investment return assumption is 6% above inflation. Historically, equities returned more than 6.9% annualized from 1927 to 2019 after adjusting for inflation.

- My initial draw assumption for retirement is 3% of your portfolio, in line with recent research.

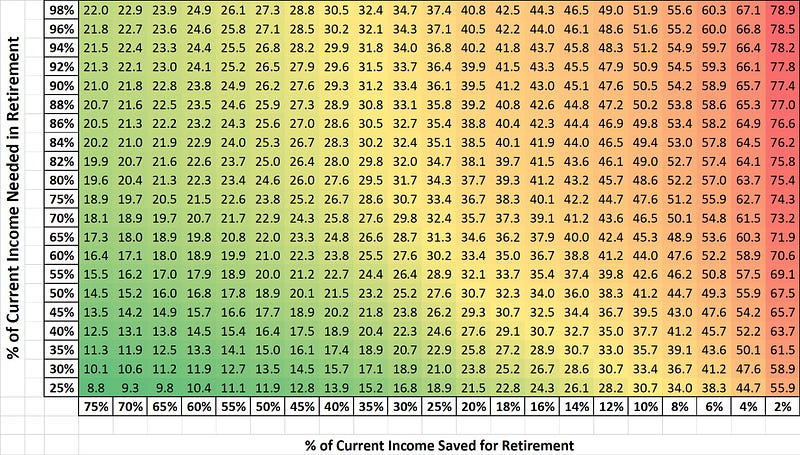

How Soon You Can Reach Your FIRE Point

So, without further ado, here it is…

This grid shows how long it will take you to reach FIRE, depending on your retirement savings rate and your desired retirement income replacement rate.

To see how you should use the tool, let’s walk through an example.

No matter your income in dollars, if you’re saving 30% toward retirement, look at the column with 30% in the lowest, white cell. If when you retire you want to replace 70% of income, go up that column until you reach the row with 70% in its leftmost, white cell.

This shows you’ll need 29.8 years to replace 70% of current income.

Move three cells up to see it will take 32 years to replace 82% of your income.

What the Data Show for Your FIRE Point

The Cost of a Low Savings Rate

If you’re 22, want to replace your non-savings income, and save only 6%, you won’t likely be able to retire much before age 82!

The Power of Increasing Your Savings Rate

If you save 10% of income and plan to replace 90% of income, you’ll need 50.5 years to retire!

Increase savings to 30% and reduce retirement income to 70%, you’ll reach FIRE in 29.8 years.

That saves you more than 20 years of work! Save half your income and live on the same after-savings income in retirement and you’ll reach FIRE in 18.9 years, saving you another decade of work!

The Power of Working (a bit) Longer

As mentioned above, save 30% of income and plan on the same 70% you spend now, and you’ll need 29.8 years to reach FIRE.

Work just 2.2 years (7.4%) longer, and you can replace 82% of your income. That’s a 17%+ increase in your retirement income!

Savings Rate Needed for “Normal” Retirement Age

Say you’re 22, plan to replace all your non-savings income, and want to retire by 67. You’ll need to save over 12% of your income for retirement.

The Impact of an Employer Match Depends on Your Choices

Say your employer match your savings dollar for dollar up to 6%. Say you then use that to reduce your own contributions from 12% to 6%. Your replacement rate now needs to be 94%, pushing back your retirement by more than 3 years, past age 70.

On the other hand, if you continue saving 12% and use the 6% match to accelerate your savings, expect to retire before age 63.

The Impact of Social Security Benefits

Say the Social Security Administration’s current estimate of your benefits promises to replace 25% of your income. Let’s then admit that at best, they will deliver 80% of that, or 20% of your income. If you start with 30% savings and 70% replacement, Social Security will shave 4.6 years off your FIRE time.

The Bottom Line

The grid above lets you estimate how long you need to reach your own personal FIRE moment, depending on how aggressively you save and how much income you’ll want in retirement.

Using percentages lets you to use the tool no matter how high or low your income. The above examples walk through the impacts of low savings, increased savings, working longer, employer match, and Social Security benefits.

About the Author

Opher Ganel has set up several successful small businesses, including a consulting practice supporting NASA and government contractors. His most recent venture is a financial strategy service for independent professionals. You can connect with him there, or by following his Medium publication, Financial Strategy.

Disclaimer

This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

Originally published at https://wealthtender.com.