Why Conventional Wisdom About How to Allocate Your Investments May Be Wrong

This Is When Being 100% Invested in Equities Makes Sense

And when it starts breaking down…

Here’s a shocker — Americans are woefully unprepared for retirement, saving far too little, and having set aside only a tiny fraction of what we’ll need to be able to retire.

Despite what many fear, Social Security will still be around, but benefits will likely be reduced and may start at a later age, making an already insufficient source for retirement funding even worse.

According to the Social Security Administration’s actuarial tables, Americans aged 67 have an average life expectancy of just under 18 years. Over that length of time, the long-term-average annual inflation of 3.1% would reduce the purchasing power of your cash by 42%. This means that stuffing cash under your mattress is a really bad idea (and not just because sleeping on a lumpy surface is uncomfortable), because your money has to grow fast enough to beat inflation.

Since 1926, stocks have averaged a real (after-inflation) return of about 7%, while bonds lagged at about 2%. Clearly, having most of your portfolio invested in equities is the better bet over the long term, but short-term volatility is cited as the best reason to diversify at least some of your investments in bonds.

This raises the question — how much should you keep in stocks?

Old Rules Get Updated

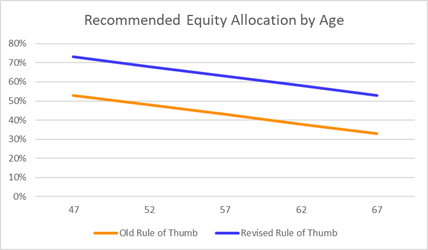

The old rule of thumb told us to subtract our age from 100 and use the result as our equity percentage allocation. At age 47, that would be 53%, dropping by a percentage point each year, reaching 33% at Social Security’s full retirement age of 67 (for those born in 1960 or later) as shown by the orange line in Fig. 1.

However, now that Americans are living longer, that old rule needs to be tweaked. According to CNN Money, many financial planners now say you should set your equities allocation by subtracting your age from 110 or even 120, lifting those allocations to as high as 73% for 47-year-olds, gradually dropping to a still significant 53% for 67-year-olds (blue line in Fig. 1).

The Case for 100% Equity Allocation

However, the case can be made for a 100% equity allocation until fairly close to retirement.

Say your income is $75,847 (the median in Maryland). According to the 4% rule, you’d need a retirement portfolio worth nearly $1.9 million to replace 100% of that income for a long retirement. Let’s further assume that your early Social Security benefits will be $19,847 (to make the math easy). That reduces the annual income your portfolio needs to replace to $55,000, and your needed portfolio size to “only” $1.375 million. Let’s further assume that you can and do set aside $500 per month, or $6000 each year.

What nobody seems to realize is that a significant part of your resources is already more bond-like than stock-like.

I’m talking about your earning potential. Think about it. Unless you’re unemployed, still a student, or already retired, you get a salary (or business income) every month and that’s expected to continue until you retire. You may argue that you could lose your job, but that can be likened to a bond issuer defaulting. Another possible objection is that a bond returns its face value at maturity, while not many of us get a huge lump sum at retirement. Enter Social Security. That stream of lifetime payments is worth a lot. For the above assumption of $19,847, that value is nearly $500,000 according to the 4% rule.

Regardless of the details, if you consider that your ability to earn money behaves much more like a bond than like stocks, your de-facto bond allocation is much higher than you think, and probably higher than it needs to be, unless you’re within a few years of retirement.

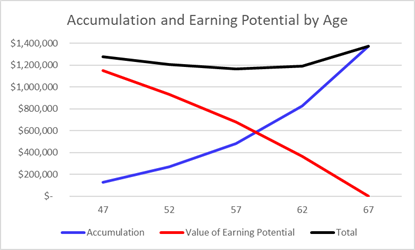

So, if we were to liken your earnings to the flow of bond coupon payments or an annuity, how much would it be worth? Using Charles Schwab’s annuity calculator, the value of a 20-year period-certain, set-amount, immediate annuity paying $75,847/year from age 47 is (as of this writing) just under $1.15 million. A 15-year annuity from age 52, is worth more than $930,000. A 10-year annuity from age 57, nearly $683,000. A 5-year annuity from age 62, over $360,000 (red line in Fig. 2).

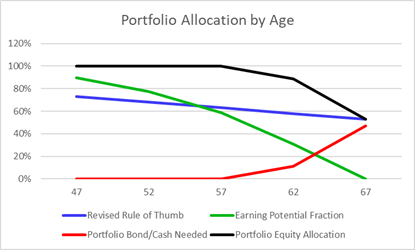

What does this mean for your equity allocation? To answer that, we need another assumption, that you’re on track to accumulate $1.375 million by age 67 by setting aside $6000/year. For that to be true, you’d need to have about $130,000 by age 47, $270,000 by age 52, $483,000 by age 57, and $826,000 by age 62, leading to the $1.375 million at age 67 (blue line in Fig. 2). This means that your ability to earn is nearly 90% of your resources at age 47, almost 80% at age 52, just under 60% at age 57, over 30% at age 62, and of course 0% once you retire at age 67 and no longer work (green line in Fig. 3).

Compare these to the bond/cash recommendations from the revised rule of thumb we saw above, of 27% for 47-year-olds, increasing by one percentage point per year up to 47% for 67-year-olds (complement of blue line in Fig. 3), and you’ll find that you have more than enough “safe” resources up to age 57, almost enough at age 62 where you’re missing just 11%, becoming 47% shy by retirement at age 67, where your earning potential has zeroed out (red line in Fig. 3) — so you may want to shift 47% of your portfolio out of equities by then.

Caveats

The above analysis is only intended to make a general point, that your earning potential can count toward your bond allocation, allowing you to invest more aggressively until shortly before retirement. This means there are some caveats that prevent you from taking the details too literally.

- Your income won’t stay flat throughout your working life, likely growing until your late 50s and starting to decline after that.

- It’s a given that your case will not identically match the above example scenario, since your existing portfolio value, your salary, and your retirement needs are extremely unlikely to all exactly match the values assumed above.

- Inflation, stock returns, and bond returns will all fluctuate over the years and decades. Using average values for all years is a simplification.

- Interest rates will change over time, affecting annuity costs and through them the details of the analysis.

- Finally, this analysis assumes that you don’t plan to leave a large bequest to your heirs. If you do, I’d argue that your time horizon is no longer your ~18-year life expectancy at age 67, but rather the much longer life expectancy of your kids when you’re 67. If that’s your plan, your stock allocation should likely stay at 100% to your last day. However, it also means that you need to accumulate a much larger portfolio to ensure that not only do you not run out of money before your passing even if a major bear market strikes, but that your portfolio thrives despite your drawing money to cover your retirement living expenses.

Takeaway

Regardless of the details, if you consider that your ability to earn money behaves much more like a bond than like stocks, your de-facto bond allocation is much higher than you think, and probably higher than it needs to be unless you’re within a few years of retirement. As long as this is true, a 100% portfolio equity allocation makes sense. Moreover, if your plan is to leave a large bequest to your heirs, that 100% equity allocation could extend up to (and perhaps even into) your retirement years.

Disclaimer

This article is intended for informational purposes only, and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.

About the Author

Opher Ganel has set up several successful small businesses, including a consulting practice supporting NASA and government contractors. His most recent venture is a financial strategy service for independent professionals. You can connect with him there, or by following his Medium publication, Financial Strategy.