Home Ownership Is A Bad Idea

The runaway American dream will sink your retirement

I came across something interesting recently when I was researching a stock.

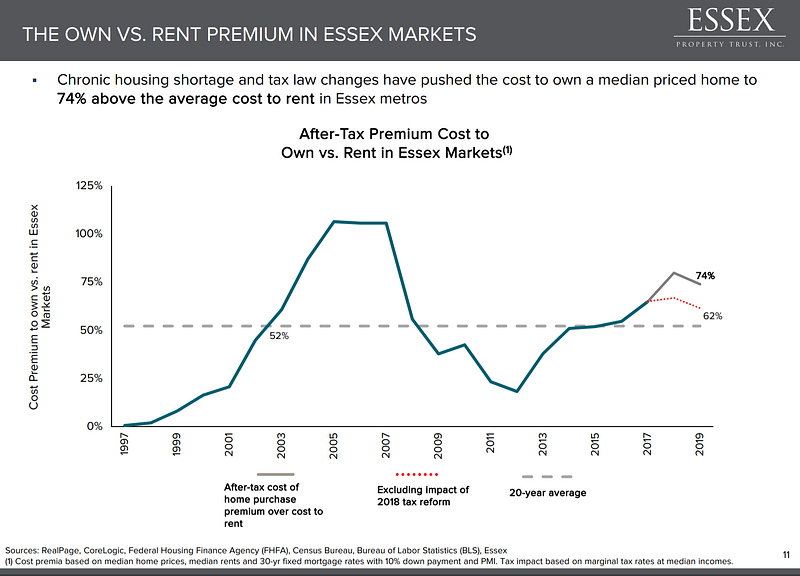

In expensive markets, such as San Francisco, Los Angeles, and Seattle, it’s less expensive to rent than it is to own. Not a surprise. I just didn’t know the extent of the rent advantage.

I have never bought into the myth of home ownership.

It’s a surefire way to inflate your expenses and make life a constant financial struggle, particularly in large cites.

And, unless you have plenty of money to spare, buying a home sets you up to spend too much of what you make and potentially sabotage your retirement. For most people, the so-called American dream ends up a massive expense.

If you’re middle or upper middle class, you’re better off having as much money as possible left over at the end of the month. Use it to pay your basic expenses, then save and invest the rest.

In the day we sweat it out on the streets of a runaway American dream At night we ride through mansions of glory in suicide machines

— Bruce Springsteen, Born To Run

Mansions Of Glory, Suicide Machines

Consider the biggest barrier of entry to home ownership for many people — the down payment.

According to consumer association HSH, you must make $128,444 a year to afford a $592,800 (median price) home in Los Angeles. This calculation takes into account a 10 percent down payment.

That’s $59,280.

And that’s a lot of money for quite a few people. It takes a long time to save enough to afford a home that sits in the middle of Los Angeles’s real estate landscape. At the median, you’re probably going to have to settle for a neighborhood that isn’t your first choice and a house that isn’t of your dreams. We see our new homeowner friends do it everyday, moving to a less desirable district just so they can own a home.

This common approach results in dumping $60,000 into a loan that generates a monthly payment north of $2,500. And you’re not in the neighborhood or living space you really want to be in.

Want an upgrade? You’re on your way to living beyond your means, just so you can own a home.

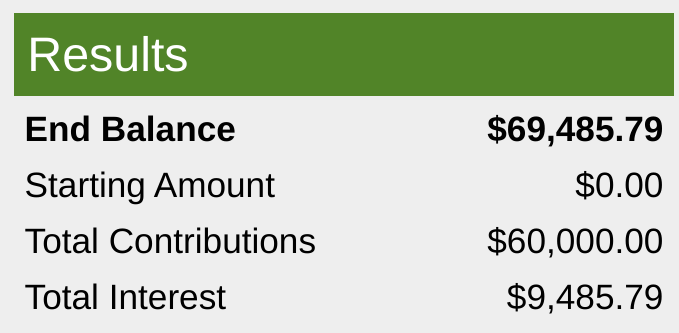

Imagine an alternative scenario where you invested that $60,000 and let it compound alongside regular monthly investments versus one where you started with nothing alongside regular monthly contributions.

Here are your results over a five-year period when you start at zero and invest $1,000 a month, assuming a six percent annual rate of return. I chose $1,000 a month over five years because that’s roughly how long it would take you to accumulate $60,000 in cash.

Here’s how things look if you did the exact same thing, but started with $60,000.

I’d rather have an extra $80,293 (and 53 cents) in my investment account after just five years than a house any day of the week.

I won’t even factor in how much more money you might have had you invested in dividend-paying stocks and, with any luck, contributed more than $1,000 a month over that five-year time frame.

What’s Your Goal?

For an increasing number of people in their 20’s, 30’s, and 40’s, the goal isn’t the acquisition of material things.

While some view a home as an investment, it also requires spending that goes far beyond your down payment and monthly mortgage obligation. You’re on the hook for all sorts of associated costs from property tax to regular and unexpected maintenance.

Speaking for myself, it has become a condescending refrain when the consensus claims that I want experiences over material things. Don’t simplify things as to make them easier to not only understand, but to denigrate as some Utopian, modern-day hippie fantasy.

I don’t merely want experiences over things. I want to call my own shots. I want to live how I want to live now and in the future. I want to allocate my income towards this goal — and whatever a non-linear retirement looks like for me — rather than what amounts to a possession.