How I Saved $60,000 during 2020

An Introduction

This is going to be the story of how I managed to save $60,000 over the course of 2020. Let me first give a brief breakdown on how much I am earning currently to put this all in context. I also want to preface all this by saying that in a year like 2020, I recognize that I have been extremely privileged and lucky to have a job.

According to my official pay statement, I earn around $130,000 annually. However, some of this includes more stock compensation, which I am due to receive in a couple of months’ time. Before taxes, I roughly earn $10,000 per month. I have been making regular contributions to my 401k retirement account and HSA (Health Savings Account).

Post-tax, it becomes around $7,000 in my bank account. I have had some changes to my pay this year, and I will go through those in more detail when I share later about how I was able to save $60,000 during the year.

How I Went About Saving

Prior to 2020, I was content to get my paycheck and spend; however much I felt like as long as it was less than what I had in my bank accounts at the end of the day. There wasn’t a hard and fast rule for me when it came to saving, but I was relatively frugal when by myself.

For the better part of 2019, I was hovering around $20,000 in my account. It felt like I was barely saving any money, even though I felt like I was cutting corners in other areas of my life to save money. At this point, $20,000 to just provide for me sufficient, but my lack of discipline in saving was resulting in my money not really going anywhere.

Around February 2020, I started getting interested in buying real estate because I was seeing more and more of my friends buying. Properties in my area were going up a lot, and it made sense to me from an investment perspective.

The only problem was that $20,000 as a 20% down payment was a joke in the Pacific Northwest (PNW). After browsing some more, I realized that the properties I liked generally started at $500,000. A 20% down payment for that would be $100,000! It was hard for me to imagine saving up to that amount when I felt like at most $1,000-$2,000 was going into my savings account.

Having a Goal

Now that I knew I wanted to have at least $100,000 saved, I was much more motivated to save. As Campbell McConnell once said, “Savings, remember, is the prerequisite of investment.” The investment here was my future home, and I wanted to get there as soon as my money could manage.

I had been tracking my spending in Mint for some time, but I started monitoring my spending more closely after this point. I knew that there were some areas that I did not want to give up, such as donating 10% of my post-tax income to charities and non-profits.

Saving Basics

There are two ways to save:

- Reduce your costs.

- Earn more money.

If you reduce your spending habits but earn less, you might save less money. The net savings you achieve depends on the balance between your cash inflow and outflow. Largely due to the pandemic and other side ventures, I was able to dramatically increase my rate of savings by doing both.

How I Reduced My Costs

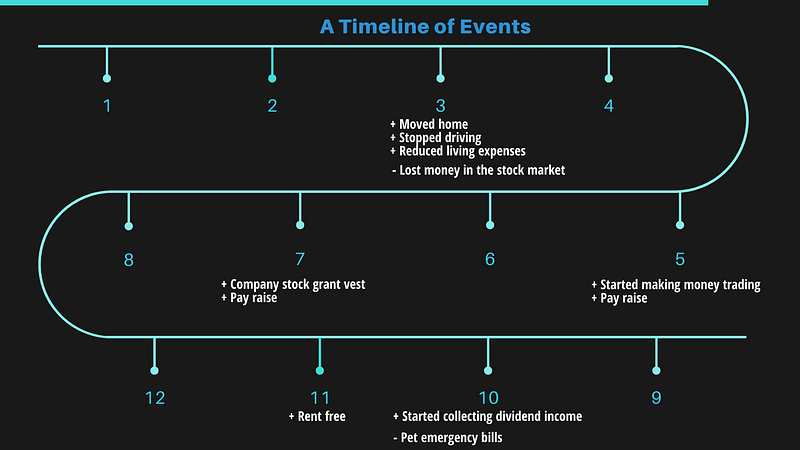

2020 was an exceptional year, and I am very blessed that the COVID-19 pandemic had little impact on the life of my family. Since I work an office job, I started working from home during the early stages of the pandemic. With most things shut down, I was barely driving anymore. I also realized that this would be a good time to go see my family and spend some time with them until things got better (this was when COVID-19 was not yet officially present in my parents’ city).

Since I left before my lease expired, I continued paying rent for a couple of months. After that, my landlord was kind enough to allow me to pay a discounted rate until I moved my things out. Of course, the pandemic got a lot worse since the spring of 2020, and I ended up living with my parents for the rest of the year. My parents are very loving and kind and haven’t charged me for rent even though I offer to pay, so I try to make it up by buying groceries sometimes and getting them things that they want.

Unfortunately, I have very few friends where my parents live. It didn’t matter to me so much at the beginning since I expected the pandemic to resolve itself soon. However, I have been able to keep up with my PNW friends through occasional Zoom calls, so I’ve been thankful for that.

Cost reductions summary:

- I moved home and am now rent-free

- Stopped driving: no more credit card bills for fueling up and paused driver’s insurance

- Reduced eating out: I get takeout with my family maybe once a week. That’s less than how I used to regularly eat out with friends a few times a week.

- Took advantage of work reimbursements to purchase home office equipment

How I Increased My Earnings

In the spring of 2020, I had my compensation review with my manager. My year-end feedback had been positive, and I got what my manager called an “average raise” of $2,000. This increased my take-home pay by $100 a month (after taxes). In July 2020, I received my first stock grant and got an extra $2,000. I also started getting paid an extra $1600 a month at work.

In addition to my full-time job, I became interested in the stock market in March after it fell a staggering amount at the onset of the pandemic. I had already invested around $8,000 in the stock market in some individual tech names, but most of my money was in my savings account.

My savings account interest rate was slashed, from 1.5% to 0.5% APY. I had heard of people who traded and invested their own money to impressive results, and I wanted to try my hand at it now that I had more time on my hands. If you’re interested in learning how to invest in the stock market, you can see my guide to investing here.

I lost money in the market from February to April as I did risky plays that I didn’t fully understand. I became really interested in options strategies and started selling options consistently in April.

In October, I got interested in investing with the purpose of collecting dividends. Prior to this, I would receive a few dollars here and there from some of my stock holdings, but I started paying more attention to the companies in my portfolio.

Since October, I have changed the holdings in my portfolio, so I started receiving $100 a month in dividends. Overall in 2020, I ended up investing $40,000 in the stock market and making $20,000 by trading (a 50% annual return).

How I Spent My Money

Life hasn’t been without expenses in the past year. I have been able to give more than 10% of my post-tax income to different organizations on a regular basis. I think it’s really important to use your money for the good of others, and I always want to donate at least 10% every year.

I also had some emergency expenses this year. My dog also developed an aggressive tumor in September. We never got insurance for her, and the medical bills were far above what I anticipated. I’m still kicking myself for not getting her insurance sooner, as that would have eased a lot of the headache spent getting her care that ultimately didn’t work.

Then there are the more ordinary expenses like grocery shopping and getting takeout. Overall, my spending on food is definitely less than what it was in 2019. I also still order quite a few items on Amazon for myself and my family if we need something.

The Final Result

All in all, I went from $19,193.55 in assets to $82,267.01 from January 1 to December 31 in 2020. There are some strange jumps in the numbers (in particular November), but those are due to account linking issues.

All in all, I’m really proud of how much more I was able to save in 2020. Quite a bit of my money is still in the stock market, but I have stopped depositing more money into my brokerage accounts in the past two months. I want to get to a point where I won’t have to liquidate as much of my stock positions if I end up wanting to make a home down payment.

Suppose you got all the way down to this point; thanks for taking the time to read my story. What’s yours, and where are you in your financial journey? I would love to hear from you in the comments :)

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.